When you sign a personal guarantee for a business loan, you're essentially telling the lender, "If my business can't pay this back, I will." It’s a promise that puts everything you own—your house, your savings, your car—on the line.

A business line of credit with no personal guarantee completely changes that dynamic. It draws a firm boundary between your company's finances and your personal wealth, offering a powerful layer of protection for established business owners.

What Does "No Personal Guarantee" Really Mean?

Think of a standard business loan as having two safety nets for the lender: your business's assets and, if that fails, your personal assets. A no-PG line of credit removes that second safety net. The lender agrees to look only at the business's ability to repay the debt.

This kind of financing is built on the idea that a truly healthy, mature company should be able to secure funding based on its own merits—its cash flow, its credit history, and its assets. The business stands on its own two feet.

The Strategic Advantage for Seasoned Entrepreneurs

For founders who have spent years, or even decades, building a successful company and personal net worth, this isn't just a loan—it's a critical asset protection strategy. It’s a way to keep growing the business without putting the family home at risk.

This financing is a game-changer for owners who want to:

- Shield personal assets from business creditors if the unexpected happens.

- Create a clean separation between their corporate and personal financial lives.

- Strengthen the company's credit profile completely independently of their own.

To appreciate just how valuable this is, you have to understand how common personal guarantees are. Most small business financing is secured with a guaranty agreement because it dramatically lowers the lender's risk.

In fact, it's the norm. Federal Reserve data shows that a staggering 59% of small businesses with debt have personally guaranteed it. This statistic really drives home how rare and sought-after financing without a PG truly is.

While it’s a tougher nut to crack, securing a line of credit without a personal guarantee is absolutely possible for the right kind of business—one with a proven track record, consistent revenue, and a rock-solid financial history.

To put it all in perspective, here’s a quick look at how these two financing structures stack up against each other.

Standard Line of Credit vs. No Personal Guarantee Line of Credit

This table breaks down the fundamental differences between a business line of credit that requires a personal guarantee and one that doesn't.

| Feature | Standard Line of Credit (with PG) | No Personal Guarantee Line of Credit |

|---|---|---|

| Personal Asset Risk | High; your personal assets can be seized. | None; your personal assets are protected. |

| Lender Requirements | Looks at both your business and personal credit. | Focuses almost exclusively on business health. |

| Typical Credit Amount | Often higher, since it's backed by you. | May start lower, based solely on revenue. |

| Best For | Startups and younger businesses. | Mature, established companies. |

As you can see, the trade-off for protecting your personal assets is meeting a much higher standard of business performance. It's a premium product for premium businesses.

How to Qualify for a No Personal Guarantee Line of Credit

Getting a business line of credit without a personal guarantee is all about proving your business can stand on its own two feet. Since the lender can't come after your personal assets if things go south, they put your company's financial health under a microscope. Think of it like a job interview where your company’s financial history is its resume—every single detail counts.

Lenders are laser-focused on three core areas: your business's financial strength, its payment history, and how long it's been in the game. Without the safety net of your personal guarantee, your business has to look exceptionally stable and predictable.

Pillar 1: Proven and Consistent Cash Flow

Cash flow is everything. To a lender, it's the clearest sign you can actually repay what you borrow. They aren't swayed by a single great sales month; they need to see a pattern of strong, predictable income day in and day out. This consistency shows them your business model works and can handle taking on new debt.

A key benchmark that really moves the needle is hitting $8,000 or more in consistent monthly revenue. Hitting that number—which is nearly $100,000 annually—tells a lender you’re past the volatile startup phase and have built a reliable customer base. You can dig deeper into lender benchmarks for financing without personal guarantees to see how this plays out.

To confirm your numbers, lenders will ask for several months of business bank statements. They'll scrutinize your average daily balances, the size and frequency of your deposits, and any days you dipped into the red. A healthy, steady cash flow is the most powerful argument you can make.

