A commercial bridging loan is really a specialized, short-term financing tool designed for one thing: speed. Think of it as a financial stopgap, a way to get from Point A to Point B when you need immediate cash and can't wait for traditional financing to come through.

It’s perfect for those time-sensitive opportunities, like snapping up a property at auction, that require you to act now before a more permanent funding solution is in place.

So, What Exactly Is a Commercial Bridging Loan?

Imagine you’ve found the perfect commercial property, but the deal closes in two weeks. A traditional bank loan could take months to approve, meaning you'd lose the opportunity. This is where a commercial bridging loan comes in. It acts as a sturdy, temporary bridge to get you across that financial gap quickly, securing the asset while you arrange your long-term mortgage.

This type of funding is a powerful alternative to the slower, more rigid process of traditional lenders. While a bank gets bogged down in paperwork, bridging lenders are built for speed, often wiring funds in a matter of days, not months. That agility makes them an indispensable tool for real estate developers, investors, and business owners who can't afford to wait.

The Core Purpose: Fast Cash for Big Moves

At its heart, a commercial bridging loan is all about providing liquidity precisely when it’s needed most. Its real value isn't in its long-term cost, but in its rapid deployment. Businesses turn to these loans to solve urgent cash flow problems or, more commonly, to pounce on opportunities that would otherwise vanish.

Here are a few classic scenarios where they make all the difference:

- Auction Purchases: You need to pay for a winning bid almost immediately.

- Property Development: You need funds to start renovations or construction before the long-term development loan is finalized.

- Fixing a Broken Chain: You're buying a new commercial space but the sale of your old one is delayed.

- Urgent Business Expansion: You need to acquire new equipment or inventory to handle a sudden surge in demand.

This strategic use of short-term capital is becoming more and more common. In January 2025 alone, private lenders handled over 4,200 bridge loan transactions totaling more than $2 billion—that’s a 51% jump from the previous year. As recent market trend analyses show, this surge highlights just how much businesses in major U.S. markets are relying on quick, flexible funding.

Ultimately, this is where a brokerage like FSE comes in. We connect businesses with the right lenders to build that financial bridge. We help you frame your opportunity in a way that meets lender criteria, making sure you get the capital you need to move forward without missing a beat.

Understanding How Bridging Loans Work

A commercial bridging loan is built for one thing: speed. It provides a rapid injection of asset-backed cash to close a short-term financial gap, letting you pounce on an opportunity before it disappears. The whole process is designed to be fast, focusing on the value of the property and your plan to pay back the loan, not a months-long deep dive into your business's financial history.

Think of it this way: a traditional bank loan is like booking a commercial flight. It’s methodical, requires lots of paperwork and advance planning, and ultimately gets you there on a set schedule. A bridging loan is like chartering a private jet. It’s more expensive, sure, but it gets you exactly where you need to be, right when you need to be there, bypassing all the usual delays.

