Trying to secure business funding can be a frustrating experience, full of long waits and confusing paperwork.I've been there. But the landscape has changed. The modern business loan application process isn't about weeks of uncertainty anymore; decisions can now come through in as little as 24 hours. This guide is here to cut through the jargon and give you a clear, actionable roadmap to getting funded.

What to Expect from the Modern Loan Process

Forget the old way of doing things—stacking up a mountain of paperwork at your local bank and then waiting months for an answer. Technology has completely reshaped how businesses get access to capital, making the entire experience much faster and more transparent. Instead of relying on rigid, one-size-fits-all criteria, today’s lenders use real-time data to get a true pulse on your business's health.

This whole shift is thanks to fintech platforms and specialized brokerages. Digital lending is no longer a niche concept; fintech platforms now handle over 63% of U.S. personal loan originations and more than half of all small-business loans in developed economies. For small and mid-sized businesses in the U.S., this translates to real-world speed: preliminary decisions in as little as 24 hours and funding in your account within 48 hours when working with a broker like FSE. You can dig deeper into these business lending trends on fintech-market.com if you're curious.

Traditional Banks vs Modern Lenders At a Glance

The first step to a successful application is understanding the fundamental differences between old-school banks and the newer players in the funding game. Traditional banks tend to be obsessed with long-standing credit history and hefty collateral, which can shut the door on newer or fast-growing companies.

Alternative lenders and brokers, on the other hand, look at what’s happening in your business right now. They analyze metrics like your monthly revenue and daily cash flow, giving them a much more current and accurate picture of your financial health. This approach is a game-changer for businesses in dynamic industries like construction, logistics, and retail.

This table breaks down the key differences at a high level.

| Factor | Traditional Banks | Alternative Lenders & Brokers (like FSE) |

|---|---|---|

| Decision Speed | Weeks to months | 24-48 hours |

| Paperwork | Extensive and complex | Minimal and digital |

| Approval Criteria | Heavily credit score-based | Focus on revenue & cash flow |

| Flexibility | Rigid loan structures | Multiple, tailored options |

As you can see, the experience is night and day. It really comes down to what you value most: the familiarity of a big bank or the speed and flexibility of a modern lender.

The fundamental change is a move from historical-based underwriting to real-time performance analysis. Lenders today want to see how your business is doing right now, not just what a tax return from last year says.

Why This Guide Matters for Your Business

Think of this guide as your practical playbook. We're going to walk you through the entire journey, from getting your documents in order to understanding the underwriting process and, most importantly, avoiding the common mistakes I see business owners make all the time.

Whether you're a contractor needing to cover payroll between big jobs or a retailer stocking up for the holiday rush, the insights here will help you present your business in the strongest possible light. Let's get you ready to secure the capital you need, quickly and confidently.

How to Prepare for a Successful Application

A strong business loan application process doesn't start the moment you fill out a form. It begins long before. Think of it less as an application and more as building a compelling case for your company's future. The goal is to lay out your financial story so clearly that a lender can confidently see where you’ve been and, more importantly, where you're going.

Rushing the process with a messy pile of papers is one of the fastest ways to get a "no." Lenders aren’t just looking at the numbers themselves; they’re looking for professionalism, stability, and foresight. A clean, organized package tells them you run a tight ship.

Get Your Financial Documents in Order

First things first, you need to paint a complete financial picture of your business. This isn't just about showing revenue; it's about proving that your revenue translates into predictable cash flow and, ultimately, profit. My advice? Get all of this ready before you even start looking at lenders. Create a dedicated folder on your computer and save everything as PDFs.

Here’s the essential paperwork you'll need to gather:

- Business Tax Returns: Lenders will want to see your last two to three years of returns. This gives them a bird's-eye view of your company's performance over time.

- Profit and Loss (P&L) Statements: Have your year-to-date and previous year’s P&L ready. This is the nitty-gritty of your revenues, costs, and expenses that shows if you're actually making money.

