Navigating business financing as a startup can feel like you've been handed a map with a dozen different paths, each leading to a different destination. The right route depends entirely on where you want your business to go. For most founders outside the Silicon Valley bubble, options like working capital loans and merchant cash advances offer a direct line to fast, accessible capital—something venture capital and big banks rarely provide.

Understanding the Modern Startup Funding Landscape

For most new entrepreneurs, the world of business financing feels like an exclusive club they can't get into. All we hear about are massive, headline-grabbing funding rounds for AI and tech startups, which creates this myth that venture capital (VC) is the only "real" way to grow. But that media hype paints a very narrow, and frankly, misleading picture.

The reality? For the vast majority of businesses in essential industries like construction, logistics, and retail, the traditional funding paths are often dead ends. Big banks can be painfully slow and allergic to risk, while VCs are hunting for a very specific type of unicorn—a hyper-growth, high-risk model that just doesn’t fit most companies. It’s no wonder so many founders feel stuck.

Navigating Beyond the Hype

To make a smart decision, you have to understand the environment you're operating in. Right now, the market is incredibly lopsided. For example, the United States currently pulls in a staggering 64% of all global startup funding, with a huge chunk of that—nearly half of all worldwide venture capital—being poured into artificial intelligence. You can get a deeper look at the numbers in this global startup funding report.

This heavy focus on tech puts entrepreneurs in every other sector in a tough spot, forcing them to find different ways to fuel their growth.

This guide is designed to cut through that noise. We’re laying out a clear, practical roadmap to the financing options that actually work for businesses outside the VC bubble. It’s a primer to demystify the journey and help you find the right capital for your real-world needs, without all the jargon and complexity. The trick is to match the funding to your specific situation.

Your Roadmap to Smart Capital

We're going to break down a range of solutions perfectly suited for the kinds of businesses that banks and VCs tend to ignore. That means getting to the bottom of the fundamental differences between major funding types so you can see exactly which one aligns with your goals. The whole point is to give you the knowledge you need to confidently go after the capital that will help you win.

The best business financing for startups isn't about chasing the biggest check; it's about securing the right capital at the right time with terms that support sustainable growth, not hinder it.

This means we'll be looking at options that care about your business's actual performance—things like your monthly revenue and how long you've been operating—instead of an flawless credit score or a flashy pitch deck promising the moon.

Decoding Your Three Core Financing Paths

When you start looking for startup financing, the sheer number of options can feel overwhelming. It’s easy to get lost in a sea of jargon. But really, it all boils down to three fundamental paths, and each one comes with a distinct set of trade-offs.

Think of it like planning a cross-country trip. You could drive, fly, or take a train. Each gets you to your destination, but the speed, cost, and what you sacrifice along the way are completely different. Securing capital for your business works much the same way. The key is to match the funding vehicle to your business model, your growth stage, and what you need right now.

Path 1: Debt Financing — The Traditional Route

Debt financing is the one most people are familiar with. We're talking about traditional bank loans and loans backed by the Small Business Administration (SBA). At its heart, it’s simple: you borrow money that you agree to pay back, with interest, over a set period.

The biggest upside here is that you keep 100% ownership of your company. You aren't selling off a piece of your business; you're just "renting" the capital you need to grow. For founders who want to maintain absolute control over their vision, this is a huge plus.

Of course, that control comes with a catch. Lenders, especially big banks, are famously risk-averse. They’ll want to see a strong credit history, a few years in business, and often require personal collateral to back the loan. For a brand-new startup, meeting these strict requirements is often a non-starter. The process itself can also be a marathon, sometimes taking months from application to funding.

Path 2: Equity Financing — Selling a Piece of the Pie

With equity financing, you’re not taking on debt. Instead, you're selling a percentage of your company to an investor in exchange for cash. This is the world of angel investors and venture capitalists (VCs). They aren't looking for loan repayments; they're betting on your company's future success and want a piece of the potential upside.