Pillar 2: A Strong Business Credit Profile

Just like you have a personal credit score, your business has its own credit profile. For a business line of credit with no personal guarantee, lenders lean heavily on this to gauge risk. A strong business credit report is proof that you have a track record of managing debt responsibly.

They'll zero in on a few key metrics:

- PAYDEX Score: This score from Dun & Bradstreet reflects how promptly you pay your suppliers. A score of 80 or higher is the gold standard, showing you consistently pay on time or even early.

- Intelliscore Plus (Experian): This score from Experian predicts the odds of your business becoming seriously delinquent on payments. A high score signals financial stability and low risk.

- FICO Small Business Credit Score: Much like your personal FICO score, this gives a quick snapshot of your company's creditworthiness based on its financial habits.

Building a solid business credit profile doesn't happen overnight. It requires a deliberate effort, like opening trade lines with vendors who report to the credit bureaus, paying every bill on time, and keeping your credit utilization low.

A clean business credit report is non-negotiable. Lenders are looking for a history free of defaults, liens, or judgments. Your business credit acts as your company’s professional reputation in the financial world.

Pillar 3: Established Operational History

Time in business is a proxy for experience and resilience. From a lender’s perspective, a long operational history proves you’ve navigated market swings, fine-tuned your operations, and carved out a durable place in your industry. For most lenders offering no-PG financing, this isn't just a preference—it's a hard-and-fast rule.

Typically, you'll need at least two years in business to even be in the running. That two-year milestone shows you're not a fledgling experiment but a sustainable enterprise. A company that has survived and thrived for several years is a far safer bet than one still proving its concept. This history gives lenders the confidence that your revenue is real and your management team knows how to handle whatever comes their way, making it a true cornerstone of qualification.

Evaluating The Pros And Cons Of A No-PG Line Of Credit

Deciding to pursue a business line of credit with no personal guarantee is a major financial crossroads for any company. Like any strategic decision, it’s a game of trade-offs. The allure of shielding your personal assets from business risk is powerful, but it's not a free pass. This type of financing brings its own unique set of challenges and costs.

Ultimately, the choice boils down to a fundamental question of priorities for you and your business right now. What’s more important: the iron-clad protection of your personal wealth, or securing capital with potentially more favorable terms, even if that means putting your own assets on the line?

Let’s walk through both sides of this coin.

The Clear Advantages Of Going No-PG

The biggest win here is obvious, and it's the one that lets entrepreneurs sleep a little better at night: the clean separation of business and personal liability. Think of it as building a financial firewall between your company’s obligations and your family’s security.

Here’s what that looks like in practice:

- Total Protection of Personal Assets: This is the headline benefit. If the business hits an unrecoverable rough patch and defaults, your personal world—your home, your savings, your retirement funds—is off-limits to creditors.

- Forces Stronger Corporate Credit: When you secure financing based purely on the business's strength, you’re compelled to build and maintain an impeccable corporate credit profile. Every on-time payment proves your company can stand on its own two feet, which is invaluable for future financing needs.

- Reduces Personal Financial Stress: The pressure of running a business is immense. Removing the constant, underlying fear of losing your personal assets allows you to make clearer, more objective decisions for the company's growth.

A no-PG line of credit is more than just a loan; it's a statement. You're telling the financial world that your business is fundamentally strong enough to be judged on its own merits.

The Realistic Downsides Of No-PG Financing

Lenders are in the business of managing risk, not giving it away. When they can't fall back on your personal assets, they hedge their bets in other ways. You have to go into this process with your eyes wide open to the hurdles you'll face.

Here are the trade-offs you must be prepared for:

- Higher Interest Rates and Fees: This is the most direct cost. Lenders charge a premium for taking on the added risk. Expect to see higher interest rates and potentially more fees compared to a standard, personally guaranteed line of credit.

- Lower Initial Credit Limits: Since the lender is betting entirely on your business's performance and cash flow, they'll start you off with a more conservative credit limit. They need to see a proven track record of responsible borrowing before they’re comfortable extending more capital.