- Balance Sheets: A current balance sheet is a snapshot in time, showing exactly what your company owns (assets) and owes (liabilities).

- Business Bank Statements: Plan on providing the last three to six months. Lenders pore over these to understand your day-to-day cash flow, average daily balance, and how consistent your deposits are.

For instance, I once worked with a landscaping company whose income was very seasonal. Looking at a single month's bank statement was misleading. But by providing six months of statements, we could clearly show a healthy average revenue, which smoothed out those seasonal peaks and valleys and got them approved.

Know Where You Stand With Your Credit

Your credit history—both for your business and for you personally—is a huge piece of the puzzle. Lenders use it as a shorthand to judge your reliability. Ignoring your credit profile can stop an otherwise great application dead in its tracks.

A solid personal credit score, generally 680 or higher, is often non-negotiable. Why? Because almost every small business loan requires a personal guarantee. This means if the business can't pay the debt, you're on the hook for it personally.

Lenders don't just see a business; they see the people running it. Your personal financial habits are often viewed as a strong indicator of how you'll manage your business's financial commitments.

Your business credit score (from agencies like Dun & Bradstreet) matters, too. It shows how well you've paid your own suppliers and creditors. The smartest thing you can do is pull both your personal and business credit reports before you apply. Find any errors and get them fixed now, not when you're under a deadline.

Tell a Clear Story About the Money

Finally, you have to answer the most important question: "What is this loan for?" Lenders want to back a specific plan, not just plug a vague hole in your finances. Getting crystal clear on how you'll use the funds shows them you have a real strategy for growth.

Don't just say you need "$100,000 for expansion." That tells them nothing. You have to get specific.

Vague Request: "We need working capital."

Specific Request: "We need $75,000 to buy a new CNC machine that will boost our production capacity by 20%, plus another $25,000 for the raw materials to service a new contract we just landed."

See the difference? This level of detail shows the lender exactly how their capital will generate a return on investment, which makes repayment seem far more certain. It turns your application from a simple request for cash into a solid business proposal. Writing a brief, clear summary of your plan to go with your documents can make all the difference in the underwriting phase of the business loan application process.

Choosing the Right Loan for Your Business

Getting financing isn't just about getting a check—it’s about getting the right kind of funding for your specific situation. I’ve seen countless business owners get this wrong. They secure a loan, only to find the repayment terms cripple their cash flow, or the structure doesn't match their goals. The wrong loan can be a boat anchor, while the right one can be the wind in your sails.

A common mistake is simply asking for a "business loan" without knowing what that really means. It’s like telling a mechanic your car is broken without describing the problem. You wouldn't use a hammer to turn a screw, and the same principle applies here. Lenders want to see you've thought this through.

