For small and mid-sized businesses, maintaining healthy cash flow is the key to seizing opportunities and navigating unexpected challenges. A business line of credit offers a flexible, revolving safety net that traditional term loans cannot match. Unlike a lump-sum loan, it provides access to a preset capital limit that you can draw from as needed, paying interest only on the funds you use. This powerful tool is essential for managing payroll during slow seasons, purchasing inventory to meet a surge in demand, or bridging cash flow gaps between projects.

However, the modern lending market is crowded. With a vast array of traditional banks, online lenders, and marketplaces all competing for your attention, identifying the right partner for your company's unique financial situation can be a significant hurdle. How do you distinguish between similar offers to find the truly best business lines of credit for your specific industry and revenue model? This guide is designed to cut through the noise and provide a clear, direct path to the right financing.

We will provide a detailed roundup of the top providers, from fintech innovators like Bluevine to established institutions like Wells Fargo, and brokers like FSE that can streamline your search. Each review includes a direct link to the provider’s website, helping you quickly move from evaluation to application. Whether you need to fund a new project, expand your fleet, or simply establish a reliable source of working capital, this is your roadmap to securing the flexible funding your business deserves.

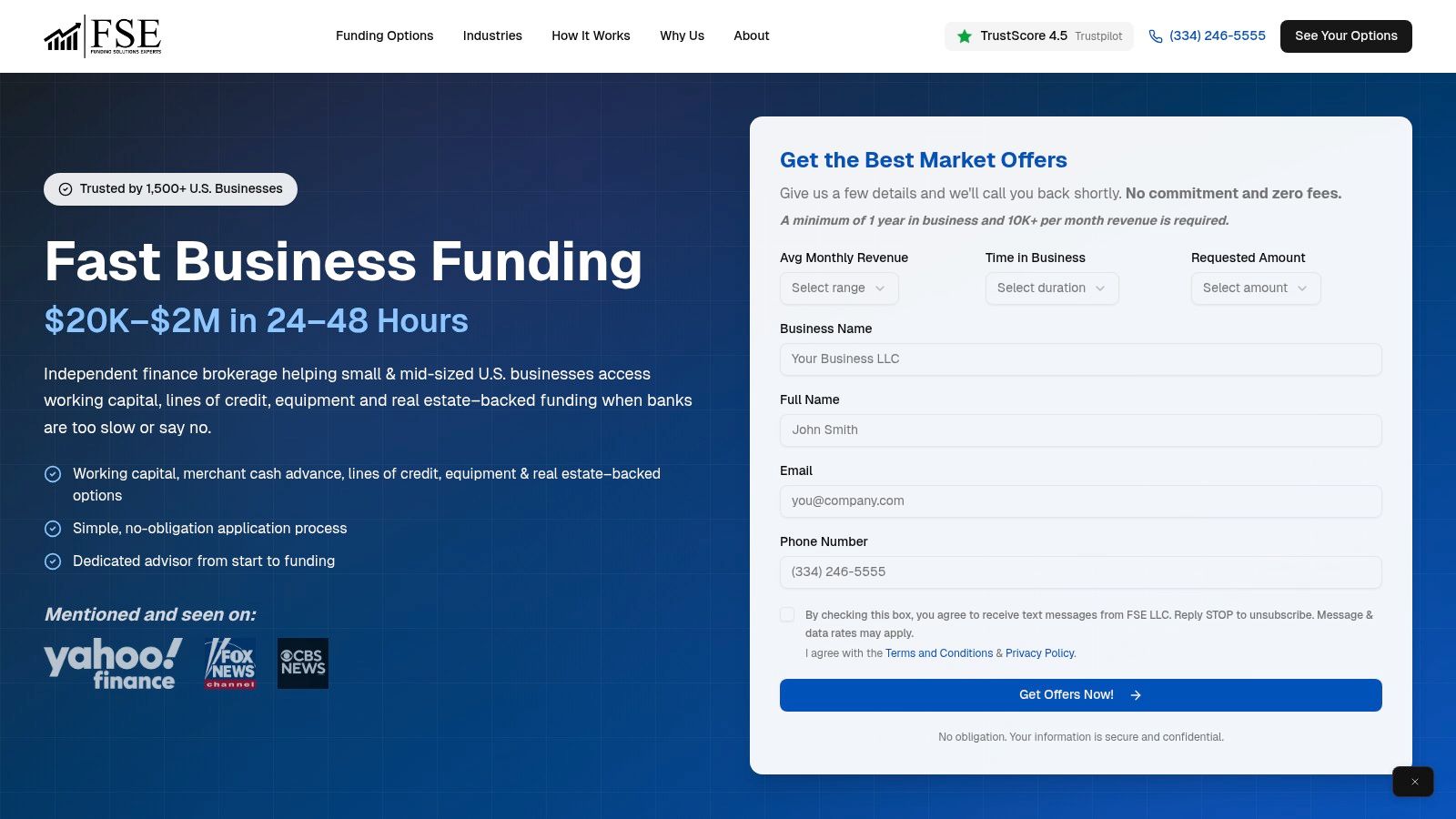

1. FSE - Funding Solution Experts

FSE - Funding Solution Experts earns its place as our featured choice by functioning as a strategic financial partner rather than just a direct lender. As an independent commercial finance brokerage, FSE leverages a vast network of over 50 lending partners to connect small and mid-sized U.S. businesses with tailored capital solutions. This model is particularly effective for companies that need funding faster than a traditional bank can provide or for those who have been turned down by conventional institutions. The platform’s strength lies in its ability to quickly source and compare multiple competitive offers, ensuring businesses find the best business lines of credit and other financing products that align with their specific operational needs.

