When choosing between a business credit line vs loan, the decision depends on your needs. Do you require flexible, ongoing cash access for daily expenses, or a single, large sum for a specific investment? Answering this helps align your financing with your business strategy.

A Quick Comparison

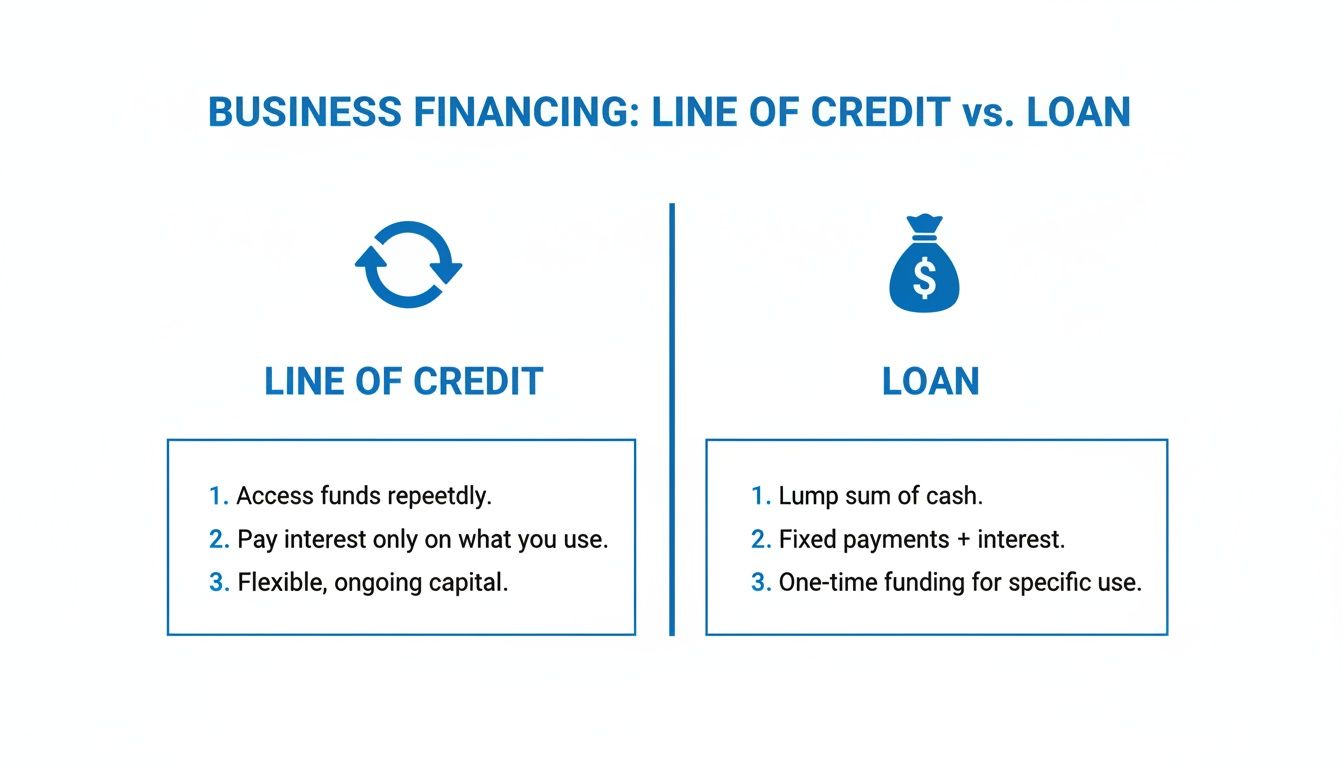

Think of a business line of credit as a financial safety net you can use anytime. A business term loan is a one-time cash injection for a planned purchase. For example, a restaurant owner might use a line of credit to manage cash flow during slow seasons, covering payroll and other costs. Lenders often have more flexible requirements for lines of credit, sometimes needing just six months in business and $50,000 in revenue. Term loans are stricter, often requiring two years of history and higher revenue. This flexibility is key, especially given low approval rates for small business credit.

As shown, a line of credit is revolving, while a term loan is a direct, one-time payment.

Key Differences

| Feature | Business Line of Credit | Business Term Loan |

|---|---|---|

| Structure | Revolving credit limit to draw from, repay, and reuse. | One-time lump sum of cash. |

| Best Use | Working capital, payroll, unexpected costs. | Major purchases like equipment or real estate. |

| Repayment | Pay interest only on the amount drawn. | Fixed monthly payments. |

| Flexibility | High. Ongoing access to funds. | Low. Funds are for a specific purpose. |

This table simplifies the choice by focusing on how funds are delivered and repaid.

How They Work

A business line of credit works like a credit card for your company. You get a set limit, say $100,000, and can draw funds as needed. You only pay interest on what you use. If you borrow $20,000, you pay interest on that amount alone. This is ideal for managing cash flow.

A business term loan is a one-time deal. If approved for $100,000, you get the full amount upfront. Interest accrues on the entire principal immediately, and you make fixed monthly payments. Once repaid, the loan is closed.

Comparing Costs

A term loan usually has a fixed interest rate, making payments predictable. A line of credit often has a variable rate tied to market benchmarks. With a term loan, interest starts on the full amount from day one. With a line of credit, you only pay interest on what you’ve used. Fees like origination, annual, or draw fees also apply.

When to Choose Which

A line of credit is best for short-term, unpredictable needs like managing seasonal demand or bridging payroll gaps. A term loan is for planned, one-time investments like buying major equipment or expanding your business. Your choice depends on what you need the money for and your business's cash flow. For more on these options, check resources from American Express and data from places like Bankrate.

Final Decision Checklist

- What’s the money for? A large, single purchase suggests a term loan. Ongoing, unpredictable costs point to a line of credit.

- What’s your timeline? Lines of credit are often approved faster, sometimes within 24-48 hours. Term loans take longer.

- What's your cash flow? Consistent revenue suits a term loan’s fixed payments. Variable income is better matched with a line of credit's flexible repayment.

Frequently Asked Questions

Can I have both a business loan and a line of credit?

Yes, many businesses use a loan for large investments and a line of credit for operational flexibility.

Which is better for building business credit?

Both are effective if the lender reports to credit bureaus. Consistent, on-time payments are key.

Is collateral required?

Not always. Many lenders offer unsecured options based on your business's cash flow.

When traditional banks create roadblocks, FSE - Funding Solution Experts opens doors. Our advisors specialize in matching your unique business needs with the right funding solution from our extensive network of over 50 lenders, ensuring you get the fast, flexible capital you need to grow. Find out how we can help by visiting https://www.fseb2b.com.