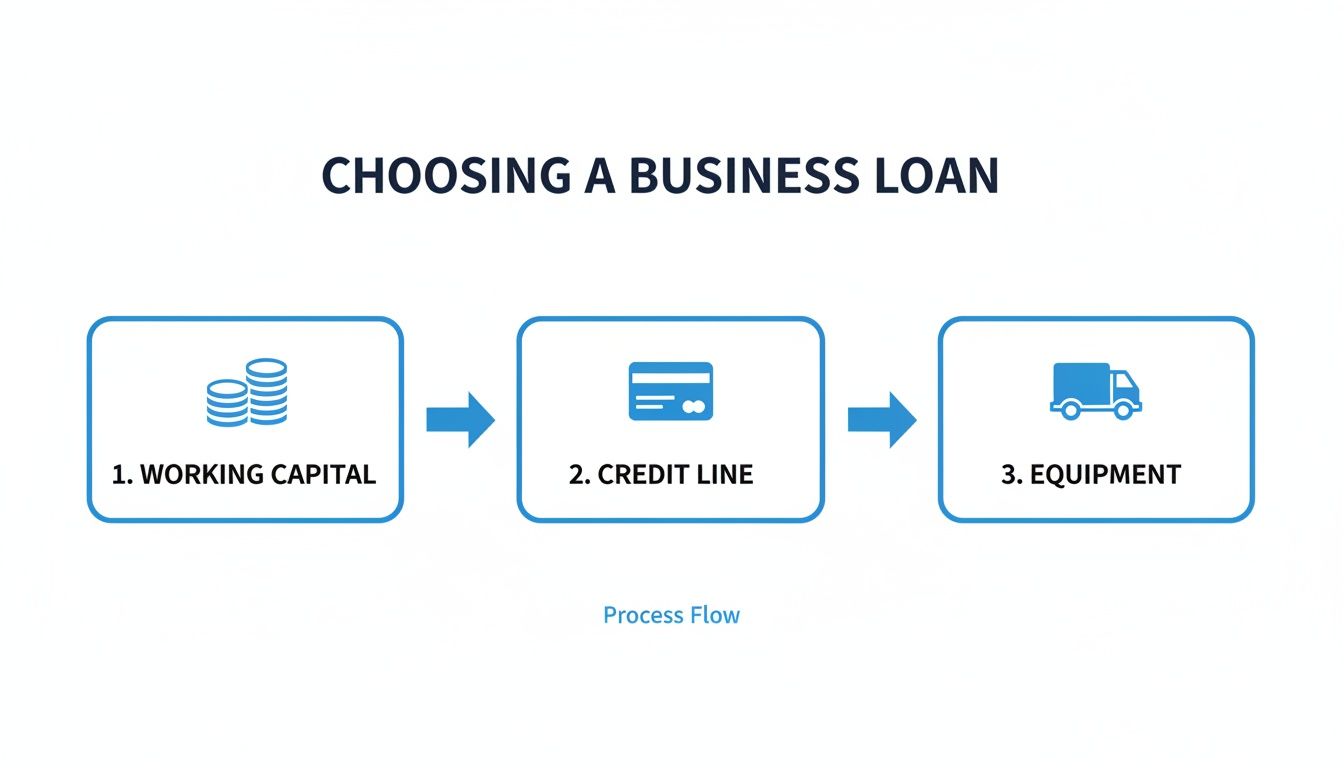

Matching the Loan to Your Business Goal

Before you even think about applying, you need to get crystal clear on one thing: what, exactly, is this money for? Are you trying to cover payroll during a slow season, buy a piece of equipment that will increase your output, or just need a buffer for unexpected expenses? Your answer immediately narrows down the options.

Let's walk through a few real-world examples:

- Working Capital Loans: Think of these as a short-term boost to keep things running smoothly. I worked with a restaurant that needed cash to stock up on premium ingredients and hire extra staff for the holiday rush. A working capital loan bridged the gap until that holiday revenue started rolling in.

- Business Line of Credit: This is your financial safety net, perfect for when you need flexibility. An e-commerce client of mine has a $100,000 line of credit. When a particular product suddenly went viral, she drew $40,000 to triple her inventory, paid it back once the sales cleared, and still had the full $100,000 ready for the next opportunity—all without a new application.

- Equipment Financing: As the name suggests, this is purely for buying machinery, vehicles, or heavy-duty tools. A construction firm needed three new excavators. We used equipment financing where the new machines themselves acted as collateral, which made getting an approval much easier and faster.

Knowing these differences is fundamental to a successful business loan application process. It signals to lenders that you're a serious operator with a clear plan for their capital.

Navigating Your Lending Options

Once you know the type of loan you need, the next big question is where to get it. A decade ago, the answer was almost always your local bank. Today, the field is much wider, which is both a blessing and a curse.

Going straight to a big bank can feel like you're trying to move a mountain. Their underwriting is often rigid, built for established companies with years of history and plenty of hard assets. The statistics don't lie. According to the Report on Employer Firms, only 41% of small business applicants get the full amount they ask for from big banks. In fact, application rates at large banks have even dropped from 44% to 39% as more owners get fed up and look elsewhere. You can dig into the full lending trends from the Federal Reserve to see the data for yourself.

This frustration is exactly why alternative lenders and brokerages have become so important.