The core of the FSE experience is its combination of technology and personalized guidance. While the initial application is a simple online form that takes minutes to complete, each client is paired with a dedicated advisor. This expert acts as a single point of contact, navigating the lender network on the client's behalf, demystifying complex terms, and helping structure repayments that match the business’s cash flow cycle. This high-touch service removes the friction and uncertainty often associated with securing business capital.

Key Features and Strategic Advantages

FSE stands out by offering a holistic approach to business funding that goes beyond a single product. Its diverse portfolio and streamlined process provide significant advantages.

- Expedited Funding Cycle: The platform is built for speed. Businesses often receive preliminary decisions within 24 hours of applying, with funds typically deposited in their accounts within 24 to 48 hours after approval. This rapid turnaround is critical for capitalizing on time-sensitive opportunities or managing unexpected expenses.

- Extensive Lender Marketplace: Access to over 50 lenders dramatically increases the probability of approval and encourages competitive rates and terms. Instead of applying to multiple lenders individually, a single FSE application opens the door to a wide array of options, from working capital loans to lines of credit up to $250,000.

- Dedicated Advisory Service: The inclusion of a dedicated advisor is a key differentiator. This expert provides invaluable support by comparing market offers, explaining the nuances of each option, and ensuring the final financing structure is a sustainable fit for the business.

- Broad Product Versatility: FSE’s network offers a comprehensive suite of products, including revolving lines of credit, equipment financing, commercial real estate loans, merchant cash advances, and even reverse consolidations designed to improve weekly cash flow. This versatility makes it a one-stop shop for businesses with evolving capital needs.

Ideal Use Cases and Practical Tips

FSE is an excellent fit for established businesses (typically with at least one year of history and $10,000+ in monthly revenue) that prioritize speed, flexibility, and expert guidance.

A construction company, for example, could secure a line of credit through FSE to manage payroll and material costs between project milestones, ensuring smooth operations without waiting for client payments. Similarly, a retail business could use a fast working capital loan to purchase bulk inventory ahead of a peak season, maximizing sales potential.

To use the platform effectively, have your recent bank statements and basic business information ready. This will help your advisor quickly assess your financial health and match you with the most suitable lenders.

| Feature Summary | Details |

|---|---|

| Best For | Established SMBs needing fast, flexible capital and expert guidance. |

| Funding Speed | Decisions in ~24 hours; funding in 24-48 hours. |

| Credit Lines | Up to $250,000, depending on lender and qualifications. |

| Eligibility | Typically 1+ year in business, $10K+ monthly revenue. |

| Lender Network | 50+ partners offering diverse loan products. |

| Customer Support | Dedicated advisor for personalized service. |

Pros:

- Very fast funding timeline.

- High approval odds due to a large lender network.

- Personalized guidance from a dedicated advisor.

- Wide range of financing products for various needs.

Cons:

- As a brokerage, rates may be higher than direct bank loans.

- Minimum eligibility requirements exclude very new startups.

Website: https://www.fseb2b.com

2. Bluevine

Bluevine has established itself as a top-tier fintech lender, specifically for businesses seeking one of the best business lines of credit with an emphasis on speed and simplicity. It’s an ideal solution for established businesses that require rapid access to working capital to seize opportunities, manage cash flow gaps, or handle unexpected expenses without the lengthy approval process of a traditional bank. The platform’s streamlined online application and transparent qualification criteria make it a standout choice for time-crunched entrepreneurs.

