It’s a frustratingly common story for entrepreneurs: your income statement shows a healthy profit, but your bank account is running on fumes. This is the classic cash flow problem in a nutshell. It highlights a critical lesson every business owner has to learn—profit on paper doesn't pay the bills. The real measure of your company's financial health is the actual cash moving in and out of the business.

Why Profit Is Not the Same As Cash

Many business owners fall into the trap of thinking that if the company is profitable, it must be financially secure. That’s a dangerous misconception because it completely ignores timing. Profit is just an accounting concept, a long-term score. Cash flow, on the other hand, is the immediate, real-world fuel that keeps your lights on and your doors open.

Here’s an easy way to think about it: Profit is like your total net worth, including assets like your house and retirement accounts. Cash is the money in your wallet that you need to buy groceries and pay your mortgage this week. You can have a high net worth but still be in a tough spot if you can't access cash for immediate expenses. It’s the exact same principle in business.

The Real-World Impact of Poor Cash Flow

This isn't just some abstract financial theory; it’s a massive challenge for businesses everywhere. In fact, recent data shows that a staggering 51% of small businesses grapple with uneven cash flow, making it their third biggest financial hurdle. Unfortunately, it seems to be getting worse, with more businesses taking on debt just to cover basic operating costs. You can dig into more small business statistics on Kaplan Collection Agency to see the full picture.

When you're stuck in a cash crunch, the consequences hit hard and fast, sending ripples through your entire operation.

- Inability to Pay Bills: You might find yourself struggling to pay suppliers, rent, or utilities on time, which can quickly damage your business credit and essential relationships.

- Payroll Stress: Making payroll becomes a constant worry, a stressful scramble that takes a toll on employee morale and can lead to you losing great people.

- Missed Growth Opportunities: You might have to pass on big orders or exciting new projects simply because you don't have the cash on hand for inventory or new hires.

- Increased Debt: To bridge the gap, many owners turn to high-interest credit cards or short-term loans, which can easily spiral into a difficult cycle of debt.

A business can be profitable on paper and still go under because it runs out of cash. Think of cash as the oxygen that keeps your business alive, while profit is a measure of its long-term health.

Getting a handle on this fundamental difference is the first, most important step toward taking back control. This guide is your roadmap to figuring out what’s really causing your cash flow problems, putting immediate fixes in place, and building a proactive financial strategy for the future. You’ll learn how to build a stable, thriving business that doesn’t just look good on a spreadsheet but actually has the cash it needs to operate and grow.

Diagnosing the Root Causes of Your Cash Crunch

Before you can fix a leak, you have to find where the water is coming from. The same logic applies to your business finances. A cash crunch is just a symptom, not the disease itself. To get a real handle on your cash flow, you need to look beyond the bank balance and pinpoint the operational snags that are draining your resources.

Think of yourself as a financial detective for a moment. Your mission is to figure out exactly where your cash is getting stuck. By investigating the four most common culprits, you can stop reacting to financial emergencies and start building a more stable, predictable business.

H3: Late Payments and Piling-Up Receivables

This is the classic cash flow killer. You’ve done the work, delivered the product, and sent the invoice, but the payment is nowhere in sight. This gap between earning the money and actually having it in your bank account creates a growing "accounts receivable" balance—basically, a long list of IOUs from your customers.

When this problem gets out of hand, the warning signs are pretty clear. Your Days Sales Outstanding (DSO), which is the average time it takes to get paid, starts creeping up. You might also notice that your invoicing process is a mess of spreadsheets and manual reminders, letting overdue payments slip through the cracks. If you're heavily reliant on a few huge clients, a single late payment from one of them can throw your entire month off kilter.

H3: Bloated Overhead and Surprise Expenses

Your business could be pulling in great revenue, but if your fixed costs are sky-high or you’re constantly getting sideswiped by unexpected bills, that cash vanishes almost as fast as it comes in. High overhead is like a slow, constant drain on your bank account, leaving you with no cushion for emergencies or opportunities.

This is a real danger zone for small businesses. Cash reserves are notoriously thin across the board, and recent surveys show that nearly 4 in 10 businesses don't have enough cash to cover even one month of expenses. This vulnerability is especially tough on younger companies. You can find more details in this report on small business financial trends from OnDeck.