The main draw is the access to massive amounts of capital without the pressure of a monthly loan payment hanging over your head. Investors are often willing to fund high-risk, high-reward ideas that a bank would never touch. On top of the money, a great investor can also bring invaluable industry connections and expertise to the table.

But the trade-off is a big one: you're giving up ownership and a degree of control. Each time you take on equity, your own stake in the company you built gets smaller. VCs also have very specific expectations—they're hunting for businesses that can deliver explosive, 10x returns in just a few years. This model is a fantastic fit for a certain type of high-growth tech company, but it's a poor match for the vast majority of small businesses.

Path 3: Alternative Financing — The Modern Middle Ground

Alternative financing has emerged to fill the huge gap left by slow, traditional banks and highly selective VCs. This category includes more nimble products like working capital loans, lines of credit, and merchant cash advances (MCAs). These options are built for one thing: getting capital into the hands of business owners quickly and efficiently.

This path operates on a different philosophy. Lenders in this space care more about your business's real-time performance—your recent revenue and cash flow—than they do about your personal credit score or how many years you've been in business.

The core principle of alternative financing is accessibility. Approval is based on the health of your business today, not just its history, allowing founders to get funded in as little as 24 hours.

This speed makes it a powerful tool for grabbing time-sensitive opportunities, like buying inventory at a deep discount or covering an unexpected operational expense. While the cost of capital might be higher than a five-year bank loan, the value is in the fast, straightforward process that’s tied directly to your business performance.

To help you see the bigger picture, here’s a simple breakdown of how these three paths stack up against each other.

Comparing Key Startup Financing Categories

| Financing Type | What You Give Up | Typical Speed | Best For |

|---|---|---|---|

| Debt Financing | Control over cash flow (via loan payments) | Slow (Weeks to Months) | Established businesses with strong credit and collateral seeking predictable, low-cost capital. |

| Equity Financing | Ownership and some decision-making control | Slow (Months to a Year+) | High-risk, high-growth startups (often tech) with the potential for massive scale and a big exit. |

| Alternative Financing | A higher cost of capital | Fast (24-72 Hours) | Businesses of all stages needing quick access to capital for opportunities or short-term needs. |

Each path has its place. The goal isn't to say one is universally "better," but to understand the trade-offs so you can choose the one that makes the most sense for your specific situation.

