At its core, a business term loan is a straightforward and dependable way to get capital. You receive a lump sum of cash upfront and pay it back over a fixed period through regular, predictable payments. It's one of the most classic and widely used tools for funding major, planned investments that fuel business growth.

What Exactly Is a Business Term Loan?

The easiest way to think about a business term loan is to compare it to a personal loan you're already familiar with, like a mortgage for a house or financing for a car. You borrow a set amount of money for a specific reason and agree to pay it back—plus interest—with a consistent payment schedule. That predictability is its greatest strength, giving you a clear financial roadmap.

This is very different from a revolving business line of credit, which acts more like a credit card you can draw from and pay down repeatedly. A term loan is a one-time injection of funds, making it the perfect vehicle for a single, large-scale project where you know exactly how much you need from the get-go.

To give you a quick snapshot, here are the essential components of a typical term loan.

Business Term Loan At a Glance

| Feature | Description |

|---|---|

| Loan Amount | A single, lump-sum disbursement of cash. |

| Repayment | Fixed, regular payments (usually monthly) over a set period. |

| Interest Rate | Can be fixed or variable, determining the cost of borrowing. |

| Term Length | The repayment period, ranging from short-term (1-3 years) to long-term (10+ years). |

| Best For | Specific, one-time investments like equipment, real estate, or business expansion. |

This table shows why business owners value term loans: every element is defined upfront, leaving little room for surprises.

Core Components of a Term Loan

Every term loan, regardless of the lender, is built on three fundamental pillars. Getting a handle on these is the first step to figuring out if this is the right financing for your business.

- Principal: This is simply the amount of money you borrow. If you’re approved for a $100,000 loan to upgrade your manufacturing line, the principal is $100,000.

- Interest: This is what the lender charges for the service of lending you money, always expressed as a percentage rate. It’s their compensation for taking on the risk.

- Term Length: This is the repayment runway—the agreed-upon time you have to pay the loan back in full. Terms can be as short as a few months or stretch out to 10 years or more for big-ticket items like commercial property.

The real magic of a term loan is its predictability. A fixed payment schedule lets you budget with precision and forecast your cash flow, taking the guesswork out of your finances.

These three ingredients—principal, interest, and term—all come together to determine your payment amount and frequency, which is most often monthly.

When Businesses Use Term Loans

Businesses typically reach for a term loan when they're making a significant, strategic move designed to create long-term value. It’s a tool for deliberate, planned growth, not for patching up unexpected cash flow gaps.

For instance, a landscaping company might take out a five-year term loan to purchase a new fleet of commercial mowers. A successful restaurant might use one to fund a major renovation and add a patio for outdoor seating. In both scenarios, the loan is directly tied to a project that will boost the company's ability to earn more revenue.

Common uses include:

- Purchasing heavy machinery, equipment, or vehicles

- Expanding to a new physical location or opening another branch

- Financing the acquisition of a competing business

- Making significant leasehold improvements to a rented space

- Securing permanent working capital for a large-scale growth plan

A Look at the Different Types of Term Loans

Once you've got the basic concept of a business term loan down, you'll find they aren't a one-size-fits-all product. Think of them like tools in a toolbox. You wouldn't use a sledgehammer for a finishing nail, and the same logic applies here—the right loan depends entirely on the job you need it to do.

The main way lenders slice and dice these loans is by their repayment period, or "term." This one factor has a massive ripple effect, influencing everything from your monthly payment to the total interest you’ll pay over the years. Getting familiar with the categories is the first step toward making a smart financing choice.

Short-Term Loans

Short-term loans are the sprinters of the lending world. They’re built for speed and designed to solve immediate, temporary needs. Typically, you’re looking at a repayment window of three years or less, and sometimes just a few months.

Imagine a retail shop that needs to stock up on inventory for the holiday rush. They could use a short-term loan to buy all that merchandise, knowing they can repay the funds quickly once the holiday sales start rolling in. It's all about seizing an opportunity or plugging a temporary cash flow hole.

Here are a few common scenarios for short-term loans:

- Bridging a cash gap while waiting on a large client payment.

