Yes, you absolutely can get a business loan even with bad credit. While it’s true that traditional banks will likely show you the door, there’s a whole world of alternative lenders who look at your business very differently. They’re more interested in your company's current health—your cash flow, your recent sales—than mistakes you might have made in the past.

Why a Bad Credit Score Isn't a Dealbreaker

Getting turned down by a bank can feel like hitting a brick wall. It’s discouraging, but a rejection from a big bank is far from the final say on whether your business can get funded. Think of your personal credit score as a rearview mirror; it’s a great summary of where you've been, but it says very little about where your business is headed.

Alternative lenders, on the other hand, look through the windshield. They focus on your company's real-time performance and its future potential. This forward-looking approach has opened up financing for thousands of otherwise healthy, growing businesses whose owners have a less-than-perfect credit history.

A New Way to Look at Lending

To understand this shift, it's helpful to see how traditional banks and alternative lenders evaluate businesses side-by-side. Their priorities are worlds apart.

Bank Loans vs. Bad Credit Business Loans: A Quick Comparison

| Evaluation Factor | Traditional Bank Lenders | Alternative & Bad Credit Lenders |

|---|---|---|

| Primary Focus | Historical credit & collateral | Current cash flow & revenue |

| Credit Score | Critical factor (often 680+ FICO required) | Secondary factor (can be below 550) |

| Application Process | Lengthy, document-heavy | Fast, streamlined, often online |

| Decision Speed | Weeks or months | Hours or a few days |

| Collateral | Often required (real estate, equipment) | Typically unsecured or uses future sales |

| Time in Business | Usually requires 2+ years | Often accepts 6-12 months |

As you can see, the game is completely different. Where banks see risk in a FICO score, alternative lenders see opportunity in your bank statements.

What Lenders Look for Instead of Credit

So if your personal credit score isn't the main event, what is? These lenders have a checklist of their own, and it's all about the here-and-now health of your business.

They dig into concrete, day-to-day metrics to gauge your ability to handle a loan.

Here’s a snapshot of what they prioritize:

- Consistent Monthly Revenue: This is huge. Most lenders want to see at least $10,000 to $20,000 in monthly sales. It’s direct proof that you have a steady income stream to make payments.

- Time in Business: Lenders generally want to see that you’ve been up and running for at least one year. This demonstrates stability and proves you can manage the ups and downs of your market.

- Healthy Bank Balances: They'll want to see your last few months of bank statements. They’re looking at your average daily balance and scanning for red flags like frequent overdrafts or non-sufficient funds (NSF) notices.

By zeroing in on these operational vital signs, these lenders can confidently offer business loans for bad credit to solid companies that traditional banks would unfortunately pass over.

Why Your Business's Health Matters More Than Your Credit Score

If you're hunting for a business loan with bad credit, it's easy to get fixated on your personal FICO score. Traditional banks have spent decades drilling into us that this one number is the be-all and end-all of financial trustworthiness. But in the world of modern alternative lending, that’s an old-school way of looking at things.

Think of your credit score as a rearview mirror. It shows where you’ve been—old debts, past stumbles, payment history. It tells a story, sure, but it says very little about the engine humming under your business's hood right now.

Shifting the Focus from Past Performance to Present Potential

Alternative lenders work from a completely different playbook. They get that an owner’s personal financial past and their business's current reality can be two very different stories. A low credit score might be the ghost of a medical emergency from five years ago or a messy divorce—neither of which has anything to do with your company's ability to pull in revenue today.

So, instead of looking backward, they look at what’s happening in the here and now. They want to check your business's current financial pulse: its revenue, its cash flow, and its day-to-day stability. Frankly, it’s a much more logical way to figure out if a business can handle and pay back new funding.

The Bottom Line: For an alternative lender, your last three months of bank statements tell a more compelling story than a seven-year-old credit report. They show exactly how much cash your business is generating and how well you're managing it.

This change in perspective is a game-changer. It unlocks financing for thousands of solid businesses that would otherwise be shut out by traditional banks simply because of an owner's old credit issues.