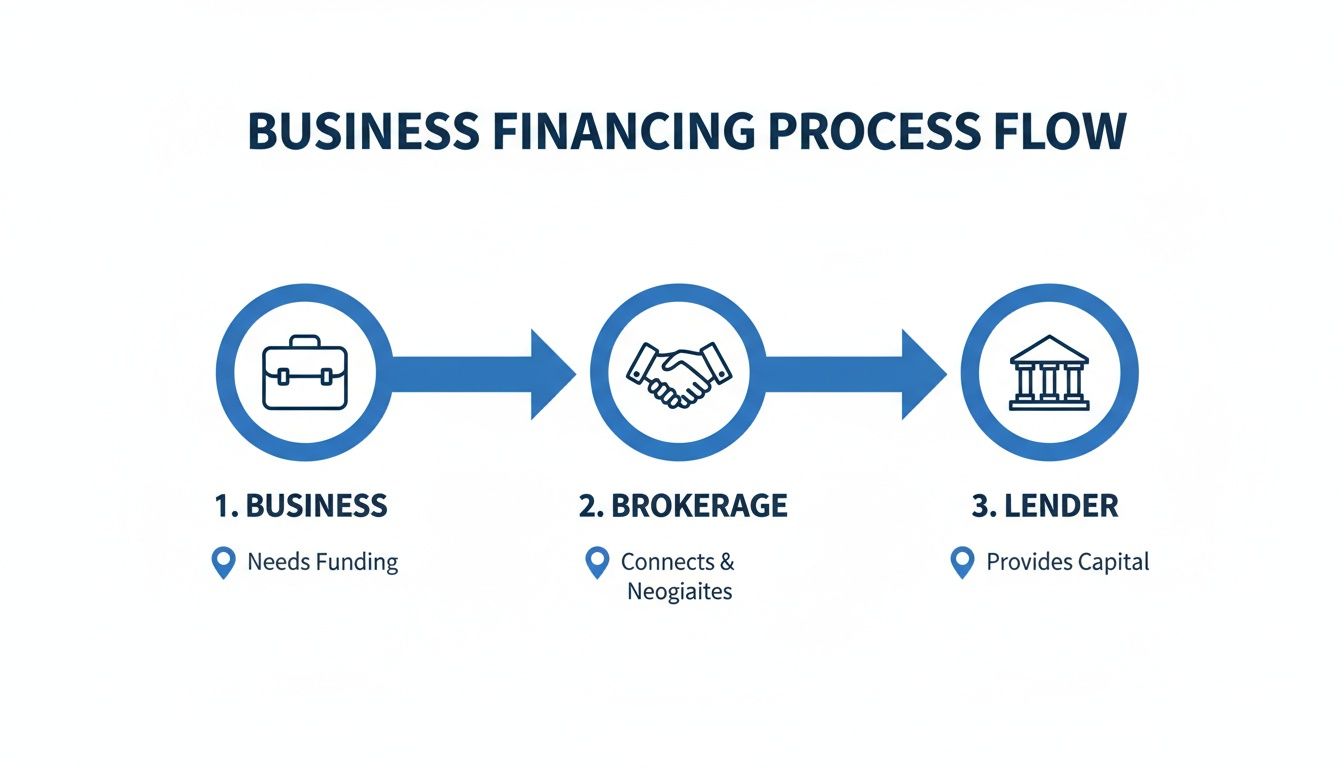

This flowchart maps out the typical journey for securing this type of funding.

As you can see, a specialist brokerage like FSE is a vital link in the chain, matching a business's urgent capital needs with the right lender who can deliver on time.

Open vs. Closed Bridging Loans

Bridging loans come in two main flavors, and the difference all comes down to the certainty of your repayment plan, or what we in the industry call the exit strategy.

Closed Bridge Loans: This is the more secure of the two. It means you have a legally binding, guaranteed way to repay the loan already lined up. Think a signed contract for the sale of a property or a concrete, approved offer for a long-term mortgage. Lenders love this certainty, and because it’s lower risk for them, you’ll often get better terms.

Open Bridge Loans: This type offers more flexibility. You have a solid plan to repay the loan—like renovating and selling the asset or refinancing down the line—but the final details aren't locked in with a contract just yet. Lenders see this as a slightly higher risk, so you can expect the interest rates to be a touch higher to compensate.

No matter which type you need, having a believable and well-documented exit strategy is the single most critical part of any bridging loan application.

The Financial Nuts and Bolts

To really get a feel for how these loans work, you have to understand their unique financial structure. They aren't just smaller versions of a traditional loan; their costs and terms are designed specifically for short-term, strategic use.

A well-structured commercial bridging loan can be the difference between securing a competitive property deal and missing out. It's not just short-term finance; it’s a strategic tool for acting decisively in fast-moving markets.

The star of the show in any bridging deal is the property itself. A lender’s primary concern is its value, as that asset is their security. This asset-first approach is why the borrower’s credit history and business revenue, while still important, aren't scrutinized nearly as heavily as they would be at a traditional bank.