- Covering an emergency repair to critical equipment.

- Funding a small marketing push with an expected fast return.

Because the payback period is so condensed, the monthly payments are higher. The upside? You pay far less in total interest compared to a longer-term loan.

Intermediate-Term Loans

Sitting comfortably in the middle, intermediate-term loans strike a nice balance. They offer more manageable payments than a short-term loan while funding more significant projects. These loans usually have terms ranging from three to five years, making them a versatile workhorse for established businesses.

A great example is a growing marketing agency that needs to buy a new suite of high-powered computers for its expanding design team. It's a bigger investment than they could pay back in a year, but it doesn't warrant a decade-long loan. An intermediate loan is often the perfect fit for this kind of growth-focused investment.

Long-Term Loans

Long-term loans are the marathon runners, built for the major, foundational investments that will define your company's future. With repayment terms that often stretch from five to ten years or even longer, they are reserved for financing big-ticket assets with a long, productive life.

This is the kind of financing you seek out for transformative goals, such as:

- Buying commercial real estate, like your first office or warehouse.

- Financing a business acquisition.

- Undertaking a major construction project or facility expansion.

The longer repayment schedule means lower monthly payments, which makes those massive loan amounts much more affordable. Just remember, the trade-off is that you will pay significantly more in total interest over the life of the loan.

Secured vs. Unsecured Term Loans

Beyond the loan's timeline, another crucial fork in the road is whether it's secured or unsecured. This all comes down to the level of risk the lender is willing to take on, which directly impacts your interest rates and your chances of getting approved.

A secured loan is backed by collateral. This is a valuable business asset—like real estate, inventory, or equipment—that you pledge to the lender. If you can't repay the loan, the lender has the right to seize that asset. This safety net for the lender usually means better interest rates and terms for you.

An unsecured loan, as the name implies, isn't tied to any specific collateral. The lender is betting entirely on your business's financial strength, cash flow, and credit history. Because the risk is much higher for them, these loans almost always come with higher interest rates and tougher qualification standards.

Interestingly, the market for unsecured business loans is booming, projected to hit USD 561.3 billion by 2034. This growth is largely driven by new technology that allows lenders to better assess risk without relying on physical assets. If you want to dive deeper, you can learn more about trends in the unsecured lending market.

What Lenders Look For In Your Application

Trying to get a business term loan can feel like you're being put under a microscope. But it’s not as mysterious as it seems. Lenders are simply trying to answer one fundamental question: "Is this business a good bet?" They're in the business of managing risk, and they have a pretty standard checklist they use to figure out if you can reliably pay back the loan.

Knowing what's on that checklist ahead of time is your biggest advantage. It lets you walk in prepared, with a strong application that tells the right financial story about your company. It’s less about being perfect and more about presenting a clear, honest picture of your business's health and where it's headed.

The Five Pillars of Underwriting

When an underwriter gets your loan file, they're essentially checking the strength of five core areas of your business. Think of them as the five pillars holding up your loan request. Each one offers a unique angle on your company’s ability to handle new debt.

- Creditworthiness: This is a big one. It covers both your personal and business credit scores, offering a quick look at how you've handled debt in the past.

- Cash Flow: Lenders pore over your bank statements to see if you have consistent, positive cash flow. This is their proof that you have the money coming in to cover your current bills plus a new loan payment.

- Collateral: For secured loans, this is what you put on the line—equipment, inventory, or real estate. It’s the lender’s safety net if things go south.

- Capital: This is all about how much of your own money you have in the business. It shows lenders you have real skin in the game, which is a huge confidence booster.

- Conditions: Lenders don't operate in a vacuum. They’ll also look at things like your industry, current market trends, and the general economic outlook to assess external risks.

Remember, no single pillar makes or breaks your application. An underwriter is trained to look at the whole picture. So, major strength in one area can often help make up for a little weakness in another.

Your Personal and Business Credit Score

Your credit history is often the first thing a lender checks, and it makes a powerful first impression. A solid credit score shows you’re disciplined with your finances and have a history of paying your debts on time.