The Numbers That Really Move the Needle

If a 550 FICO score isn't a dealbreaker, what are these lenders looking at? They zoom in on the vital signs of your business, which are easy to prove with the right documents.

It really boils down to three core things:

- Consistent Monthly Revenue: This is the big one. Lenders need to see a reliable stream of income. Most are looking for a minimum of $10,000 to $20,000 in gross monthly sales, which you'll prove with your recent bank statements.

- Time in Business: They want to see that you're not a flash in the pan. Typically, lenders require you to have been up and running for at least one year. This shows you’ve got a viable business model and have cleared the early hurdles.

- Average Daily Bank Balance: This little number speaks volumes about your cash management skills. They’ll scan your statements for a healthy daily balance and watch out for red flags like frequent overdrafts or bounced payments (NSFs), as those can signal a company in distress.

By focusing on these real-world metrics, lenders can make smart decisions based on your business's current strength, not its past struggles.

A Real-World Example

Let’s take a general contractor with a 580 personal credit score because of a foreclosure that happened years ago. Walk into a traditional bank, and the conversation is likely over before it starts.

But an alternative lender will look at the business itself. Here are its vitals:

- It's been in business for three years.

- It consistently pulls in $45,000 a month from steady contracts.

- The business bank account keeps an average daily balance of $8,000.

What does the lender see? A stable, profitable company with strong, predictable cash flow. That old foreclosure is ancient history and has no bearing on the business’s ability to repay a loan today. This contractor is an ideal candidate for funding because the business is a solid bet. This is the perfect illustration of how focusing on provable business health opens doors where traditional lending only sees roadblocks.

Exploring Your Top Financing Options for Bad Credit

When the bank says no, it’s easy to feel like you've hit a dead end. The truth is, you’ve just been on the wrong road. The world of alternative finance is full of different funding vehicles, each built for specific business needs—especially for owners who need a business loan for bad credit.

Instead of focusing on a single credit score, these options look at the real health of your business: your sales, your invoices, and your daily cash flow. Let's break down the most practical and effective solutions out there.