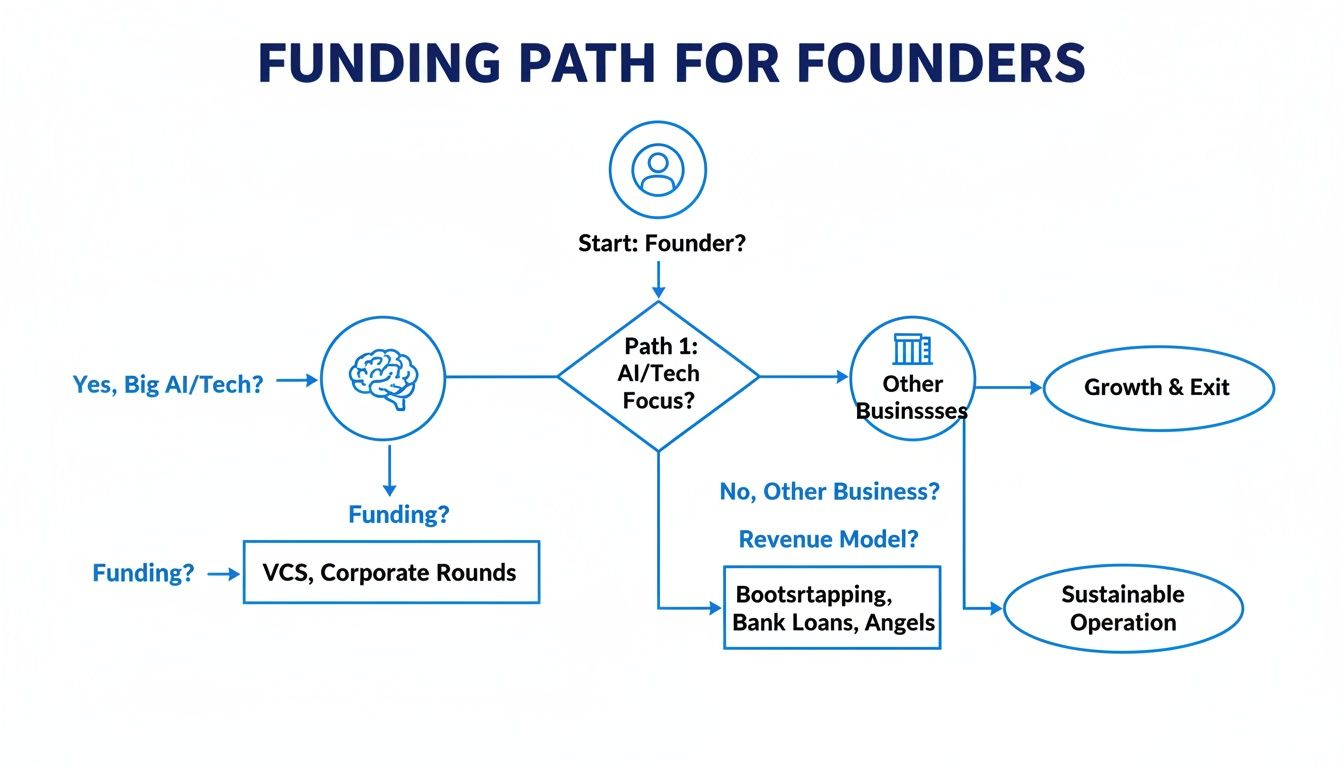

This decision tree gives you a visual of how different types of businesses might approach these funding routes.

As you can see, while venture capital gets a lot of media attention, it’s really geared toward a narrow slice of the startup world. Most businesses will find their best fit within the debt and alternative financing arenas. Understanding these fundamental differences is the first, most critical step toward making a smart financing decision for your company.

The Truth About Venture Capital and Equity

Venture capital gets all the headlines. We've all seen the dramatic TV pitches and read about sky-high valuations. This is equity financing, where you trade a piece of your company for cash, and it's easily one of the most misunderstood paths a founder can take. Getting that big check isn't just about the money; it's about entering into a very specific, demanding partnership.

Think of a VC investor as a supplier of rocket fuel. They provide an incredible amount of power, but it's only useful for rockets built to reach the moon at blistering speeds. If your goal is to build a reliable, profitable, and sustainable local delivery business, that fuel isn't just unnecessary—it’s the wrong tool for the job. VCs aren't just funders; they become co-owners who need a massive return on their investment, often aiming for 10 to 20 times their initial capital within a tight 5-7 year window.

This expectation changes everything. It means VCs are hunting for hyper-scalable businesses that can completely dominate enormous markets. They need to see a believable story of how your startup will either be acquired for a fortune or go public. This is exactly why VC money is so heavily concentrated in just a handful of industries.

The High-Stakes World of VC Funding

The competition for venture capital is brutal. Investors are making calculated bets that one or two companies in their portfolio will become massive hits and pay for all the others that fail. Because of this, only a tiny fraction of businesses that seek VC funding ever get it. The data paints a very clear picture: the money flows to very specific sectors and locations, leaving most small businesses out of the conversation entirely.

Just look at the artificial intelligence space. A recent report revealed that AI startups pulled in an incredible $89.4 billion in global venture capital. That's 34% of all VC investment, even though these companies represented only 18% of all funded startups. This trend, with North America leading the charge at $42.6 billion, shows just how laser-focused VCs are. You can dig deeper into these numbers by exploring the latest data on AI's impact on startup funding.

This intense focus means that if your business is in an industry like home services, hospitality, or local retail, the VC route is almost certainly a dead end. Chasing this kind of funding can become a massive distraction, draining your time and energy with very little chance of paying off.