While every lender is different, most traditional banks like to see a personal credit score of 680 or higher to qualify for the best term loan rates. But don't panic if your score isn't there yet. Plenty of alternative lenders work specifically with business owners who have a few dings on their credit report, though you can expect to pay a higher interest rate for that flexibility.

Time in Business and Annual Revenue

These two data points are straightforward but tell a lender a lot about your company's stability. Most lenders prefer to see that you've been in business for at least two years. This track record proves your business model works and you’ve made it past the volatile startup phase.

Your annual revenue, on the other hand, shows your capacity to take on debt. There’s no single magic number, but your revenue needs to be high enough to comfortably cover the new loan payments. Lenders will look closely at your revenue trends to make sure sales are steady or, even better, growing.

Lenders aren’t just looking at a single number; they are analyzing the story your financials tell. Consistent revenue and a solid operational history suggest a lower-risk investment for them.

Preparing Your Essential Documents

Nothing slows down a loan application like a missing document. Getting your paperwork in order before you even apply makes the whole process smoother and shows the lender you’re organized and serious.

Here’s a checklist of what you should have ready to go:

- Business Tax Returns: Have the last two to three years of your federal tax returns on hand. This is how lenders verify your profitability.

- Business Bank Statements: Get three to six months of your most recent statements together. This is the primary way lenders will analyze your cash flow and daily balances.

- Financial Statements: This means your Profit and Loss (P&L) statement, balance sheet, and statement of cash flows. You'll likely need them for the previous year and the current year-to-date.

- Business Plan: This isn't always required, but for a new business or a very large loan request, it’s a must. Your plan should clearly explain how you'll use the funds and include realistic financial projections.

- Legal Documents: Keep copies of your articles of incorporation, business licenses, commercial leases, and any franchise or partnership agreements easily accessible.

Understanding the True Cost of Your Loan

The interest rate on a business loan is a lot like the tip of an iceberg. It’s the first number you see, but it’s what’s hiding below the surface that really tells you the whole story. To truly grasp what you’ll be paying, you have to look past that initial rate and understand the total cost of borrowing.

Making a smart financial decision means comparing loan offers on an even playing field. You have to look beyond the sticker price—the interest rate—and dig into all the components that make up the loan's true cost. It’s not unheard of for a loan with a lower interest rate to actually be more expensive once all the fees are factored in.

Interest Rate vs. APR: What Is the Difference?

The first and most important distinction to get your head around is the difference between an interest rate and the Annual Percentage Rate (APR). They sound similar, but the APR provides a much clearer, more honest picture of what you’ll actually pay over the course of a year.

The interest rate is simply the percentage the lender charges for the privilege of borrowing their money. It's the core cost, for sure, but it doesn't include any of the other fees the lender might tack on for setting up and managing the loan.

The Annual Percentage Rate (APR), on the other hand, bundles that interest rate with most of the lender’s fees. It then expresses that total cost as a single annual percentage.

Here’s a simple way to think about it:

- Interest Rate: The price of the raw ingredients for a meal.

- APR: The final price of the meal on the menu, which includes the cost of the ingredients plus the chef's time and the restaurant's service charge.

Because the APR includes both interest and fees, it’s almost always higher than the simple interest rate. It is, without a doubt, the best tool you have for making a true apples-to-apples comparison between loan offers. A loan with a lower interest rate but high fees could easily have a higher APR than one with a slightly higher rate but minimal fees.

When you're weighing different business term loan offers, always anchor your comparison to the APR. It’s the most transparent metric for understanding the total cost of financing and will save you from getting blindsided by hidden charges.

Uncovering Common Loan Fees and Charges

So, what are these fees that get rolled into the APR? They can vary quite a bit from one lender to the next, but a few common ones pop up time and time again. Knowing what to look for helps you evaluate whether a loan’s fee structure feels right for your business.

Origination Fee: This is one of the most common costs. It covers the lender's administrative work in processing and underwriting your application. It’s typically a percentage of the total loan amount, often between 1% and 5%. On a $100,000 loan, that’s an upfront cost of $1,000 to $5,000, which is usually deducted right from the funds you receive.