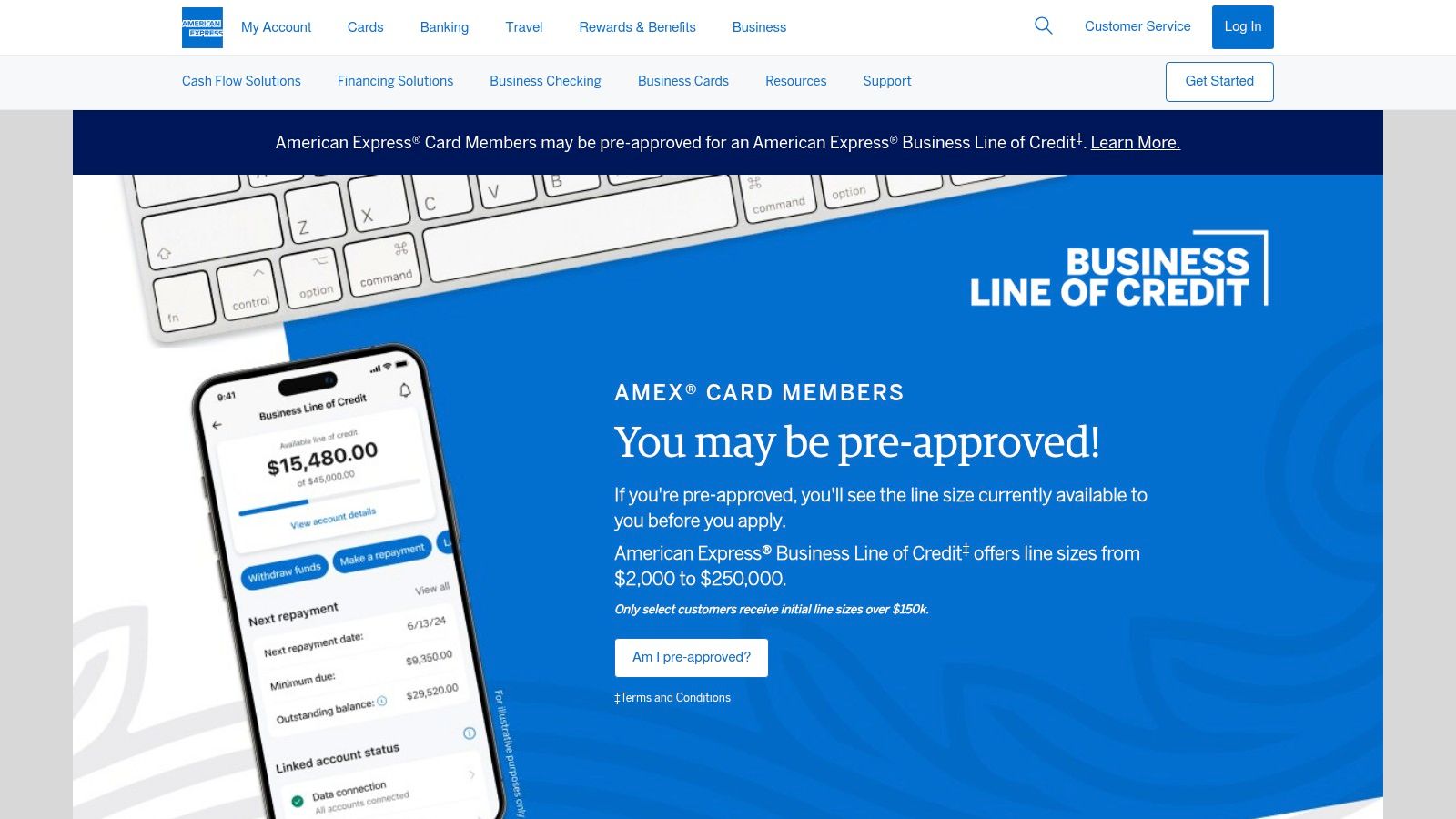

Leveraging one of the most trusted names in finance, the American Express Business Blueprint platform offers one of the best business lines of credit for established businesses seeking transparency and flexibility. This product is a strong fit for businesses that value a clear fee structure and the backing of a major financial institution. The AmEx line of credit provides a unique hybrid model, allowing business owners to convert each draw into either a short-term single-repayment loan or a longer-term installment loan, offering customized repayment options based on specific cash flow needs.

Key Features and Offerings

The revolving nature of the American Express line of credit means that as you repay your balance, your available credit replenishes. The standout feature is the ability to choose your repayment structure for each individual draw. This allows you to use a short, single-repayment loan for a quick inventory turn and a longer installment loan for a capital improvement project, all from the same credit line.

- Credit Lines: Typically from $2,000 to $250,000.

- Funding Speed: Funds are typically deposited into your business bank account within 1 to 3 business days after a draw is approved.

- Repayment Terms: Draws can be structured as single-repayment loans (1-3 months) or installment loans (6-24 months).

- Fees: American Express provides a published table of fee ranges based on the loan term, providing exceptional transparency.

Eligibility and Application Process

American Express is clear about its minimum qualifications, making it easier for businesses to determine if they are likely to be a good fit. Some existing AmEx business card members may see pre-approval offers within their Blueprint dashboard, further simplifying the process.

| Requirement | Minimum Threshold |

|---|---|

| Time in Business | 12+ months |

| Personal FICO Score | 660+ |

| Monthly Revenue | $3,000+ |

| Business Structure | Most U.S.-based business structures are eligible. |

The application is entirely online and integrates with the Business Blueprint dashboard, which provides a holistic view of your AmEx financial products. You will need to provide standard business information and connect your business bank account to verify revenue.

Pro Tip: Existing American Express business customers should check their Blueprint dashboard first. You may find a pre-approved offer, which can streamline the application and provide immediate insight into your potential credit limit and terms.

Pros and Cons

Pros:

- Transparent Pricing: Clear, published fee ranges help you understand the cost of borrowing before you draw funds.

- Flexible Draw Structure: The ability to choose between single-repayment and installment terms for each draw is a unique and powerful feature.

- Strong Brand Reputation: Borrowing from a globally recognized and trusted brand like American Express.

- Integrated Financial Dashboard: The Blueprint platform provides a central hub for managing your AmEx financial products.

Cons:

- Requires Personal Guarantee: Like most small business financing, this line of credit requires a personal guarantee and is secured by business assets.

- No Early Payoff Discount: For single-repayment loans, paying the balance early does not reduce the total fee owed.

- Larger Lines Favor Existing Customers: Credit lines above approximately $150,000 are often reserved for businesses with a significant, pre-existing relationship with AmEx.