Key Insight: Working with a brokerage like FSE is a game-changer. Instead of you applying to dozens of lenders one by one, we take a single application and shop it to a network of over 50. This saves your credit score from taking multiple hits and massively boosts your odds of finding a lender who actually wants to fund your business.

Banks vs. Brokers: A Practical Comparison

Let’s make this real. Imagine two identical construction companies. Both need $150,000 for new excavators to take on a big contract.

Company A decides to go it alone and applies directly to three large banks. Each application is a mountain of paperwork. More importantly, each one triggers a hard inquiry on the owner’s credit. After six weeks of radio silence and follow-up calls, two banks say no. The third comes back with a high rate and terrible terms. Now the owner has wasted over a month and damaged their credit score for nothing.

Company B works with a finance brokerage. They fill out one streamlined online application. Their advisor, who understands the construction industry, immediately knows which lenders are a good fit. The application is presented to a handful of pre-vetted lenders who specialize in equipment financing. Within 48 hours, they have three competitive offers on the table. They pick the best one and have the funds in their account in less than a week.

It’s pretty clear which approach is smarter. Using an expert not only saves you time and headaches but also protects your credit and gets you a better deal. Who you choose to partner with in your search for funding is one of the most critical decisions in the entire business loan application process.

Your Application's Journey: From Submission to Funding

So, you’ve gathered your documents and have a clear idea of which loan type you need. Now, it's time to dive into the application itself. The good news? The modern business loan application process is built for speed, cutting out the weeks of waiting you’d get from a traditional bank.

It all kicks off with a straightforward online application. Forget the thick paper packets of the past; these are designed to be completed in just a few minutes. This first step gives the lender a snapshot of your business: who you are, what you need, and a glimpse into your financial standing.

Next, you'll upload the documents you've already prepped. Having everything ready to go in a digital folder makes this part incredibly smooth. This is your first real chance to show the lender you’re organized and serious—a clean, complete submission avoids needless delays right out of the gate.

The Advisor Review and Underwriting Phase

Once you hit 'submit,' your application lands with a funding advisor. Think of them as your advocate. Their role is to review your file, make sure it’s complete, and position your business in the best possible light for the underwriting team. They’ll look beyond the numbers to understand your story, your industry, and why you need the funds.

This is a huge advantage over going it alone. A seasoned advisor knows what underwriters look for and can emphasize the strengths that a simple balance sheet might miss. It’s a human touch that can make a real difference.

From there, your application heads to underwriting—the heart of the lender’s decision-making process. Underwriters are the ones who perform the deep dive, analyzing your financials to assess risk and determine your creditworthiness. They're not just looking at a credit score; they're evaluating the real-time health of your business.

They focus on a few key metrics:

- Monthly Revenue: Consistency is king. Lenders need to see a reliable income stream to feel confident you can handle repayments.

- Average Daily Bank Balance: This shows you maintain a healthy cash buffer and aren't just scraping by day-to-day.

- Time in Business: Most alternative lenders require at least one year of operating history to show you’ve got a stable foundation.

- Cash Flow Health: They’ll analyze the rhythm of cash moving in and out of your accounts to ensure you can comfortably take on new debt.

The underwriting process isn't about finding reasons to say no. It's about finding the confidence to say yes. Modern lenders focus on your recent performance, not just your history, to make that call.

This infographic simplifies how your specific business need connects to the right loan type, which is the foundational step of this entire journey.

As the diagram shows, figuring out if you need capital for daily operations, flexible cash access, or a major purchase is what points you toward the right funding solution from the start.

The Speed Advantage: From Approval to Your Bank Account

This whole process—from application to underwriting—is where you really see modern lenders shine. By focusing on current data and using smart technology, they make decisions with incredible speed. It’s pretty standard to see preliminary offers land in your inbox within 24 hours.

This speed is more than a convenience; it's a competitive edge. When a critical piece of equipment fails or a golden growth opportunity pops up, you don't have time to wait weeks for a bank's committee to meet. It’s a harsh reality that only 14.6% of small business loan applications get approved at large banks, a statistic that makes many business owners hesitant to even try. This is the gap that fintech lenders have filled, and you can find more small business lending insights on Finli.com.