- A Grueling Underwriting Process: Get ready for a deep dive into your financials. The application process is significantly more intensive. Underwriters will scrutinize everything—bank statements, P&L reports, customer concentration, and even the stability of your industry.

To make this even clearer, here's a side-by-side look at what you're gaining versus what you're giving up.

Pros and Cons of a No-PG Line of Credit

| Advantages (Pros) | Disadvantages (Cons) |

|---|---|

| Your personal assets are completely safe from creditors. | Interest rates are almost always higher. |

| Builds a strong, independent business credit history. | Initial credit limits are typically smaller. |

| Provides significant peace of mind for business owners. | The approval and underwriting process is very strict. |

| Creates a clean financial separation. | May require significant business collateral as security. |

Making the right call means being honest about both sides. You have to weigh the incredible security that a no-PG line offers against the steeper costs and the tougher qualification gauntlet you'll have to run to get it.

Finding the Right Lenders for No Personal Guarantee Credit

When you're looking for a business line of credit without a personal guarantee, your search probably shouldn't start at the big bank on the corner. The lending world is split into different groups, and each has its own comfort level with risk. Knowing where to look is the first, and most important, step.

Traditional banks, for the most part, play it safe. Their entire lending model is built on minimizing risk, and a personal guarantee has always been one of their foundational safety nets. For the vast majority of small and mid-sized businesses, walking into a traditional bank and asking for a loan without a PG is a non-starter.

This old-school reluctance opened up a huge opportunity in the market—one that a new breed of lender was more than happy to seize.

The Rise of Alternative Lenders and Fintech

The best place to find no-PG financing is almost always with alternative lenders and fintech platforms. These companies aren't your typical banks. They operate on a completely different model, relying on sophisticated data analysis and real-time financial monitoring to get a clear picture of a business's health.

Instead of just poring over last year's tax returns, they plug directly into your business bank accounts and accounting software. This gives them a live, up-to-the-minute view of how your business is actually performing right now.

They’re looking at things like:

- Daily Cash Flow: How much money is coming in and out, and how consistent is it?

- Revenue Trends: Are you growing month-over-month? Their algorithms can see momentum that a balance sheet might not show.

- Payment Histories: They can see firsthand how you handle your bills and other financial commitments.

This data-first approach lets them get comfortable lending based on the strength of the business itself, making them the primary source for a true no-PG line of credit. It's a fundamental shift that businesses have welcomed as they look for more flexible ways to get capital.

Since 2020, this kind of flexible financing has become incredibly popular. Recent figures show that 43% of loan applicants were looking for business lines of credit, while only 36% were applying for standard term loans. This highlights a clear trend toward more adaptable funding. You can dig deeper into these small business lending trends on CreditSuite.com.

The Strategic Advantage of a Finance Broker

Sure, you could go directly to these fintech lenders yourself, but it's easy to get lost in the weeds. Every lender has its own sweet spot—a specific industry, revenue level, or credit profile they prefer—and they don't exactly advertise their secret underwriting formulas. Applying to the wrong ones is a waste of time and can rack up hard inquiries that ding your business credit score.

This is exactly why partnering with a specialized finance brokerage like FSE can make all the difference. Think of a broker as a matchmaker who connects good businesses with the right funding.

A broker’s job is to translate your company's financial story into a language lenders immediately understand. They know which lenders are actively looking for a business just like yours and are willing to offer a no-PG line of credit.

Instead of blindly applying and hoping for the best, you get a warm, targeted introduction. A good brokerage has a vetted network of lending partners, including niche players who specialize in this specific type of financing. They’ll pre-qualify your business against the lenders’ criteria, so you only apply where you have a strong chance of approval. This focused strategy doesn't just save you time; it protects your business from the fallout of multiple rejections and puts you on the fast track to securing the capital you need.