Understanding the Equity Funding Stages

For those few startups that do fit the mold, funding isn’t a one-and-done deal. It’s a journey that happens in structured rounds, or "stages," with each one tied to hitting major growth milestones.

- Seed Stage: This is the first real money in. It often comes from angel investors or early-stage VCs and is used to prove the concept, build a minimum viable product (MVP), and do some initial market research.

- Series A: After the startup has a working product, some early customers, and a solid business model, it raises a Series A round. This cash is for scaling up the team, refining the product, and expanding its customer base.

- Series B: By this point, the company is on solid ground and ready to grow aggressively. Series B funding is poured into major expansion, like moving into new cities or countries, acquiring top-tier talent, and ramping up sales and marketing.

- Series C and Beyond: These are the big leagues. Later-stage rounds are for successful, mature startups that are often getting ready for an IPO or a major acquisition. The goal here is to cement market dominance and push toward profitability.

Venture capital is a specialized tool for a small subset of startups. For the majority of small and medium-sized businesses, true growth capital is found through more accessible and realistic financing options.

At the end of the day, you have to be brutally honest with yourself. Does your business model truly align with the high-risk, high-return world of equity investors? For most entrepreneurs, the smartest path to growth isn't selling off pieces of their company, but finding the right financing to support steady, sustainable success.

Exploring Fast and Flexible Alternative Financing

When you're running a startup, opportunities and emergencies don't wait for a bank's lengthy approval process. Waiting weeks or even months for a traditional loan just isn't realistic. This is precisely where the world of alternative financing comes in, offering a lifeline built for speed and flexibility. It's a category of business funding that looks at your company's current health, not just a perfect financial history.

Think of it like this: traditional banks are like massive cargo ships. They're reliable and cost-effective for long, planned journeys but are incredibly slow to change course. Alternative lenders are more like speedboats—nimble, quick, and able to get you exactly where you need to go, right when you need to be there. This agility lets you jump on time-sensitive opportunities, like a big inventory discount or an urgent equipment repair, without missing a beat.

With these options, approvals can come through in as little as 24 hours, with the money in your account not long after. How? Because these lenders care more about your real-time performance, like consistent monthly revenue, than a flawless credit score from years past.

Working Capital Loans

A working capital loan is a straightforward infusion of cash meant to cover your day-to-day operational costs. It’s not for buying a new building or making a long-term investment; it's the financial fuel that keeps your business engine running smoothly. The versatility of these loans makes them an absolute lifesaver for managing cash flow.

Here’s a real-world scenario: A landscaping company lands a major commercial contract. They need to hire two new crew members and buy extra supplies now, but the client won't pay for another 60 days. A working capital loan provides the immediate cash to get the job done, bridging that revenue gap so they can deliver without a hitch.

Merchant Cash Advances (MCAs)

A Merchant Cash Advance, or MCA, isn't a loan in the classic sense. Instead, a provider advances you a lump sum of cash in exchange for a slice of your future credit and debit card sales. The payback is tied directly to your daily revenue—on busy days you pay back more, and on slow days you pay back less.

This flexible repayment model makes MCAs a fantastic fit for businesses with seasonal or fluctuating income, like restaurants and retail shops.

Picture this: A popular coastal restaurant needs to stock up on fresh seafood and bring on extra staff for the summer tourist rush. An MCA gives them the capital to prepare. As summer sales take off, the advance is paid back automatically from their daily card sales, never putting a strain on their slower off-season months.

Equipment Financing

For so many startups, having the right gear is non-negotiable. Equipment financing lets you purchase the machinery, vehicles, or tech you need by using the asset itself as collateral. This is a huge advantage, as you don’t have to pledge other business or personal assets to get the funding.

This type of financing is a powerful tool for growth, letting you scale operations and take on bigger jobs without a massive upfront capital drain. The loan terms are typically structured to match the equipment's expected lifespan, which creates a predictable payment schedule.

For example: A logistics startup must add two more delivery trucks to its fleet to keep up with demand. Through equipment financing, they get funding specifically for those trucks. The vehicles themselves secure the loan, allowing the company to expand its delivery capacity and revenue potential immediately.