Typical Commercial Bridging Loan Terms at a Glance

The table below provides a quick snapshot of the common terms and costs you'll encounter. It’s a handy reference for seeing if a bridging loan aligns with your project's financial realities.

| Loan Feature | Typical Range or Condition |

|---|---|

| Loan-to-Value (LTV) | 60% to 75% of the property’s market value. |

| Loan Term | 3 to 24 months (sometimes longer in special cases). |

| Interest Rates | 0.5% to 1.5% per month. |

| Interest Payment | Often "rolled-up" and paid at the end of the term. |

| Origination Fee | 1% to 2% of the total loan amount, paid upfront. |

| Exit Fee | Sometimes ~1% of the loan amount, paid upon repayment. |

| Underwriting Focus | Primarily on the property value and the exit strategy. |

| Funding Speed | Can be as fast as 5-10 business days from application. |

As you can see, while the monthly costs are higher than a long-term mortgage, the structure is built for short-term holds where speed and access to capital are paramount. These components are the price of agility in the commercial property market.

When to Use a Commercial Bridging Loan

Knowing how a commercial bridging loan works is one thing, but knowing exactly when to use one is what really sets sharp investors apart. These aren't your everyday business loans; they're tactical tools for specific, time-crunched situations where conventional financing just can't keep up.

Think of it like this: a traditional commercial mortgage is a cargo ship. It’s reliable, carries a heavy load, and is perfect for a long, planned journey. A bridging loan, on the other hand, is a speedboat—built for speed and agility, getting you to a nearby opportunity before anyone else can even leave the dock. It’s your financial speedboat.

Seizing Time-Sensitive Purchase Opportunities

By far the most common reason for a commercial bridging loan is to snap up a property when the clock is ticking. In these high-pressure scenarios, the slow, methodical pace of a high-street bank becomes a major liability.

Property Auctions: This is the classic example. You win a great property at auction, but the hammer falls and you have 28 days or less to complete the purchase. A standard mortgage application can’t even get through underwriting in that time. A bridging loan gives you the cash to secure the asset, buying you precious time to arrange longer-term financing.

Below Market Value Deals: Opportunity knocks, but it doesn't wait around. Maybe you've found a distressed property or a motivated seller who needs cash now. These deals offer incredible value but are gone in a flash. A bridge loan empowers you to act decisively, close the deal quickly, and lock in that built-in equity.

Bridging Gaps in the Property Chain

For any business moving or expanding, the dreaded "property chain" can bring everything to a grinding halt. A bridging loan is the perfect tool for breaking free and taking back control.

Imagine you’ve found the perfect new warehouse for your expanding business, but the sale of your current facility hits an unexpected snag. Without the proceeds from that sale, you’re about to lose out on the new property and your entire growth plan is on hold.

This is where a bridging loan commercial solution steps in. It provides the funds to buy the new warehouse right away, completely separate from the sale of your old one. Once your original property finally sells, you simply use that money to pay off the bridge loan.

This strategic move prevents one delay from derailing your entire expansion. It’s about maintaining momentum and insulating your business from the unpredictable actions of others in a transaction.

Funding Renovations and Redevelopment Projects

Most traditional lenders get nervous when they see a property that needs serious work. They much prefer lending against stable, move-in-ready assets, not buildings that are uninhabitable or need a complete overhaul.

This creates a frustrating catch-22 for developers: you need funds to fix up the property, but lenders won't give you funds until it's fixed.

A commercial bridging loan cuts right through that problem. Lenders in this space are experienced with "fix-and-flip" or value-add projects. They can provide the capital to both purchase and renovate a property, basing their lending on its projected after-repair value (ARV). Once the work is done and the property is refinanced or sold, the developer pays back the loan.