Visit American Express Business Blueprint to learn more and apply.

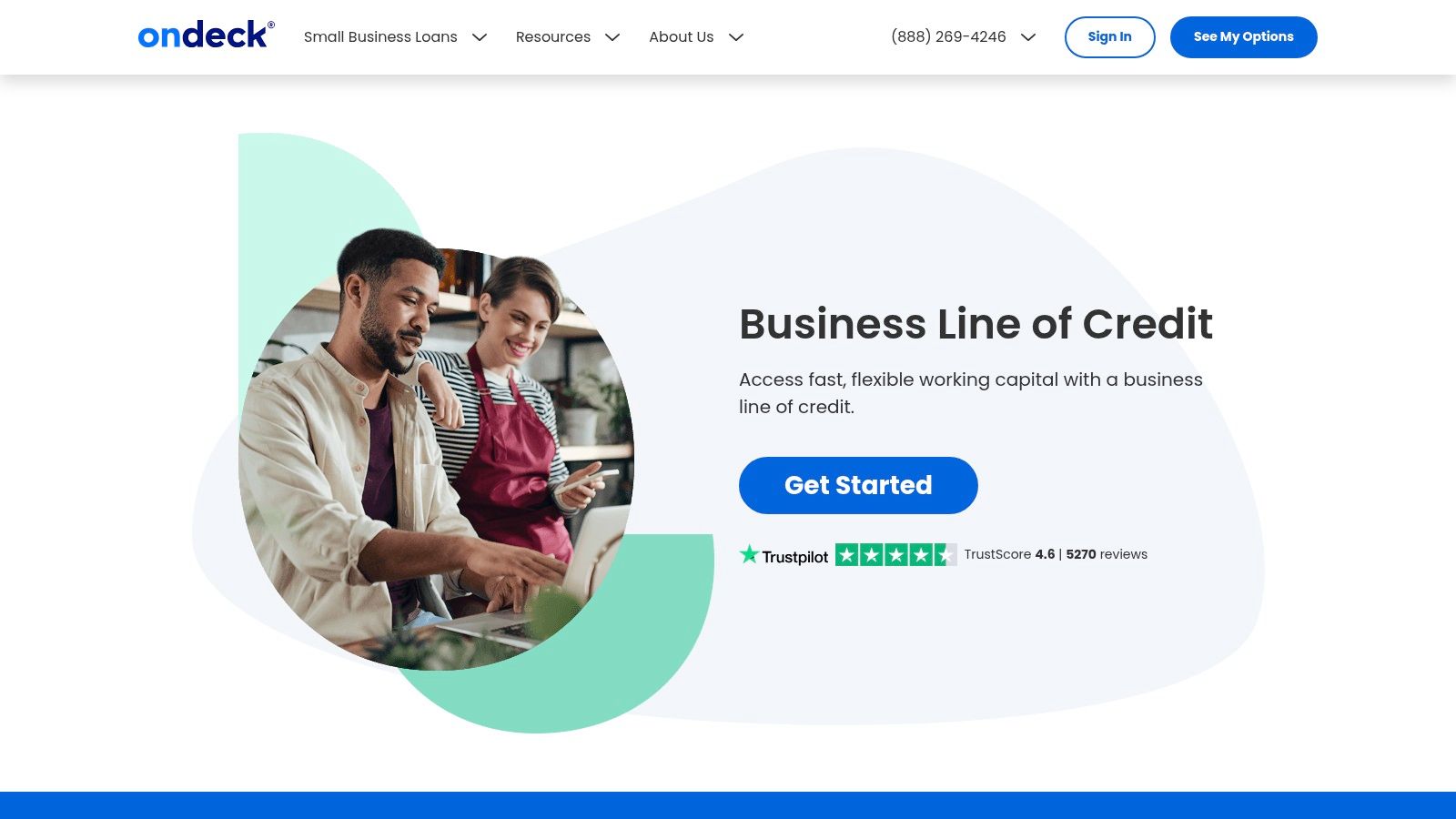

4. OnDeck

OnDeck has carved out a strong reputation in the fintech lending space as a go-to source for one of the best business lines of credit for established small businesses needing reliable, on-demand capital. It excels at providing a straightforward application process and rapid funding, making it an excellent choice for businesses that have moved beyond the startup phase and require a flexible credit facility to manage cash flow, purchase inventory, or cover unexpected operational costs without the red tape of traditional banking.

What sets OnDeck apart is its emphasis on flexibility and relationship-building. Once approved, eligible borrowers can access instant funding on withdrawals 24/7, a critical feature for businesses that operate outside of standard banking hours. This focus on immediate access and transparent terms positions OnDeck as a powerful tool for dynamic businesses that can't afford to wait for capital.

Key Features and Offerings

OnDeck's revolving business line of credit is built for frequent use and easy management. You draw funds as needed, pay interest only on what you use, and your available credit replenishes as you make repayments. This structure is ideal for handling recurring expenses or seizing growth opportunities as they arise.

- Credit Lines: From $6,000 to $100,000

- Funding Speed: Potentially as fast as same-day funding for draws.

- Repayment Terms: Flexible 12, 18, or 24-month terms with a choice of weekly or monthly payments.