Your 4-Step Roadmap to a No-PG Line of Credit

Getting a business line of credit without a personal guarantee isn’t about just filling out a form. It’s a deliberate process. Unlike other loans where your personal credit can cover for business weaknesses, this application rests entirely on your company’s shoulders. The lender needs to see a clear, compelling, and well-documented story of financial strength.

Think of it as a four-stage journey. By tackling it one step at a time—from preparation and profile-building to finding the right partner and navigating underwriting—you’ll be in a much stronger position to get approved.

Stage 1: The Pre-Application Checklist

Before you even approach a lender, you need to get your financial house in order. Lenders expect you to have your documents ready to go. Scrambling to find paperwork at the last minute sends the wrong signal and can bring the whole process to a screeching halt.

Get your essential document package ready now:

- Recent Business Bank Statements: Have the last three to six months ready. Lenders use these to confirm your cash flow and see what your average daily balances look like.

- Profit and Loss (P&L) Statements: You'll need an up-to-date P&L and likely the previous year's as well. This is your proof of profitability.

- Balance Sheet: This document gives a complete snapshot of your company’s financial health by showing its assets, liabilities, and equity.

- Business Formation Documents: Keep your Articles of Incorporation (or Organization), EIN verification letter, and any key business licenses handy.

Stage 2: Strengthening Your Business Profile

With your documents organized, it’s time for a quick health check on your company's public financial profile. It’s a smart move to spot and fix any issues before a lender sees them. They will absolutely be pulling your business credit reports, so you should beat them to it.

Start by getting your reports from the major business credit bureaus like Dun & Bradstreet and Experian Business. Look for errors, old disputes, or late payments that might be dragging your scores down. If you find anything wrong, dispute it right away. If your PAYDEX score is below the magic number of 80, you might even ask vendors who you always pay on time to start reporting those payments.

Think of this stage as prepping your house before a buyer's inspection. You want to fix the small issues before they become major sticking points during the lender's evaluation. A clean, strong profile is non-negotiable.