Underwriting Fee: This is very similar to an origination fee and covers the deep dive the lender does into your business’s financial health. Think of it as the cost for them to verify your documents, run credit checks, and complete their risk assessment. Some lenders just roll this into the origination fee, while others list it as a separate line item.

Prepayment Penalty: This is a big one to watch out for. A prepayment penalty is a fee a lender charges if you decide to pay your loan off ahead of schedule. Lenders make their profit from the interest you pay over the full life of the loan. If you pay it back early, they miss out on that expected income, and this fee is their way of getting some of it back. If you think there's a chance you'll have extra cash flow to clear your debt early, make sure you find a loan with no prepayment penalty.

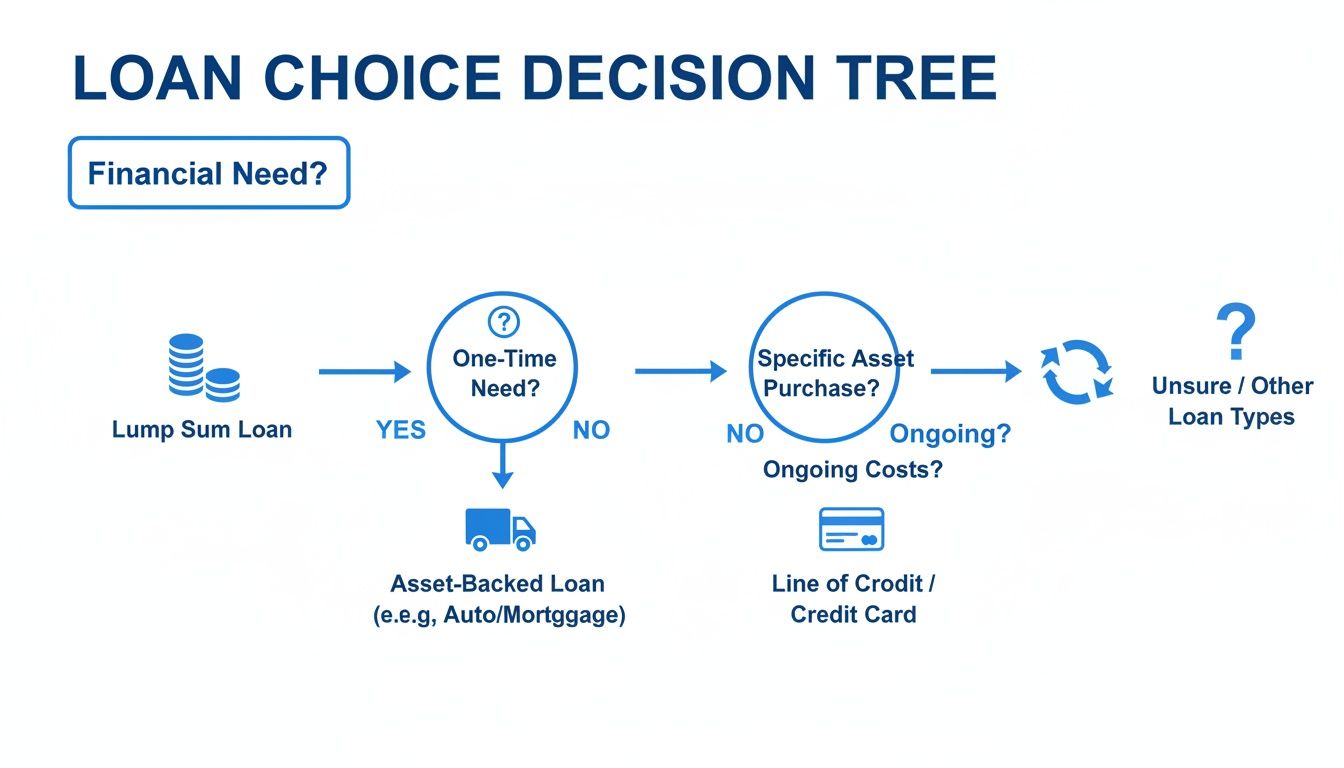

Is a Term Loan the Right Choice? A Look at Your Other Options

A business term loan can be a powerful engine for growth, but it's not the only tool in the shed. The world of business financing is packed with different options, and picking the right one is a crucial strategic decision. Get it right, and you accelerate your success. Get it wrong, and you could create unnecessary financial headaches.