- Fees: A monthly maintenance fee applies, which is waived for the first six months if you draw $5,000 or more in the first five days of opening your line.

Eligibility and Application Process

OnDeck is commendably clear about its minimum qualifications, enabling business owners to quickly determine if they are a good fit before starting an application. This transparency saves time and helps manage expectations.

| Requirement | Minimum Threshold |

|---|---|

| Time in Business | 1+ year |

| Personal FICO Score | 625+ |

| Annual Revenue | $100,000+ |

| Business Structure | Most structures accepted |

The application is entirely online and can be completed in minutes. By securely linking your business bank account, you provide OnDeck with the information needed for a quick review, often resulting in a decision within the same business day.

Pro Tip: Align your repayment schedule (weekly or monthly) with your business's cash flow cycle. If you have consistent daily or weekly revenue, a weekly payment might be easier to manage and could result in lower overall interest costs.

Pros and Cons

Pros:

- Rapid Funding on Draws: Instant 24/7 funding for draws is available to eligible borrowers, providing unparalleled access to capital.

- Clear Eligibility Criteria: Upfront requirements allow for easy self-assessment before applying.

- Flexible Repayment Options: The choice between weekly and monthly payments helps align with different business models.

- Builds Business Credit: OnDeck reports payment activity to major business credit bureaus, helping you build a stronger credit profile.

Cons:

- Higher Costs than Banks: As with most fintech lenders, the convenience and speed may come with higher interest rates compared to a traditional bank loan.

- Revenue Requirement: The $100,000 minimum annual revenue can be a barrier for very new or micro-businesses.

- Monthly Maintenance Fee: A recurring fee applies after the initial waiver period, adding to the overall cost of the credit line.

Visit OnDeck to learn more and apply.