This approach is becoming more and more popular. Recent market data shows that in the first quarter of 2025, property investment became the number one reason for taking out a bridge loan, accounting for 23% of all transactions. This trend really shows how investors are using short-term capital to drive their growth. You can dive deeper into these bridging finance trends to see how the market is evolving.

In all these cases, the common thread is a temporary cash-flow gap that stands between an investor and a great opportunity. A commercial bridging loan is the specialized financial tool designed to cross that gap and turn a potential roadblock into a profitable success.

How to Qualify for a Commercial Bridging Loan

Getting a commercial bridging loan is a whole different ballgame compared to traditional bank financing. Forget the mountains of paperwork and the intense focus on years of financial history. Bridging lenders cut right to the chase, zeroing in on two things that really matter: the value of your property and your plan for paying them back.

This approach is all about the deal itself. If you've got a solid commercial asset and a clear, believable exit strategy to settle the loan quickly, you're already most of the way there. It’s a process built for speed and opportunity, not for dissecting your past.

What Lenders Really Care About

At their core, bridging lenders are asset-based. They aren't as concerned with your company's P&L statements as they are with the quality of the real estate that's securing their investment. That means their underwriting is lean and focused on a few key areas.

To get the green light, you'll need to make a strong case for the following:

The Property (Your Collateral): This is everything. Lenders will require a professional appraisal to get a clear picture of the property's current market value. The loan you get will be a percentage of this figure, known as the Loan-to-Value (LTV).

The Exit Strategy: This is the absolute make-or-break part of your application. You must have a credible, documented plan to repay the loan. This could be anything from selling the property to refinancing it with a more permanent commercial mortgage.

The Story of the Deal: Why this property? Why now? Lenders want to understand the opportunity you're seizing. A clear, compelling story that explains why you need funds fast and how the project will succeed goes a long way.

The entire philosophy behind qualifying for a bridge loan is this: the lender is betting on the asset, not just the borrower. Your job is to prove that the property is a great investment and you have a rock-solid path to repayment.

This streamlined focus is exactly why these loans can be approved so quickly. The market for this kind of short-term funding is booming. In the UK, for instance, application volumes jumped 11% in the second quarter of 2025, while average LTVs remained a healthy 54%. Processing times even hit a record low of 32 days, a level of efficiency we aim to replicate for our clients in the US. You can dig deeper into these trends by checking out the latest bridging finance market reports.

Getting Your Paperwork in Order

While the process is much leaner than a bank's, you'll still need to provide some essential documents to get your application over the line. Having these ready from the start will make a huge difference in how fast you get funded.

Here’s a typical checklist:

- Purchase Agreement: If you're buying a property, this is the legal document that lays out all the terms of the sale.

- Property Appraisal: Lenders need an independent valuation to set the LTV and understand their risk exposure.

- Proof of Your Exit Strategy: This isn't just a concept; you need to back it up. It could be a pre-approval letter for refinancing, a signed contract to sell another asset, or a detailed business plan for a renovation project.

- Borrower Information: Just the basics about you and your business entity for the lender's due diligence checks.

This is where working with an experienced brokerage like FSE really pays off. A good advisor knows exactly how to package your application to catch a lender's eye, framing the deal in the best possible light. This not only boosts your odds of approval but also helps you land the best rates and terms on the market.

Comparing Bridging Loans to Other Financing

Picking the right financing is a lot like choosing the right tool for a construction job. You wouldn't use a sledgehammer where a scalpel is needed. A bridging loan is a highly specialized instrument, and understanding how it stacks up against other options is key to making a smart, strategic decision for your business.

Each funding type has its own purpose, speed, and cost. A traditional commercial mortgage is built for long-term stability, while a line of credit offers flexible access to cash. A bridging loan, on the other hand, is engineered for one thing: rapid deployment to seize an immediate opportunity.

Commercial Bridging Loans vs. Traditional Mortgages

The single biggest difference between a bridging loan and a traditional commercial mortgage comes down to time.