Once you get an offer you like and accept it, the final step is funding. In most cases, the capital is wired directly into your business bank account, often within 24 to 48 hours of approval. That rapid infusion of cash can be the difference between seizing an opportunity and watching it slip away. The entire business loan application process is designed to get you funded when it matters most.

Common Application Mistakes to Avoid

Navigating the business loan process can be tricky. I’ve seen countless great businesses get turned down not because they weren't qualified, but because of simple, avoidable mistakes on their application. These aren't just typos; they're strategic fumbles that send the wrong message to lenders.

Think of your application as your business's first impression. You want to present a clear, professional, and confident case for funding. Sidestepping these common pitfalls is the first step to getting it right. Too many owners, feeling the pressure, rush their applications with messy financials. Submitting outdated reports, missing tax returns, or showing unexplained revenue dips is a surefire way to get a "no."

Applying for the Wrong Type of Loan

One of the most common blunders I see is a mismatch between the need and the loan product. It’s like using a sledgehammer to hang a picture—it shows the lender you haven’t really thought through your financial strategy. This immediately raises a red flag.

For instance, a construction company that just needs to cover payroll between big project payments should be looking at a flexible line of credit, not a five-year term loan. On the other hand, financing a major piece of equipment that will last a decade with a short-term working capital loan will absolutely crush your cash flow with high, frequent payments.

Before you even start an application, align the loan type with its purpose:

- Short-Term Needs (like inventory or payroll): A line of credit or a working capital loan is usually your best bet.

- Long-Term Assets (like equipment or real estate): Stick with equipment financing or a traditional term loan.

Providing Vague or Incomplete Information

Underwriters live on specifics. A vague request for “$50,000 for business growth” tells them absolutely nothing. It signals you don’t have a solid plan, making it impossible for them to gauge the risk or potential return on their investment. You have to spell out exactly how you'll use every dollar and how that investment will generate the revenue to pay them back.

Don’t be general. A much stronger ask sounds like this: “We need $50,000 to purchase two new delivery vans at $20,000 each, with the remaining $10,000 for vehicle wraps and insurance. This will let us expand our delivery radius by 15 miles and serve 200 more customers a month, which we project will increase revenue by $12,000 monthly.” Now that builds confidence.

At the end of the day, lenders are looking for certainty. A detailed, well-supported plan for the funds is the best way to show you’re a reliable borrower with a clear path to repayment.

Ignoring Your Personal Credit Profile

This is a big one. Many owners think their business's performance is all that matters, but for most small business loans, that’s just not the case. Lenders see you and your business as one and the same—that's why personal guarantees are standard practice. They view your personal financial habits as a preview of how you’ll manage the business’s debts.

Ignoring a low personal credit score or errors on your report is a recipe for rejection. Before you start the business loan application process, pull your credit reports from all three bureaus. Dispute any mistakes and focus on paying down high-balance credit cards. Taking this step before you apply shows you're financially responsible and can dramatically improve your odds.

This table breaks down why it’s so important from a lender's perspective.

| Lender's Concern | What Your Credit Shows | The Impact |

|---|---|---|

| Repayment Reliability | A history of on-time payments | Demonstrates you honor your financial commitments. |

| Financial Distress | High credit card balances | Suggests you might be over-extended personally. |

| Attention to Detail | An error-free credit report | Shows you are on top of your finances. |

Ultimately, avoiding these mistakes comes down to doing your homework. By choosing the right loan, providing sharp details, and making sure your personal finances are in order, you turn a hopeful request into a compelling business case that lenders can’t ignore.

Taking the Next Step: From Plan to Funding

You've just walked through the entire modern business loan application process, and hopefully, it feels a lot less intimidating now. The truth is, getting funded isn't some great mystery; it's about being prepared, knowing what lenders are looking for, and presenting your business in the best possible light.