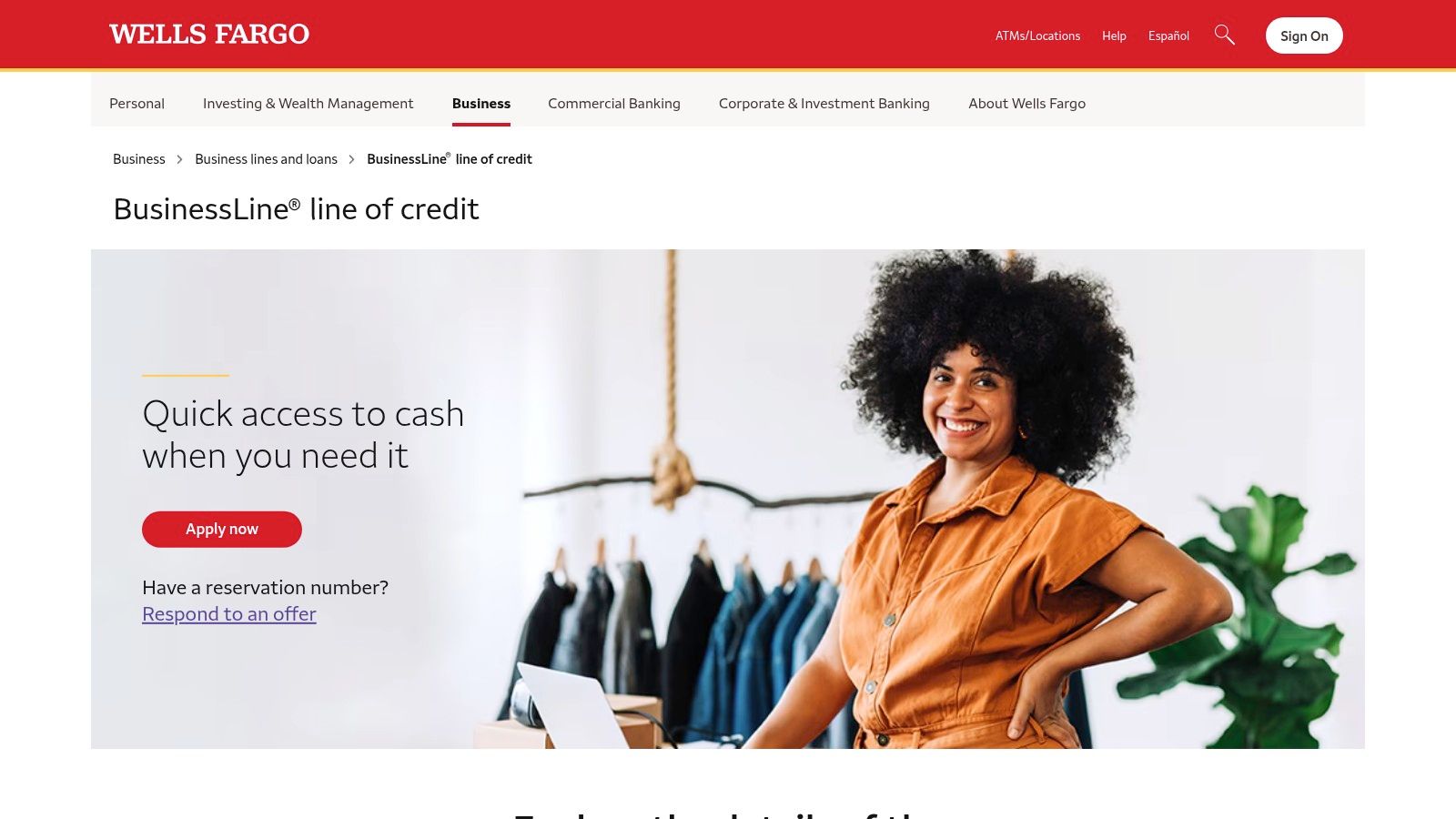

5. Wells Fargo (BusinessLine and Prime Line of Credit)

For businesses that prefer the established framework and integrated services of a traditional bank, Wells Fargo offers some of the best business lines of credit through its BusinessLine and Prime Line products. This option is ideal for established companies with strong credit profiles seeking potentially lower interest rates and the convenience of managing their credit, checking, and other financial services all under one roof. Unlike many fast-paced fintech lenders, Wells Fargo provides a more conventional banking relationship, complete with in-person support and a full suite of treasury tools.

The primary advantage of a Wells Fargo line of credit is its direct link to the Prime Rate, which can result in more favorable variable rates for highly qualified borrowers. The bank’s ability to offer both unsecured options for smaller needs and large secured lines for major investments makes it a versatile, long-term financial partner.

Key Features and Offerings

Wells Fargo structures its offerings to meet different business scales. The unsecured BusinessLine is designed for everyday working capital, while the larger Prime Line is secured and built for significant capital needs. Both operate as revolving credit, allowing you to draw and repay funds as your business requires.

- Credit Lines: Up to $100,000 (unsecured BusinessLine); $500,001 to $3,000,000 (secured Prime Line).

- Funding Speed: Slower than online lenders; the process involves more comprehensive underwriting and can take several days to weeks.

- Repayment Terms: Flexible, revolving credit with monthly payments on the outstanding balance.

- Fees: Annual fee of $95 (lines $10k–$25k) or $175 (> $25k) on BusinessLine, waived for the first year.

Eligibility and Application Process

As a traditional bank, Wells Fargo has stricter and more documentation-intensive requirements compared to online alternatives. A strong credit history and solid business financials are key to a successful application.

| Requirement | Typical Threshold |

|---|---|

| Time in Business | 6+ months (often prefers 2+ years) |

| Personal FICO Score | 680+ for guarantors |

| Annual Revenue | Varies; must demonstrate strong, consistent cash flow |

| Documentation | Business and personal tax returns, financial statements, business plan may be required |

Applications can be started online but often require follow-up with a banking representative, either over the phone or at a local branch. This hands-on process provides personalized guidance but extends the approval timeline.

Pro Tip: Consolidate your business checking and credit card services with Wells Fargo before applying. A pre-existing banking relationship can significantly strengthen your application and may lead to better terms.

Pros and Cons

Pros:

- Potentially Lower Rates: Well-qualified borrowers may access more competitive variable interest rates tied to the Prime Rate.

- Integrated Banking: Seamlessly manage your line of credit alongside checking, savings, and other business services.

- Builds Strong Bank Relationship: Establishes a formal banking relationship that can be beneficial for future, larger financing needs.

- High Credit Limits: Secured lines offer substantial capital for major growth initiatives.

Cons:

- Slower Funding Process: Underwriting is more thorough and takes significantly longer than fintech options.

- Stricter Requirements: Newer businesses or those with less-than-perfect credit may find it difficult to qualify.

- Annual Fees: The BusinessLine product comes with an annual fee after the first year.

- Requires More Documentation: Expect to provide extensive financial paperwork during the application process.

Visit Wells Fargo to learn more and apply.

6. Lendio

Lendio operates not as a direct lender but as a powerful lending marketplace, making it one of the best business lines of credit resources for owners who want to maximize their options with minimal effort. Instead of applying to multiple lenders one by one, Lendio allows businesses to submit a single, 15-minute application to get matched with its network of over 75 lenders. This approach is perfect for business owners who have been declined by a traditional bank or simply want to compare multiple offers side-by-side to find the most competitive terms without investing significant time in the search.

The platform’s core value lies in its efficiency and breadth of choice. By casting a wide net, Lendio increases the probability of securing an approval and empowers borrowers to make a more informed financing decision. Access to a dedicated funding advisor further demystifies the process, providing expert guidance to help navigate and compare the various offers received.

Key Features and Offerings

Lendio’s marketplace model means that the specifics of a line of credit (such as rates, terms, and fees) will vary depending on the lender you are matched with. However, the platform provides a centralized and streamlined experience for accessing these diverse options.

- Lender Network: Access to 75+ lenders with one application.

- Funding Speed: Varies by lender, but funding can be available as fast as 24 hours.

- Repayment Terms: Dependent on the final lender; terms are presented for comparison.

- Fees: Lendio’s service is free for the borrower; all fees and interest rates are set by the matched lender.

Eligibility and Application Process

Since Lendio works with a wide range of lenders, its eligibility requirements are more of a general guideline. Different lenders within the network have their own specific criteria, making the platform suitable for a broad spectrum of businesses, from startups to established enterprises.

| Requirement | Minimum Threshold |

|---|---|

| Time in Business | 6+ months |

| Personal FICO Score | 600+ |

| Monthly Revenue | $10,000+ |

| Business Structure | Most structures accepted, including sole proprietorships |

The application is entirely online and designed for speed. You provide basic details about your business and its financial health. Lendio then uses this information to match you with potential lenders, and you will typically start seeing offers within hours.