A conventional mortgage from a bank is a marathon. The process can drag on for months, involving deep underwriting, mountains of paperwork, and rigid borrower criteria. They are meant to be permanent, long-term financing solutions, with terms typically lasting 10 to 25 years.

A bridging loan is a sprint. Its entire purpose is to get you across a short-term funding gap in days, not months. While traditional mortgages offer lower interest rates, they’re simply too slow for situations like an auction purchase or an urgent property acquisition where you need to move fast.

A well-structured bridging loan acts as the essential first step, securing the asset quickly. The traditional mortgage then becomes the exit strategy, refinancing the bridge loan into a stable, long-term payment structure once the property is secured and stabilized.

Bridging Loans vs. Business Lines of Credit

Think of a business line of credit (LOC) as a financial safety net. It gives you a revolving credit limit you can draw from as needed and pay back over time. This makes it perfect for managing day-to-day cash flow, buying inventory, or covering unexpected operational expenses.

However, a line of credit isn't built for large, one-time asset purchases. The credit limits are often too low for acquiring a commercial property, and the approval process still focuses heavily on the business's overall financial health and revenue history, which takes time. A bridging loan delivers a single, substantial lump sum specifically for a real estate transaction, with the property itself as the primary collateral.

Commercial Bridging Loans vs. Hard Money Loans

This is where the lines get a bit blurry, as both are short-term, asset-based lending options. In fact, many people in the U.S. market use the terms interchangeably. Both prioritize the property's value over the borrower's credit score and are offered by private lenders, not big banks.

The main distinction often lies in the source of funds. Hard money loans are almost always funded by private individuals or small groups of investors. Bridging loans, while also from private sources, may come from more established institutional or specialized lending firms. For the borrower, though, the practical experience is very similar: fast funding, short terms, and a laser focus on the real estate asset.

Comparing Commercial Financing Options

To help you see the differences at a glance, we've put together a simple comparison. This table lays out a side-by-side look at bridging loans against other popular business financing to help you choose the right solution.

| Financing Type | Speed to Fund | Typical Term | Primary Use Case |

|---|---|---|---|

| Commercial Bridging Loan | 5-10 business days | 3-24 months | Acquiring property quickly, auction purchases, funding renovations. |

| Traditional Mortgage | 2-4 months | 10-25 years | Long-term ownership of a stabilized commercial property. |

| Business Line of Credit | 1-3 weeks | Revolving | Managing daily cash flow, inventory, operational costs. |

| Hard Money Loan | 5-10 business days | 6-24 months | Similar to bridging; often for fix-and-flip or distressed properties. |

Ultimately, the right choice depends entirely on what you're trying to accomplish. If you need to lock down a valuable asset before a competitor does or before the opportunity disappears, a bridging loan provides the speed and firepower that other financial tools simply can't deliver.

Navigating Risks and Planning Your Exit

Let’s be direct: while a commercial bridging loan gives you incredible speed and flexibility, it’s a high-stakes financial tool. It comes with its own rules and risks, and any good partner will be upfront about them. The higher interest rates aren't a surprise—they're the price you pay for a lender shouldering more risk to get capital in your hands in days, not months.

The real danger isn't the cost itself, but the tight timeline. These loans are a temporary fix, a bridge to somewhere else. Their success depends entirely on one thing: your exit strategy. Without a crystal-clear, believable plan to pay back the loan, you could find yourself in a very tough spot.

Defining Your Exit Strategy

Your exit strategy is your road map for repaying the bridging loan in full by the end of its term—usually somewhere between 3 and 24 months. This can't be just a hopeful idea. It has to be a concrete, actionable plan that convinces the lender you know exactly what you’re doing. In fact, a strong exit is the cornerstone of any successful bridging loan commercial application.

Lenders typically see two main paths for a solid exit:

Refinancing with Long-Term Finance: This is the go-to strategy for most borrowers. You use the bridge loan to quickly acquire or stabilise a property, and then you refinance onto a traditional commercial mortgage with a much lower interest rate to pay off the bridge. A lender will want to see proof that this is a realistic goal, like a pre-approval letter or a strong history of securing similar financing.