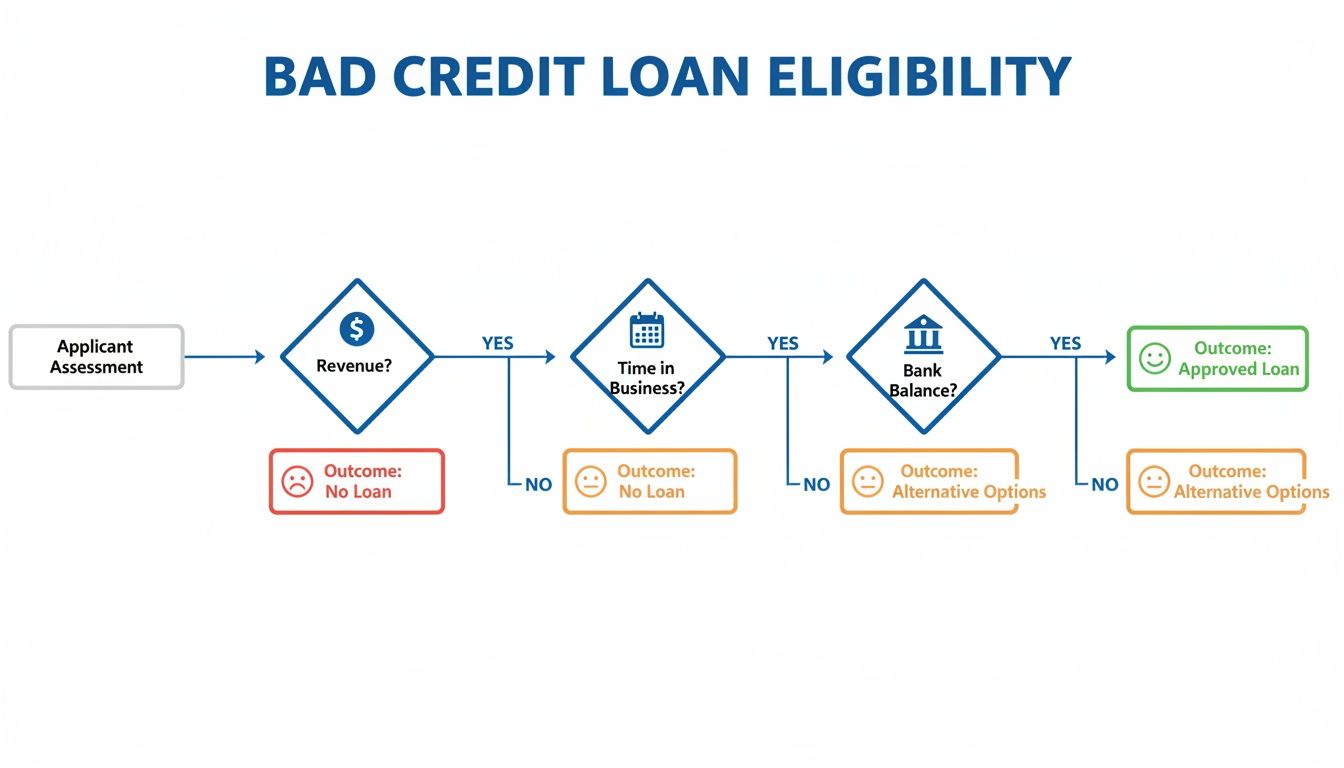

This flowchart gives you a high-level look at how these lenders size up a business.

As you can see, metrics like consistent revenue, how long you've been in business, and a healthy bank balance become the keys to unlocking capital, even when a credit history is less than perfect.

To help you navigate these choices, we've put together a quick comparison table. It breaks down the most common options so you can see at a glance which one might be the right tool for the job.

Bad Credit Financing Options at a Glance

| Financing Type | Best For | Repayment Structure | Typical Funding Speed |

|---|---|---|---|

| Merchant Cash Advance | High-volume card sales (retail, restaurants) | A percentage of daily credit/debit card sales | 24-48 hours |

| Revenue-Based Financing | B2B or service businesses with consistent bank deposits | Fixed daily or weekly bank debits | 1-3 business days |

| Invoice Factoring | B2B businesses waiting on customer payments | Factor collects from your customers; you get an advance | 2-5 business days |

| Short-Term Loan | One-time investments like inventory or equipment | Fixed daily, weekly, or bi-weekly payments | 1-3 business days |

This table is a starting point. Now, let's dive deeper into how each of these works so you can get a better feel for the mechanics and decide what truly fits your business model.

1. Merchant Cash Advance (MCA)

A Merchant Cash Advance (MCA) is one of the most accessible funding types for businesses with a steady stream of credit and debit card sales—think restaurants, retail stores, or auto shops. Technically, it isn't a loan at all. It's a sale of a portion of your future revenue at a discount.

Here’s the simple version: A funder gives you a lump sum of cash today. In return, they get a small, agreed-upon percentage of your daily card sales until the advance is paid back.

The repayment mechanism is its biggest strength:

- On a busy day, you pay back a little more.

- On a slow day, you pay back a little less.

This natural rhythm means the payments flex with your cash flow, which is a game-changer for businesses with seasonal ups and downs. Because repayment is tied directly to your daily sales, funders care far more about your sales history than your FICO score.

2. Revenue-Based Financing

Revenue-Based Financing is a close cousin to the MCA but works a little differently. Instead of being tied to your card sales, repayment happens through a fixed, automated debit from your business bank account, usually on a daily or weekly schedule.

This structure makes it a perfect fit for businesses that don't rely heavily on card payments, like B2B companies, contractors, or consultants who get paid via checks and wire transfers. The lender will analyze your recent bank statements to see your total revenue deposits, and that's what qualifies you.

The core idea is the same as an MCA: your proven ability to generate consistent cash flow is what matters most. It’s a direct way to get working capital based on the health of your entire operation, not just one sales channel.

3. Invoice Factoring

If you run a B2B company, you know the pain of waiting 30, 60, or even 90 days for clients to pay their invoices. That wait can create huge cash flow gaps, making it tough to cover payroll or jump on the next big project. Invoice factoring, also known as accounts receivable financing, is the solution.