Pro Tip: When you receive offers through Lendio, pay close attention to the total cost of capital, not just the interest rate. Compare APRs, draw fees, and any maintenance fees to understand the true cost of each line of credit.

Pros and Cons

Pros:

- Saves Significant Time: One application provides access to dozens of lenders, eliminating the need to shop around.

- Increases Approval Odds: A broader pool of lenders means a higher chance of finding a match, especially for those with less-than-perfect credit.

- Expert Guidance: Funding advisors can help you understand and compare complex loan terms.

- Wide Range of Options: Caters to various business needs and credit profiles.

Cons:

- Inconsistent Terms: Rates and fees vary widely between matched lenders, requiring careful review of each offer.

- Adds an Intermediary: Communication may go through Lendio instead of directly with the lender, which can sometimes slow down the process.

- You Must Vet Lenders: The responsibility is on the borrower to research and evaluate the specific lender they choose.

Visit Lendio to learn more and apply.

7. Headway Capital

Headway Capital, a part of Enova International, offers a direct and transparent "True Line of Credit" designed for small businesses that value clarity and flexibility. It solidifies its place as one of the best business lines of credit by providing a straightforward revolving credit facility without the complex structures of some competitors. The platform is an excellent fit for businesses needing dependable, ongoing access to working capital with clear terms and the ability to manage repayment schedules to match their unique cash flow cycles.

What sets Headway Capital apart is its commitment to pricing transparency, featuring an online calculator to help applicants estimate costs before committing. This, combined with flexible repayment options and rapid funding, makes it a reliable choice for businesses that need to plan their finances precisely while retaining quick access to funds for inventory, payroll, or operational expenses.

Key Features and Offerings

Headway Capital’s revolving line of credit operates like a traditional credit card: you draw funds as needed, and your credit line replenishes as you repay. This structure is ideal for managing uneven revenue streams or for having a financial safety net ready for immediate deployment.

- Credit Lines: Up to $100,000

- Funding Speed: Next-business-day funding after approval.

- Repayment Terms: Flexible weekly or monthly payment schedules with terms of 12, 18, or 24 months.

- Fees: A draw fee may apply in many states on each withdrawal, in addition to interest charges.

Eligibility and Application Process

Headway Capital provides clear, upfront minimum qualifications, which helps business owners determine their eligibility before starting an application. This transparency saves time and streamlines the funding process for qualified applicants.

| Requirement | Minimum Threshold |

|---|---|

| Time in Business | 1+ year |

| Personal FICO Score | 625+ |

| Annual Revenue | $50,000+ |

| Business Location | Must operate in an eligible state |

The online application process is designed for speed and simplicity. You will need to provide basic business details and consent to a credit check. A decision is typically rendered quickly, allowing for next-day access to capital upon approval.

Pro Tip: Use Headway Capital's online calculator with your own business data to get a realistic estimate of your potential repayment costs. This helps you model how a draw will impact your cash flow before you accept an offer.

Pros and Cons

Pros:

- Flexible Repayment Cadence: Choose between weekly or monthly payments to best align with your business's revenue cycle.

- Transparent Eligibility: Clear minimum requirements allow for easy self-assessment before applying.

- Prepayment Benefits: You can pay off your balance early to reduce the total interest paid without incurring prepayment penalties.

- True Revolving Credit: Your credit line is fully replenished as you repay, ensuring capital is always available.

Cons:

- Lower Maximum Line: The $100,000 credit limit may be insufficient for larger businesses or those with significant capital needs.

- Draw Fees: A fee may be charged on each draw in certain states, which increases the overall cost of borrowing.

- Revenue Minimums: The $50,000 annual revenue requirement can be a barrier for newer or smaller-scale businesses.

Visit Headway Capital to learn more and apply.

Top 7 Business Lines of Credit Comparison

| Product | Implementation 🔄 | Resources ⚡ | Expected outcomes 📊 | Ideal use cases 💡 | Key advantages ⭐ |

|---|---|---|---|---|---|

| FSE - Funding Solution Experts | Medium 🔄 — broker coordinates 50+ lenders; advisor-assisted process | Moderate ⚡ — quick online app; needs ~1+ year in business and ~$10K+/mo revenue | 📊 Fast approvals (prelim ~24h), funds in 24–48h; wide product mix | 💡 Businesses needing tailored options across products and fast funding | ⭐ Network breadth, advisor support, proven funding volume |

| Bluevine | Low 🔄 — direct fintech, streamlined online flow | Low ⚡ — 12+ months, 625+ FICO, ~$10K+/mo; instant draws with Bluevine Checking | 📊 Very fast decisions (minutes to hours); lines up to $250K | 💡 Firms needing quick, transparent revolving working capital | ⭐ Fast funding, clear eligibility, competitive max line for fintech |

| American Express Business Blueprint | Medium 🔄 — branded, integrated dashboard and published terms | Moderate ⚡ — 1+ year, 660+ FICO, $3K+ monthly; personal guarantee often required | 📊 Predictable fee ranges; flexible converts (single-pay or installment) | 💡 AmEx customers or businesses wanting transparent pricing and tools | ⭐ Clear pricing, flexible draw structure, brand reliability |