Business Lines of Credit

A business line of credit is one of the most flexible financing tools you can have in your corner. Unlike a term loan where you get a single lump sum, a line of credit gives you access to a pool of capital that you can draw from whenever you need it. Crucially, you only pay interest on the funds you actually use.

Think of a line of credit as your financial safety net. It’s the peace of mind knowing you have capital ready for unexpected costs or sudden growth opportunities, giving you ultimate control over your cash flow.

Once you repay what you've borrowed, the full credit line is available to you again. Its revolving nature makes it the perfect long-term solution for managing ongoing, unpredictable cash flow needs. It's ideal for businesses that need a buffer for emergencies or want to be ready to act fast when a new opportunity comes knocking.

How to Get Your Business Funding Ready

When you need capital, speed is everything. Forget the old days of writing a 50-page business plan just to get a meeting. Today, getting business financing for your startup is all about being prepared. Having your key documents organized and ready to go is your fast pass to a smoother approval process.

Alternative lenders, in particular, move at the speed of business because they focus on the vital signs of your company's health right now. This means you need to paint a clear, immediate picture of your financial performance. Nail this from the start, and you could see funds in days, not weeks.

Your Essential Funding Checklist

Think of this as your financing "go-bag." When you have these documents ready, you show lenders you're a serious, organized owner, which helps them make a decision that much faster.

Here’s exactly what most lenders will want to see:

- Recent Bank Statements: Pull your last three to six months of business bank statements. This gives a real-time look at your cash flow, showing your average daily balance and monthly deposits.

- Proof of Revenue: This could be a recent profit and loss statement or, if you take credit cards, your merchant processing statements. It’s all about backing up the revenue numbers your bank statements suggest.

- Business Identification: Have your business license, articles of incorporation, and Employer Identification Number (EIN) handy. These documents simply prove your business is legitimate and registered correctly.

- Proof of Ownership: A driver's license or another government-issued photo ID is all that's needed to verify who owns the business.

Rounding up these items ahead of time clears the biggest hurdles right out of the gate and signals to lenders that you’re reliable and ready for business.

Meeting Key Eligibility Benchmarks

Beyond the paperwork, lenders have a few core benchmarks they look at to gauge risk. While the specifics can vary between funding partners, they are a world away from the rigid requirements you'd find at a traditional bank.

The goal isn't perfection; it's demonstrating stability and momentum. Lenders want to see a business with consistent, predictable revenue that shows it can manage its finances and support repayment.

Most alternative lenders are looking for these key indicators:

- Time in Business: Most programs need you to have been operating for at least one year. This tells them you’ve navigated the initial startup hurdles and have a real track record.

- Monthly Revenue: A common baseline is $10,000 or more in monthly revenue. This figure gives lenders confidence that you generate enough cash flow to handle your existing obligations and a new payment.

- Credit Score: Your personal credit score still matters, but it's not the deal-breaker it often is with banks. Lenders in this space often work with scores that traditional institutions would decline, placing much more weight on your actual business performance.

Meeting these basic requirements is your first major step toward unlocking the fast, flexible business financing for startups you need. With your documents in order and these benchmarks in mind, you can walk into the application process with confidence and get the capital your business needs to grow.

Finding the Right Funding Partner

Once you’ve got a handle on your financing options, a new question pops up: where do you actually go to get the money? You really have two choices. You can go it alone, spending your own time researching lenders and filling out application after application. Or, you can partner with a commercial finance brokerage.

Think of a broker as a seasoned guide on your funding expedition. Instead of you sinking countless hours into finding a lender who gets your industry and is likely to say yes, a broker does all that legwork. They have a deep network of lending partners, opening the door to dozens of options with just one simple application.

This isn't just a time-saver. It's a strategic move that can give you a real competitive edge.