It's a straightforward process:

- You sell your unpaid invoices to a "factor" (a specialized finance company) at a slight discount.

- The factor immediately advances you a huge chunk of the invoice's value—usually 80% to 90%.

- The factor then works with your customer to collect the full payment.

- Once the invoice is paid, the factor sends you the remaining balance, minus their fee.

With factoring, the creditworthiness of your customers is actually more important than your own. If you work with reliable clients who pay their bills, this can be an incredible way to unlock the cash that’s already yours, regardless of what your own credit report says.

4. Short-Term Loans

A short-term business loan operates more like traditional financing but is built for speed and accessibility. You get a lump sum of cash upfront and repay it over a set term—typically six to 24 months—with fixed payments (often daily or weekly).

While a bank loan can drag on for months, a short-term loan from an alternative lender can be in your account within a couple of days. Lenders are more focused on your recent revenue and cash flow than a flawless credit history. These loans are perfect for specific, one-off investments where you have a clear use for the funds, such as:

- Buying a large batch of inventory to get a supplier discount.

- Covering the startup costs for a new, profitable contract.

- Making a necessary equipment upgrade to boost efficiency.

The cost is typically presented as a factor rate (e.g., 1.20) instead of a traditional APR. This makes it very easy to see the total payback amount from day one, giving you the clarity needed to make a smart financial decision.

Imagine running a thriving construction firm, but your bank won't touch you due to a past credit hiccup. You're not alone. The global market for unsecured business loans—which don't require collateral—hit USD 253.9 billion and is projected to reach USD 561.3 billion, growing at a strong 10.2% CAGR. North America accounts for 34.87% of this market, largely because fintech lenders have created digital underwriting processes that bypass old-school bank bureaucracy. Small businesses with 10-49 employees make up 33.58% of this market, using these funds to expand and manage inventory by showing lenders their steady cash flow is what truly counts. You can read more about these unsecured business loan trends and gain additional insights.

How to Prepare Your Application and Maximize Approval

When you have less-than-perfect credit, your loan application becomes your most powerful tool. It’s not just a collection of forms; it’s your chance to tell the real story of your business. Your credit score is a snapshot of the past, but what lenders really care about is your company’s current health and future potential.

Think of it this way: you’re building a case. You need to prove that despite past hurdles, your business is a solid, revenue-generating operation. The goal is to shift the lender's focus from what happened last year to what's happening right now—and how this new funding will fuel your growth tomorrow.

Gather Your Essential Documents

First things first, let's get your paperwork in order. Alternative lenders aren't like big banks that demand a mountain of documents. They have a much shorter, more focused checklist designed to get a quick and accurate read on your recent performance.

You'll almost certainly need to pull together the following:

- Recent Bank Statements: This is the big one. Most lenders want to see your last three to six months of business bank statements. It gives them a direct, unfiltered look at your day-to-day revenue, cash flow, and overall financial discipline.

- Proof of Revenue: While bank statements are the primary source, some lenders might ask for supporting evidence like merchant processing statements (if you accept credit cards) or a simple year-to-date profit and loss statement.

- Basic Business Information: This is the easy stuff—your official business name, address, Employer Identification Number (EIN), and documents that prove you own the company.

Each of these items helps paint a picture of a stable, well-managed business that can handle financing.

Tell a Compelling Financial Story

Once you have your documents, your job is to make sure they tell the right story. Lenders are trained to spot signs of stability and growth. Your application is your opportunity to highlight those positive signals and get ahead of any potential concerns.

A strong application doesn't just present numbers; it gives them context. You’re in the driver's seat here, building the lender's confidence with every piece of information you provide.

Your application is your chance to prove that your business's current performance is a far better predictor of its future than an old credit score. Every document should support that core message.

Taking this proactive stance can make all the difference in getting the green light.

Pro Tips to Strengthen Your Application

Before you hit that submit button, take a moment to look at your application from a lender's perspective. A few small tweaks can dramatically change how they view your business's financial strength. Here are a few insider tips to boost your approval odds.