The core principle is simple: match the funding to the specific problem you're trying to solve. You wouldn't use a sledgehammer to hang a picture frame, right? In the same way, a term loan is perfect for certain jobs, while a line of credit or equipment financing is better suited for others. Choosing incorrectly might mean paying for features you don't need or getting locked into a rigid payment plan when what you really needed was flexibility.

This decision tree can help you visualize which path makes the most sense for your immediate business need.

As the diagram shows, your choice really comes down to what you're trying to accomplish. Is it a one-time purchase, covering ongoing costs, or buying a specific asset? Your answer points you to the right type of capital.

When a Term Loan Makes the Most Sense

A business term loan truly shines when you're facing a specific, large, one-time expense with a clear price tag. Its entire structure is built for planned investments that will create long-term value for your company.

It’s probably the right move if you are:

- Expanding to a new location: You know the cost of the lease, renovations, and initial stock.

- Acquiring another business: The purchase price is a fixed, non-negotiable number.

- Launching a major marketing push: The campaign budget has been clearly defined ahead of time.

The predictability of a term loan is its greatest strength. With fixed payments and a set schedule, you can budget for these big projects with complete confidence.

When a Business Line of Credit is Better

Think of a business line of credit as a credit card for your company. It gives you a revolving credit limit you can draw from, pay back, and then draw from again whenever you need to. This makes it the perfect solution for managing day-to-day uncertainty and plugging short-term cash flow gaps.

A line of credit is the superior choice for:

- Handling seasonal dips in sales: Cover payroll and other expenses during your slow months without stress.

- Dealing with unexpected emergencies: Pay for a sudden equipment repair without derailing your operations.

- Bridging the gap while waiting on client payments: Keep your working capital healthy while invoices are outstanding.

Best of all, you only pay interest on the funds you actually use, making it an incredibly cost-effective safety net.

When to Use Equipment Financing

If your funding need is tied directly to a physical piece of machinery or equipment, then equipment financing is almost always the most logical path. In this arrangement, the new equipment itself serves as the collateral for the loan.

This is the go-to option for scenarios like:

- A construction company buying a new excavator.

- A restaurant upgrading its kitchen with commercial-grade ovens.

- A logistics firm adding new delivery trucks to its fleet.

Because the loan is secured by a hard asset, qualifying can sometimes be easier than for an unsecured term loan. Plus, the repayment term is often structured to align with the equipment's expected useful life.

The global demand for business financing is massive. Valued at roughly USD 8 trillion in 2023, the market is projected to swell to USD 12.5 trillion by 2032. Within this landscape, the demand for small business term loans remains particularly strong, with new originations jumping 9.2% year-over-year in Q2 2025. You can dig deeper into the global business loan market and what's driving its growth.

Your Guide to the Modern Loan Application Process

Forget the old days of business financing—the weeks spent waiting, the mountains of paperwork, and the endless back-and-forth with a loan officer. Technology has completely overhauled the process for getting a business term loan, making it faster and far more straightforward for entrepreneurs. Today, you can often apply online in a matter of minutes and have funds in your account within days.

This isn't just a minor tweak; it's a massive shift driven by financial technology. The fintech lending boom is fundamentally changing how businesses get the capital they need. In fact, the global fintech lending market is on track to hit an incredible USD 590 billion by 2025. This explosion shows just how much business owners prefer tech-driven solutions over old-school, paper-clogged banking. You can get a deeper look into how fintech is changing business lending and what these changes mean for you.