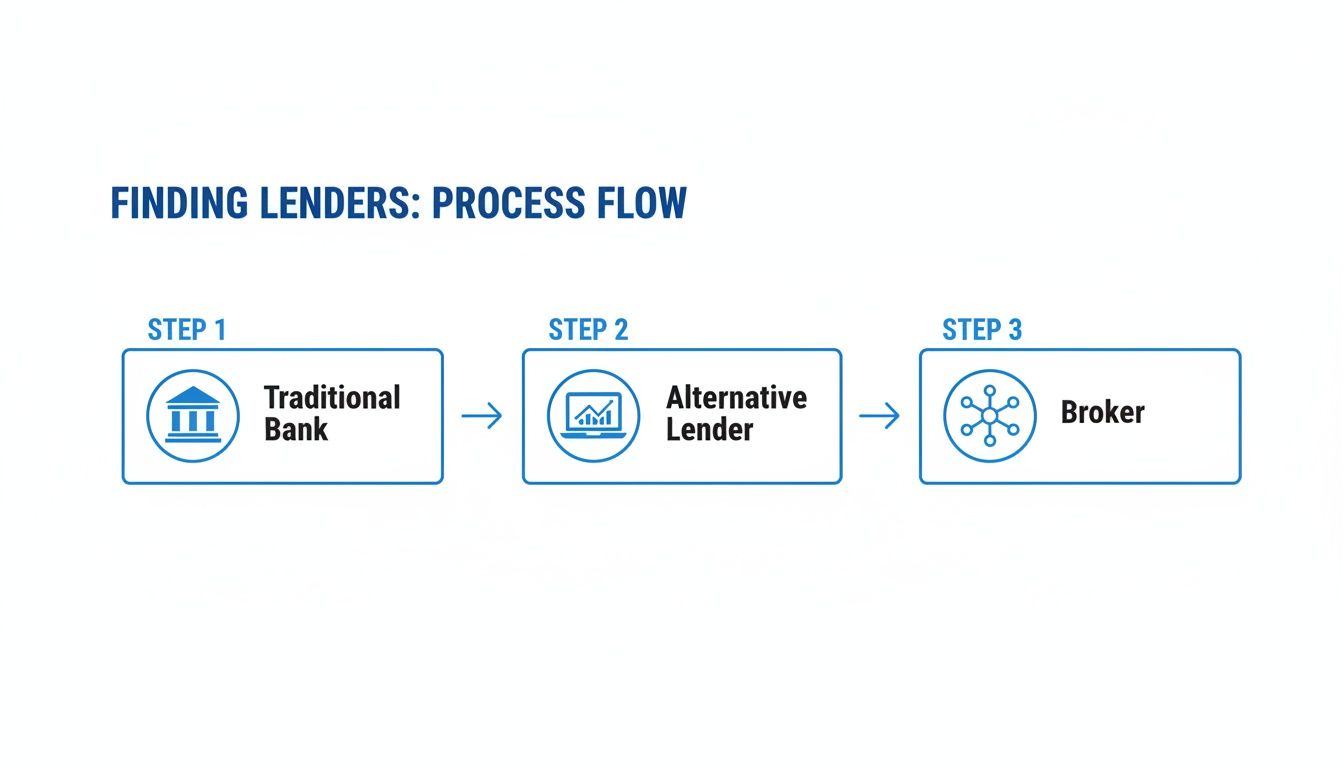

Stage 3: Identifying Your Lending Partner

Finding the right lender is half the battle. Not every bank or financial institution offers a true business line of credit with no personal guarantee, so you need to know where to look. This visual guide shows the typical paths businesses take.

As the flowchart shows, you can go to a traditional bank, but alternative lenders and specialized brokers often provide a more direct route. A good broker, in particular, can be a huge advantage. They know which lenders are actively seeking businesses with your exact profile and can cut your search time dramatically.

Stage 4: Navigating The Underwriting Process

Once your application is in, it heads to the underwriting department. This is where a real person digs into every detail of your business to assess the risk. Don't be surprised if this takes several days.

Be prepared for follow-up questions. An underwriter might ask about a large, one-time deposit, want to understand your customer concentration if one client accounts for most of your revenue, or have questions about your industry's stability.

Your job is to respond quickly and honestly. Clear, confident answers build trust and show you have a solid handle on your operations—and that's exactly what a lender needs to see before they'll extend credit based on your company's merit alone.

Alternatives and Common Pitfalls to Watch Out For

A business line of credit with no personal guarantee is a fantastic tool for mature, healthy companies, but it's not the only game in town for funding growth while protecting your personal assets. If your business doesn't quite check all the boxes for a no-PG line, there are several other smart alternatives that can get you the capital you need. These options simply shift the lender’s security from your personal finances to specific business assets.

At the same time, the road to any kind of business financing is full of potential traps. A few simple missteps in the application process can ding your business credit or lock you into a bad deal. Knowing what not to do is just as critical as knowing your options.

Exploring Other Ways to Finance Your Business

If a no-PG line of credit isn't in the cards for you right now, don't sweat it. You've got other powerful ways to get funded by using what your business already has.

Asset-Based Lending: This is a whole category of financing where your company’s assets are the star of the show, acting as collateral. For instance, accounts receivable financing lets you borrow against your outstanding invoices. Equipment financing is another great example, where the new machinery you're buying secures the loan itself. In both scenarios, the lender is looking to the asset for security, not your personal bank account.

Limited Personal Guarantees: Think of this as the perfect compromise. Instead of guaranteeing 100% of the debt, you can often negotiate a "limited" or "capped" guarantee. This might limit your personal liability to a fixed dollar amount or a specific portion of the loan, like 25%. It’s a great way to drastically reduce your personal risk while still giving the lender an extra layer of confidence.