Prepare a Brief Credit Explanation: Don't leave past credit problems open to interpretation. Write a short, honest paragraph explaining any major dings on your report. Was it a medical emergency? A messy divorce? Owning the story shows you're transparent and, more importantly, that the issue was a one-off event that has nothing to do with how you run your business today.

Review Your Bank Statements for Red Flags: Lenders are laser-focused on your bank statements, looking for signs of financial distress. The most common red flags are frequent overdrafts, non-sufficient funds (NSF) fees, and a consistently low average daily balance. If you see these issues, consider waiting a month or two to apply. A couple of months of "clean" statements showing a healthier cash buffer can work wonders.

Clearly Articulate the Use of Funds: Get specific. "Working capital" is too vague and sounds like you're plugging holes. Instead, explain exactly how the funds will generate a return. For example: "Purchase $20,000 in new inventory to fulfill a signed contract with XYZ Company" or "Invest $15,000 in a targeted marketing campaign to increase online sales by 25%." This shows you have a clear, strategic plan for growth.

By taking these steps, you elevate your application from a simple request for money to a well-structured business case. You're no longer just asking for a loan—you're inviting a financial partner to invest in your company's future. That level of professionalism is exactly what it takes to secure funding, even with bad credit.

Navigating Rates, Terms, and Common Red Flags

Let's be upfront: if you’re searching for a business loan for bad credit, the cost will almost certainly be higher than for a business owner with a perfect 750 FICO score. That's not a dealbreaker, but it does mean you need to be twice as diligent.

Getting a firm grasp on the true cost of financing is the single most important thing you can do. It’s the difference between finding a smart solution that helps you grow and signing up for a new financial headache. This knowledge gives you control. It empowers you to spot a good deal and, just as crucially, to walk away from a bad one.

Demystifying Your Offer: The Cost of Capital

In the world of alternative business funding, the price tag isn't always presented as a simple Annual Percentage Rate (APR). Many lenders use different methods, like factor rates, which are easier to calculate on the fly but can be deceptive if you aren’t sure what you're looking at.

- Annual Percentage Rate (APR): This is the all-in-one number you're used to seeing with credit cards and traditional bank loans. It bundles the interest rate and most fees into a single yearly percentage, making it the gold standard for an apples-to-apples comparison.

- Simple Interest: As the name implies, this is interest calculated only on the original amount you borrowed (the principal). It’s straightforward but not as common in the fast-paced world of short-term business financing.

- Factor Rate: This is the go-to pricing model for most merchant cash advances and short-term loans. It’s shown as a decimal—like 1.25—and makes figuring out your total payback amount incredibly simple.

Let's break down how a factor rate plays out in the real world.

Example: A Business Loan with a Factor Rate

Suppose you’re offered a $20,000 short-term loan with a factor rate of 1.30.

To calculate what you’ll pay back in total, you just multiply the loan amount by the factor rate:

$20,000 (Loan Amount) x 1.30 (Factor Rate) = $26,000 (Total Repayment)

So, the cost of borrowing that $20,000 is $6,000. The beauty of this is its simplicity—you know the exact cost from day one without needing to track complicated amortization schedules.

Critical Red Flags to Watch For

While most lenders are legitimate partners invested in your success, the alternative finance space has its share of bad actors. Protecting your business means learning to spot the warning signs of a predatory deal.

Predatory lenders thrive on urgency and confusion. Their entire game is to get you to sign before you fully understand what you're agreeing to. If you feel rushed, pressured, or confused, that’s your cue to hit the brakes and ask more questions—or just walk away.

Keep an eye out for these specific red flags:

Extreme Pressure to Sign Immediately: A credible lender wants you to be comfortable and will give you time to review an offer. If a rep is pushing a "today-only" deal or demanding you sign on the spot, it’s a classic high-pressure sales tactic, not a sign of a good partnership.

Lack of Transparency About Fees: Are there vague underwriting fees, application fees, or hidden prepayment penalties? A trustworthy lender lays all costs on the table. If fees are buried in fine print or the lender gets evasive when you ask for a clear breakdown, be very wary.

No Physical Address or Web Presence: Do a quick Google search. If the company has no professional website, no verifiable address, and no reviews or history online, you have to ask yourself who you’re really dealing with.