Creating Leverage in the Lending Marketplace

When a broker shops your application to multiple lenders at once, it essentially creates a competitive market for your business. Lenders have to vie for the chance to fund you, which naturally leads to better rates, more flexible terms, and a much higher chance of getting approved. You’re no longer just another applicant; you’re a hot commodity.

This is a game-changer, especially for businesses that traditional banks tend to ignore. While you might see headlines about AI startups raising a staggering $150 billion, that's a different universe for most small businesses in construction, hospitality, or retail. Learn more about the latest AI funding trends here.

For these real-world companies, a broker is a lifeline. They can match you with one of over 50 partners specializing in your field, often securing a decision within 24 hours.

An Advocate in Your Corner

Maybe the biggest plus is having a dedicated expert on your side. Trying to compare multiple loan offers is genuinely confusing. You're juggling different rates, hidden fees, and tricky repayment structures. A good broker cuts through the noise and lays everything out in a clear, apples-to-apples comparison.

A finance broker acts as your advocate, translating the fine print and ensuring you understand the true cost of capital. Their goal isn't just to find you a loan—it's to find you the right loan that supports your business's long-term health and growth.

This partnership turns the daunting search for startup financing into a straightforward, strategic process. It ensures you lock in the best possible deal so you can get back to what you do best—running your business.

Got Questions About Startup Financing? We’ve Got Answers.

Stepping into the world of business financing can feel like learning a new language. It's totally normal to have a long list of questions, and getting solid answers is the first step toward making a confident decision for your company. Let's break down some of the most common things we hear from founders just like you.

How Fast Can I Actually Get the Money?

This is the big one, and the answer really depends on where you're looking for funds.

Think of traditional bank loans and SBA financing as a long road trip—it can take weeks, or more often, months to get from application to cash in hand. Venture capital is even more of a marathon, filled with endless meetings, deep-dive due diligence, and back-and-forth negotiations.

Alternative financing, on the other hand, is built for the here and now. After you fill out a straightforward online application and upload a few key documents, you can often get a decision within 24 hours. Once you're approved, it's not uncommon to see the funds hit your business bank account the very next day.

What If My Personal Credit Isn't Perfect?

This is probably the most common hurdle for entrepreneurs trying to go the traditional route. Banks are laser-focused on personal credit scores, and a few past mistakes can shut the door completely.

This is where alternative financing really changes the game.

Lenders in the alternative space are more interested in your business's current health and potential. They look at your recent cash flow and revenue patterns—what your business is doing today matters a lot more than your credit score from years ago.

Many of our partners specialize in working with founders who have less-than-perfect credit. As long as you can show consistent monthly revenue and have been in business for at least a year, you’ve got a real shot. Your performance speaks louder than your credit history.

What’s the Difference Between an Interest Rate and a Factor Rate?

Understanding how the cost of your funding is calculated is absolutely critical. You'll often see these two terms, and they work very differently.

- Interest Rate: This is what you see with traditional loans and lines of credit, usually expressed as an Annual Percentage Rate (APR). It's the percentage of the loan balance you're charged over a set period of time.

- Factor Rate: This is a fixed fee you’ll see with options like a Merchant Cash Advance. It's shown as a simple decimal (like 1.3, for example).

Calculating the total cost with a factor rate is dead simple: you just multiply the amount you're advanced by the rate. If you get a $10,000 advance with a 1.3 factor rate, your total repayment will be $13,000. It's designed to be transparent so you know the full cost of the capital right from the start.

Will I Have to Put Up Collateral?

Not necessarily. Traditional lenders almost always demand you pledge specific assets—like real estate or expensive equipment—to secure a loan. For a new business, that's a huge ask.

Thankfully, many alternative financing options are unsecured. This means you don't have to tie your personal or business property to the funding. While a personal guarantee might be required, that’s different from having to sign over the title to your delivery truck.

The one big exception is equipment financing. In that case, the new piece of equipment you’re buying actually serves as its own collateral, which makes the whole process much simpler.

Ready to get clear answers for your business? The team at FSE - Funding Solution Experts is here to help you navigate your options with a simple, no-obligation application. Find your funding solution today.