Selling the Asset: If you're a "fix-and-flip" investor or a business relocating, the plan is simply to sell the property before the loan is due. In this scenario, lenders need to see a realistic market appraisal and a sound sales strategy. They have to be confident you can sell the property for a profit within the allotted time.

The Consequences of a Failed Exit

When an exit strategy falls apart, the consequences can be serious. If you can't repay the loan on schedule, you could be hit with default penalties, even higher interest rates, or, in the worst-case scenario, the lender could repossess the property to get their money back. This isn't meant to scare you—it's just the reality of how asset-backed lending works.

A well-planned bridging loan can be the key to jumping on a great property deal you'd otherwise miss. But it's a powerful tool that demands a solid and realistic repayment plan from day one. Working with someone who knows the ropes is vital to managing the risks.

This is exactly why your exit plan isn't the last thing you think about; it should be the very first. A skilled brokerage like FSE will start by helping you build a viable exit plan. It’s the best way to ensure your application not only gets approved but is structured for a successful and profitable outcome from the get-go.

Your Top Questions About Commercial Bridging Loans, Answered

Jumping into the world of commercial finance can feel a bit overwhelming, and it's natural to have questions. We've put together answers to some of the most common things business owners and investors ask about commercial bridging loans to give you the clarity you need.

How Quickly Can I Actually Get Funded?

This is where bridging finance truly shines. Forget the months-long waiting game with traditional banks. For a straightforward deal with a solid asset as collateral and a complete application, funding can land in your account in as little as 24 to 72 hours.

Of course, not every deal is simple. If the transaction has a few more moving parts or requires a detailed property appraisal, you might be looking at a week or two. Even then, it’s a world of difference compared to the standard lending process.

Is a Bad Credit Score a Deal-Breaker?

Not always. One of the biggest misconceptions is that a low credit score automatically disqualifies you. With bridging loans, the lender's focus is less on your past credit history and more on the quality of the deal in front of them.

They're primarily concerned with two things: the value of the property you're offering as security (the loan-to-value ratio) and the viability of your plan to repay the loan. If you have a strong asset and a believable exit strategy, many lenders will work with you even if your credit isn't perfect.

What Is a Typical Exit Strategy?

An exit strategy is simply your plan for paying back the loan. It's not an afterthought; it's the core of your application. The lender needs to see a clear, realistic path for you to repay the debt at the end of the short term.

Your exit strategy is the roadmap you present to the lender. It proves you’ve thought through the entire project lifecycle and gives them the confidence to back your deal, knowing their capital is secure.

The two most common exit strategies are:

- Refinancing: You use the bridging loan to acquire or improve a property, and once the project is complete or the property is stabilized, you refinance onto a traditional, long-term commercial mortgage. The funds from that new loan pay off the bridge loan.

- Selling the Property: This is the go-to plan for most fix-and-flip projects or when a business is simply moving locations. You use the bridge loan to buy and/or renovate the asset, and the proceeds from its eventual sale cover the loan repayment, hopefully leaving you with a tidy profit.

Are Bridging Loans More Expensive Than Traditional Loans?

Yes, and it’s important to be upfront about that. The interest rates and fees for a commercial bridging loan are higher than what you'd find with a conventional bank loan.

Think of it as paying a premium for speed and convenience. You're getting access to capital incredibly fast to solve an immediate problem or jump on a time-sensitive opportunity. They are a powerful tool for short-term needs, not a substitute for long-term financing. The idea is to use them strategically to unlock a deal whose return on investment will far outweigh the borrowing costs.

Ready to bridge the gap and seize your next commercial opportunity? The team at FSE - Funding Solution Experts specializes in connecting businesses like yours with the fast, flexible capital you need when traditional lenders can't deliver. Apply in minutes and get a preliminary decision in 24 hours.