| OnDeck | Low 🔄 — direct online lender with fast workflows | Moderate ⚡ — 1+ year, ~ $100K annual revenue, 625 FICO typical | 📊 Instant funding on withdrawals for eligible borrowers; lines up to $200K | 💡 Businesses needing frequent-access financing and quick draws | ⭐ Speed, flexible weekly/monthly repayment cadence |

| Wells Fargo (BusinessLine / Prime) | High 🔄 — traditional bank underwriting, in-branch options | High ⚡ — stronger credit/history (~680+), full documentation; secured options for large lines | 📊 Potentially lower variable rates for well-qualified borrowers; larger credit limits | 💡 Established businesses seeking lower rates and integrated banking services | ⭐ Lower rates for strong profiles, full banking product suite |

| Lendio | Low 🔄 — marketplace single-application matching to 75+ lenders | Low ⚡ — one application; lender-specific eligibility and fees apply | 📊 Broad range of offers; funding speed varies by matched lender | 💡 Businesses wanting to compare many lenders quickly or after a bank decline | ⭐ Wide lender access, advisor guidance, time-saving shopping |

| Headway Capital | Low-Medium 🔄 — direct lender with transparent examples | Moderate ⚡ — 1+ year, ≥$50K revenue; lines up to $100K | 📊 Next-business-day funding post-approval; transparent pricing; lower max line | 💡 Small businesses needing predictable costs and flexible repayment cadence | ⭐ Clear pricing, prepayment reduces cost, weekly/monthly repayment options |

Making the Right Choice: How to Secure Your Best-Fit Funding

Navigating the landscape of business financing can feel complex, but securing the right business line of credit is a strategic move that can unlock significant growth and operational stability. Throughout this guide, we've explored a diverse range of top-tier options, from the fast, tech-driven solutions of fintech lenders like Bluevine and OnDeck to the established, low-rate products offered by traditional banks like Wells Fargo. We've also seen how innovative platforms like American Express Business Blueprint and marketplaces such as Lendio are reshaping how businesses access capital.

The key takeaway is that the "best" option is not universal; it is entirely dependent on your company's specific circumstances, priorities, and financial health. The ideal choice hinges on a careful evaluation of your own needs against what each lender provides.

Distilling Your Priorities: From Speed to Cost

To make a confident decision, you must first clarify your primary objective. Is your goal to secure funding as quickly as possible to seize an unexpected opportunity or cover an immediate shortfall? If so, online lenders are often your most efficient path forward.

Alternatively, if your main concern is minimizing the cost of capital over the long term, and you have the strong credit and documentation to prove it, a traditional bank may be worth the more rigorous application process. For businesses that fall somewhere in between or are unsure of their eligibility, a marketplace or brokerage model offers a crucial advantage by presenting multiple options at once.

Key Insight: Your most important decision is not just which lender to choose, but which type of lender aligns with your business's core needs: speed, cost, flexibility, or expert guidance. A mismatch in priorities is the most common reason for a failed funding attempt.

A Strategic Framework for Your Final Decision

Before submitting your first application, use this final checklist to align your business profile with the right funding partner. This structured approach will save you time, reduce frustration, and increase your odds of a successful outcome.

- Assess Your Timeline: How urgently do you need the capital? If funds are needed within 24-48 hours, focus exclusively on online lenders. If you have several weeks, you can expand your search to include banks and SBA-backed options.

- Review Your Financials: What is your business credit score, annual revenue, and time in business? Be realistic. A business with six months of history and $100,000 in revenue will not qualify for the same products as one with five years of history and $2 million in revenue.

- Define the Use Case: Why do you need this line of credit? Is it for consistent working capital, a one-time equipment purchase, or managing seasonal inventory fluctuations? The answer will help determine whether a revolving line or a different product, like a term loan, is more appropriate.

- Compare the Total Cost: Look beyond the interest rate. Factor in all potential fees, including origination fees, draw fees, maintenance fees, and prepayment penalties. A slightly higher rate from a lender with zero fees may ultimately be more affordable.

The Power of an Expert Partner

Choosing from the best business lines of credit can be a resource-intensive process. Applying to multiple lenders individually can lead to numerous credit inquiries and wasted effort if you are not targeting the right partners for your profile. This is where the strategic value of a dedicated funding advisor becomes clear.

Instead of navigating this complex market alone, a brokerage like FSE - Funding Solution Experts acts as your advocate. They take the time to understand your business's unique situation and then leverage their extensive network of over 50 lenders to find a suitable match. This single-application, multi-offer approach not only saves time but also provides a competitive environment where lenders vie for your business, ensuring you receive the best possible terms.

Ultimately, a business line of credit is more than just a loan; it's a flexible financial tool that empowers you to invest in growth, manage cash flow with confidence, and build a more resilient company. By carefully considering your options and, when necessary, leaning on expert guidance, you can secure the funding you need to turn your business ambitions into reality.

Ready to find the perfect business line of credit without the exhaustive search? Partner with FSE - Funding Solution Experts to access a vast network of lenders with a single, streamlined application. Let our dedicated advisors do the heavy lifting to match you with the best funding options for your specific business needs.

Get Your Personalized Funding Offers with FSE - Funding Solution Experts