As you weigh your options, getting the fundamentals right is key. For example, some founders are surprised to learn about different types of capital available; you can check out the definitive guide to understanding the difference between a grant and a loan to get a better handle on the basics. This kind of foundational knowledge helps you make the right call for your company.

Critical Mistakes to Sidestep on Your Funding Journey

The path to securing business funding is littered with common mistakes that are surprisingly easy to avoid if you know what to look for. A little foresight here can save you a ton of time, money, and headaches.

One of the worst things a business owner can do is apply to a dozen lenders at once, hoping something sticks. Each application can trigger a hard inquiry on your business credit, and a flurry of them in a short time makes you look desperate and can drag your score down.

Instead of that scattergun approach, be a sniper. Do your homework and target only the lenders whose criteria truly match your company’s profile before you even think about submitting an application.

Here are a few other critical errors we see all the time:

- Ignoring the Fine Print: Never, ever sign a loan agreement without reading every single word. Get a cup of coffee and focus on the details—especially covenants, prepayment penalties, and any clauses that could put you in default. What you don't know can and will hurt you.

- Fudging the Numbers: It’s tempting to inflate your revenue or profitability to look like a stronger candidate, but it’s a disastrous idea. Lenders have sophisticated tools to verify everything, and getting caught means an instant denial and a black mark on your reputation.

- Being Unprepared: Showing up with messy or incomplete financial documents is a huge red flag for underwriters. It screams disorganization and can slow down your application—or get it tossed out entirely. Get your bank statements, P&L, and balance sheets in order long before you start the process.

Frequently Asked Questions

When you're exploring a business line of credit with no personal guarantee, you're bound to have some specific questions. Let's break down the answers to the ones we hear most often from business owners.

Can a New Business Qualify for a No-PG Line of Credit?

Honestly, it's a real uphill battle for any business less than two years old. Lenders are looking for a solid history of consistent revenue and smart financial decisions to feel comfortable removing the personal guarantee safety net.

Startups just don't have that track record yet, which is why a personal guarantee is almost always part of the deal for early-stage financing. The rare exception might be a brand-new company that's an absolute rocket ship, pulling in exceptionally high revenue right out of the gate.

Will Applying Affect My Personal Credit Score?

A true no-PG application is a corporate-only affair. That means it should not trigger a hard inquiry on your personal credit. The lender’s entire focus is on your business credit reports from bureaus like Dun & Bradstreet or Experian Business.

That said, you should always double-check with the lender before you hit "submit." Some might do a soft pull on your personal credit just to verify your identity, which is harmless and doesn't ding your score. Getting that clarity upfront is key to keeping your personal credit pristine.

Key Takeaway: When done right, applying for a business line of credit with no personal guarantee won't touch your personal credit score. The lender is evaluating the business, not you.

What Is a Limited Guarantee vs. a No Guarantee?

These two options offer very different shields for your personal assets. A no personal guarantee is exactly what it sounds like—you have zero personal liability for the business debt if things go south. Your personal assets are completely separate and protected.

A limited guarantee, on the other hand, is a common middle ground. You're still on the hook personally, but only up to a specific, pre-agreed-upon cap. This could be a fixed dollar amount (like $50,000) or a percentage of the loan (say, 25%). It's a way to drastically reduce your personal exposure without eliminating it entirely.

How Does a Broker Streamline This Process?

Finding lenders that even offer no-PG financing is like looking for a needle in a haystack; they're a tiny slice of the overall lending market. A good finance broker already knows who these niche players are and has built relationships with them.

Instead of you firing off applications into the dark, a broker first gets to know your business. Then, they make a direct introduction to the lenders in their network who are the best fit for your profile. This saves you an enormous amount of time, prevents a bunch of pointless inquiries from hitting your business credit report, and seriously boosts your chances of actually getting funded.

Ready to explore your funding options without putting your personal assets on the line? The team at FSE - Funding Solution Experts can assess your business profile and connect you with the right lending partners. Find out if you qualify in minutes.