With this guide, you're no longer just hoping for a "yes." You have a clear strategy to follow, turning what can feel like a maze into a straightforward path. Now you’re in the driver's seat, ready to make the right financial moves to grow your company.

Your Action Plan

Let's boil it all down to what you need to do right now. Focusing on these four areas will put you in a strong position before you ever submit an application.

- Pinpoint Your Funding Needs: Before anything else, get crystal clear on why you need the money and exactly how much. Lenders need to see a well-defined plan, not just a vague request for cash.

- Get Your Paperwork in Order: Create a dedicated digital folder and gather your key documents—recent tax returns, profit and loss statements, and several months of bank statements. Having this ready before you apply is a game-changer.

- Know Your Loan Options: Don't just apply for the first loan you see. Make sure the loan type fits the goal. Is it for short-term working capital? A major equipment purchase? Or maybe a flexible line of credit? The right product matters.

- Find the Right Partner: Don't go it alone. Working with an experienced advisor gives you an inside track. They can connect you with the right lenders from their network, which can save you a ton of time and dramatically increase your chances of getting approved.

Think of securing a loan as a major business milestone, not the final destination. Following a smart, deliberate process turns a stressful task into a strategic advantage, giving you the confidence and the capital to push your business forward.

Answering Your Top Questions About Business Loans

When you're looking for a business loan, a few key questions always come up. It's completely normal to wonder about credit scores, how fast you can get funded, and what it all means for your personal finances. Let's walk through the answers I hear business owners ask for most often.

What’s the Real Minimum Credit Score I Need?

This is probably the number one question, and the honest answer is: it depends entirely on where you apply. There’s no universal minimum.

Traditional banks play in a different league. They're typically looking for a strong personal FICO score of 680 or higher. If your score is below that, getting a "yes" from a big bank is an uphill battle unless you have substantial collateral or a business that's been profitable for years.

On the other hand, the world of alternative lending is much more flexible. These lenders care a lot more about your business's current health—specifically, your monthly revenue and cash flow. While a great score never hurts, many will work with business owners who have scores down in the 600 range, provided the business itself is bringing in consistent money.

Your credit score is just one part of the story. A healthy business with predictable cash flow can often secure funding even with a less-than-perfect credit history, especially with the right lender.

How Quickly Can I Actually Get the Money?

The time it takes to get from application to cash-in-hand is one of the starkest differences between your options.

If you go the traditional bank route, be prepared to wait. The entire process—from submitting paperwork to final approval and funding—can easily stretch from 30 to 90 days. It’s a slow, methodical journey involving multiple layers of review.

Alternative lenders and brokers like us are built for speed. We use technology to look at real-time business data, which cuts the timeline dramatically. Here’s what you can realistically expect:

- Initial decision? Often within 24 hours after we have your complete application.

- Funding? Once you accept an offer, the money is typically in your bank account in 24 to 48 hours.

That kind of speed is a game-changer when you have an opportunity you need to jump on right away.

Will This Application Hurt My Personal Credit Score?

This is a smart question, and it all comes down to the type of credit check the lender performs. There are two kinds, and the difference is crucial.

First, there’s a soft credit pull. Think of this as a preliminary check-up. When you pre-qualify for a loan, a lender does a soft pull to get a high-level view of your credit. It’s invisible to everyone else and has zero impact on your score.

Then there’s a hard credit pull. This happens when you formally submit an application for a specific loan. A hard pull gets recorded on your credit report and can cause your score to dip by a few points temporarily. This is exactly why you shouldn't "shotgun" your application to a dozen different lenders—multiple hard inquiries in a short time can look like a red flag.

Working with a brokerage is the best way to avoid this problem. We can take your single application and shop it to numerous lenders using just one initial soft pull, protecting your credit while finding you the best offers.

Ready to see what funding options are available for your business without impacting your credit score? The expert advisors at FSE - Funding Solution Experts can guide you through the process, comparing offers from over 50 lenders to find the perfect fit. Get started with a no-obligation application at https://www.fseb2b.com.