A profitable business with high overhead is like a bucket being filled with water but riddled with holes. No matter how fast you pour water in, it never gets full.

H3: Mismanaged Inventory

If you sell physical products, your inventory is literally cash sitting on a shelf. You absolutely need stock to meet customer demand, but holding too much of the wrong stuff ties up capital that you could be using for payroll, marketing, or paying down debt. This is one of the sneakiest cash flow problems small business owners run into.

You can spot an inventory problem by looking for a few key things. Is your inventory turnover low, meaning products are collecting dust for ages? Are your carrying costs for storage and insurance eating up profits? Do you find yourself constantly running deep discounts just to clear out old stock? These are all red flags.

H3: Seasonal Slowdowns

From construction companies in the winter to retail shops after the holidays, many businesses have predictable slow seasons. Everyone expects these dips, but failing to plan for them is what causes the cash crunch. If you don't save enough during your busy season, you'll find yourself scrambling to cover basic expenses when things quiet down.

The main clue here is a recurring pattern of financial stress that hits around the same time every year. Simply recognizing this cycle is the first step. From there, you can build a budget that smooths out those peaks and valleys, ensuring you have the cash on hand to operate confidently all year long.

Early Warning Signs of Cash Flow Trouble

Catching a cash flow problem early is key. Waiting until the bank account is empty means you're already in crisis mode. Use this quick checklist to see if any of these red flags are popping up in your business.

| Warning Sign | What It Means for Your Business | Immediate Action to Consider |

|---|---|---|

| Declining Cash Balance | Your expenses are consistently outpacing your income. | Review last month's bank statements to identify non-essential spending. |

| Customers Paying Later | Your Accounts Receivable is growing, tying up working capital. | Tighten your invoicing process; follow up on all overdue invoices immediately. |

| Relying on Credit for Payroll | You lack the operational cash to cover your most basic obligations. | Create a simple 13-week cash flow forecast to predict future shortfalls. |

| Struggling to Pay Suppliers | Your Accounts Payable is aging, which can damage supplier relationships. | Contact suppliers to negotiate extended payment terms before you miss a payment. |

| Maxed-Out Line of Credit | Your primary safety net is gone, leaving you with no buffer for emergencies. | Explore alternative financing options before you are forced to take a bad deal. |

| Cutting Prices to Make Sales | You're sacrificing profitability for immediate cash, a non-sustainable model. | Focus sales efforts on your most profitable products or services. |

If you've checked off more than one or two of these, it’s a clear signal that you need to dig deeper into your finances right away. These signs are your business’s way of telling you that something needs to change before a small issue becomes a major problem.

Quick Fixes to Improve Your Cash Position Now

When your bank account is getting dangerously low and payroll is looming, you don’t have time to map out a five-year plan. You need cash, and you need it now. These short-term fixes are your financial first-aid kit, designed to stop the bleeding and get your business back on stable ground.

Think of these as levers you can pull immediately. We’re not overhauling the engine right now; we’re just getting enough fuel in the tank to get to the next station. By speeding up your income and smartly slowing down your expenses, you can create the breathing room you desperately need to tackle the bigger issues.

Accelerate Your Accounts Receivable

The fastest way to boost your cash reserves is to collect the money you’re already owed. Every dollar sitting in your accounts receivable is a dollar that isn't paying your bills or funding your growth. For most small businesses, tightening up the collections process is the single most powerful way to fix immediate cash flow problems.

Here are a few tactics that work right away:

- Offer Early Payment Discounts: It might sound counterintuitive, but offering a small discount like 2% off for paying within 10 days (often called "2/10 net 30") can work wonders. That small hit on your margin is often a price worth paying for immediate cash in hand.

- Automate Invoice Reminders: Let technology do the nagging for you. Set up your accounting software to send polite, automated reminders when invoices are coming due and when they're overdue. It keeps you on your customers' radar without manual effort.

- Make Paying Easier: Don't make your customers jump through hoops. If you're not already, start accepting online payments, credit cards, or bank transfers. The simpler you make it to pay, the faster you'll get paid.

Strategically Manage Your Payables

Just as crucial as getting cash in the door is controlling when it goes out. This isn't about dodging your responsibilities. It’s about strategically timing your payments to line up better with your income. Pushing a large payment back by even a few days can make a huge difference when things are tight.