From First Click to Funded: Your Step-by-Step Digital Journey

The modern loan application is designed to be a clear, logical journey that gets you from point A to point B with minimal hassle. While every lender has its own quirks, the core steps are pretty much the same across the board.

Fill Out a Quick Online Form: It all starts with a simple, secure online application. You'll enter basic information about your business—name, industry, how long you've been operating, and your rough annual revenue. This first step usually takes less than 15 minutes.

Upload Your Documents Digitally: No more printers, scanners, or fax machines. You’ll just securely upload digital copies of your documents. Many lenders even let you link your business bank account, which gives them read-only access to verify your cash flow instantly. It's safe, secure, and incredibly fast.

Review and Compare Your Offers: Once your info is submitted, you'll typically get one or more preliminary loan offers. This is your chance to compare the important stuff: the loan amount, term length, interest rate, and the all-important APR. If you're working with a funding advisor, they can help you break down what each offer really means for your business.

Final Underwriting and Approval: After you've picked an offer, the lender does one last deep dive into your business's financial health. But thanks to automated systems, this final check usually takes just a few hours, not the weeks it used to.

E-Sign and Get Your Funds: With final approval, you’ll get a loan agreement to sign electronically. Once that’s done, the money is wired directly into your business bank account, often landing within 24 to 48 hours.

The whole point of the modern process is to get capital into your hands without derailing your business. Technology does the heavy lifting so you can stay focused on what you do best.

By knowing what to expect, you can walk into the process with confidence. This efficient path to funding saves you time and stress, letting you secure the financing your company needs to take that next big step.

Common Questions About Business Term Loans

Diving into the world of business term loans always kicks up a few questions. Let's tackle some of the most common ones that business owners ask, giving you the clear, straightforward answers you need to move forward with confidence.

What Is a Good Interest Rate for a Business Term Loan?

That's the million-dollar question, isn't it? What's considered a "good" rate really boils down to your specific business profile and the overall economic environment. If you're running a well-established business with rock-solid financials and a great credit score, you might see rates from a traditional bank in the 6% to 9% range. That’s a fantastic deal.

But most businesses don't fit that perfect mold. For everyone else, particularly those turning to online lenders, the rates typically start around 10% and can go up to 25% or even higher. The rate you’re offered will be a direct reflection of your credit score, annual revenue, and how much risk the lender thinks they’re taking on.

Can I Get a Loan with Less-Than-Perfect Credit?

Absolutely. While it’s true that big banks often want to see a personal credit score of 680 or higher, the lending world has changed. Many online and alternative lenders have built their entire business model around helping owners with imperfect credit.

Just know there's a trade-off. To balance out the higher risk, these lenders will almost certainly charge higher interest rates. They might also ask for a shorter repayment window or require you to put up specific collateral to secure the loan.

A lower credit score doesn't close the door to funding. It just reroutes you to a different set of lenders who often care more about your recent cash flow than your past credit history.

How Quickly Can I Receive the Funds?

The funding timeline is one of the biggest differences between lenders. If you go the traditional bank route, get ready to be patient. Their in-depth, manual underwriting process often means you'll be waiting anywhere from 30 to 90 days to see the money.

On the flip side, online lenders and modern fintech platforms are built for speed. Their digital applications and automated systems can slash that timeline dramatically. It's not uncommon to apply, get approved, and have the funds hit your business bank account within 24 to 72 hours.

Are There Penalties for Paying a Loan Off Early?

This is a crucial detail you have to check before signing on the dotted line. Some lenders, especially more traditional ones, will include a prepayment penalty in the loan agreement. This is basically a fee they charge to make up for the interest they'll miss out on if you pay the loan back ahead of schedule.

Thankfully, many modern lenders have done away with these penalties, offering you the freedom to pay down debt faster when your business has a great month. Always read the fine print in your loan agreement to see what the policy is—it can make a big difference to your total cost of borrowing if you plan to pay it off early.

Finding the right business term loan can feel like searching for a needle in a haystack, but you don't have to go it alone. The experts at FSE - Funding Solution Experts are here to help you sort through the noise and connect you with a lender that actually fits your business. Get a no-obligation quote today.