"Guaranteed" Approval: This is one of the biggest red flags out there. No reputable lender can guarantee approval without first looking at your business's financial health. A promise of "100% approval for everyone" is almost always a bait-and-switch tactic.

Successfully navigating the world of business loans for bad credit is all about being an informed, vigilant borrower. When you understand the terms and know what red flags to look for, you can secure the capital you need to grow your business with confidence.

Your Questions Answered: Getting a Business Loan with Bad Credit

When you're running a business and your credit isn't perfect, you're bound to have questions about financing. It's a confusing landscape. Let's clear up some of the most common concerns business owners have when they're looking for a business loan for bad credit. We'll get straight to the point on credit pulls, funding speed, and what really matters to lenders.

The main takeaway? It's less about your past and more about your business's current performance. Understanding that simple fact can make this whole process a lot less intimidating.

Will Applying for a Loan Wreck My Personal Credit Score?

This is probably the number one worry for business owners, and for good reason. Thankfully, most modern alternative lenders have built their process specifically to avoid this problem. When you first apply, they’ll run what’s called a "soft credit pull."

Think of a soft pull like a quick glance at your credit profile. It gives the lender a ballpark idea of your history, but it's invisible to other financial institutions and has zero impact on your credit score. It's a no-risk way for you to see what kind of offers might be on the table.

Only when you’ve reviewed an offer you like and decide to move forward will a lender perform a "hard credit pull." That’s the official inquiry that can cause a small, temporary dip in your score. This two-step approach lets you shop around for the best financing deal without dinging your credit along the way.

What's the Lowest Credit Score I Can Have to Qualify?

Big banks might have rigid FICO score cutoffs, but the world of alternative lending plays by a different set of rules. For many of these specialized lenders, there is no hard-and-fast minimum credit score. They're much more interested in the health and vitality of your actual business operations.

They look at practical metrics that paint a much clearer picture of your company's strength:

- Steady monthly revenue (often looking for $10,000 to $20,000 or more)

- Time in business (usually at least one year)

- A healthy daily balance in your business bank account

For instance, a business owner with a 550 credit score who can show $25,000 in consistent monthly sales is often a far more attractive candidate than someone with a 700 score and erratic revenue. As a general rule, a score over 500 opens up a lot of doors, but the decision always comes down to your company's cash flow, not just one number from your past.

How Fast Can I Actually Get the Money?

Speed is where alternative lenders truly shine. A traditional bank loan can feel like it's moving at a snail's pace, often taking weeks or even months to close. Financing designed for businesses with bad credit is built for one thing: getting capital into your hands when you need it.

The timeline is incredibly compressed. Here’s how it usually breaks down:

- Fill out a simple online application—this rarely takes more than a few minutes.

- Upload your last few months of business bank statements.

- You can get a decision, often with concrete offers, within 24 hours.

Once you pick an offer that fits your needs and sign the agreement, the funds can hit your business bank account in as little as one or two business days. This kind of speed is crucial when an opportunity pops up or an emergency expense needs to be covered now.

The ability to go from application to funding in under 48 hours is a genuine game-changer. It gives small businesses the agility to seize opportunities and manage cash flow effectively, ensuring capital arrives when it's most needed, not weeks too late.

Can I Get a Loan if My Business Isn't Making Money Yet?

For the financing options we've covered here—like merchant cash advances, short-term loans, and revenue-based financing—your existing revenue is the entire basis for the loan. These products are all about providing working capital by advancing you funds against your proven, ongoing cash flow.

Lenders need to see that track record of sales to calculate a funding amount and repayment plan that won't cripple your business. Because of this, they simply can't fund brand-new startups or pre-revenue ventures, no matter how brilliant the business plan is. Most will want to see at least one year in business and a solid history of monthly deposits. If you're just starting out, you might have better luck exploring SBA microloans or local community grants.

Ready to see what financing your business can get without impacting your credit score? FSE - Funding Solution Experts can connect you to the right lender. Our quick application gives you access to a network of over 50 lenders who care more about your business's health than its credit history. Get your no-obligation funding estimate today!