Take a hard look at your upcoming bills and sort them into "must-pay-now" and "can-wait" piles. Payroll and rent are non-negotiable. But you might have some wiggle room with other vendors.

A quick, honest phone call to a key supplier before a payment is late can do more than just buy you time—it can strengthen the relationship. Many vendors will happily grant a short extension, like moving from net-30 to net-45, if you’re proactive and transparent.

Liquidate Slow-Moving Inventory

If you sell physical products, your inventory is basically cash sitting on a shelf. Any item that isn't selling is actively costing you money in storage fees and lost opportunities. It’s time to turn that dead stock back into cash.

Consider these options to get products moving:

- Run a Flash Sale: Create a sense of urgency with a limited-time, deep discount on the items you need to clear out. It’s a great way to generate a quick injection of cash.

- Bundle Products: Pair a slow-moving item with one of your bestsellers. This boosts the perceived value and helps you move inventory that would otherwise just sit there.

- Contact a Liquidator: If you have a large amount of excess stock, a liquidator can buy it all at once. You'll get less per item, but you’ll get immediate cash and free up valuable space.

Putting these targeted fixes into action can build a much-needed cash buffer. They aren't the final answer, but they are critical emergency measures that give you the stability to step back and build a healthier long-term financial strategy.

Building Long-Term Financial Health with Cash Flow Forecasting

Those immediate fixes are great for getting out of a tight spot, but let's be honest—they're reactive. You're playing defense. To truly solve your cash flow problems for good, you have to get on the offense. That means shifting your mindset from day-to-day survival to building a system that lets you see what's coming down the road.

This proactive approach all comes down to one core discipline: cash flow forecasting. Think of it as your business’s financial weather report. Instead of being surprised by a sudden storm, you see it forming weeks out, giving you plenty of time to batten down the hatches, adjust course, and sail right through it.

From Guesswork to Strategic Control

At its heart, cash flow forecasting is a pretty straightforward exercise. You’re simply making an educated guess about how much cash will move in and out of your business over a set period. This isn't about getting bogged down in complex accounting or needing a crystal ball. It’s about replacing that nagging uncertainty with a clear, data-driven picture of where you're headed.

For most small businesses, the 13-week cash flow forecast is the gold standard. A rolling three-month window is the perfect timeframe—long enough to spot developing trends and potential shortfalls, but short enough to be reasonably accurate and actionable. It helps you answer the really critical questions, like, "Will we have enough cash to make payroll in six weeks?" or "Can we actually afford that new piece of equipment next month?"

Creating Your First 13-Week Forecast

Getting started is far less intimidating than it sounds. You don’t need fancy software; a basic spreadsheet is more than enough to map out your financial future. The whole process really boils down to tracking two things, week by week.

- Project Your Cash Inflows: This is all the money you expect to come in. Look at your sales pipeline, your historical sales data, and your accounts receivable aging report to estimate when you'll actually see customer payments land in your bank account.

- Map Out Your Cash Outflows: List every single expense you anticipate over the next 13 weeks. This includes your fixed costs like rent and salaries, but also the variable ones like payments to suppliers, marketing campaigns, and inventory buys. The key is to be realistic and thorough.

Once you have those two lists, you can create a simple weekly summary: Beginning Cash + Expected Inflows - Expected Outflows = Ending Cash. Update this forecast every single week, and you’ll always have a forward-looking view of your cash position.

A cash flow forecast transforms you from a passenger in your business to the pilot. It gives you the control to make informed decisions, avoid obstacles, and confidently steer your company toward its goals.

Having this level of financial command is absolutely vital right now. Managing cash flow has become a huge concern for entrepreneurs everywhere. Recent data shows that while 48% of small business owners point to inflation as their top worry, cash flow uncertainty is right behind it, with an alarming 72% ranking it among their top three concerns. You can dig into the numbers in this small business trends report from Ocrolus.

The Strategic Benefits of Forecasting

Beyond just keeping the lights on, a reliable forecast becomes a powerful strategic tool. It gives you the confidence to jump on growth opportunities because you know you have the cash to back them up.

Perhaps most importantly, it shows lenders and investors that you have a masterful handle on your company's finances. When you can walk into a bank and show them exactly how you'll manage your cash to repay a loan, you instantly become a much stronger, more credible candidate for funding.

Smart Financing Options to Bridge Cash Flow Gaps

Even with the best forecasting and tightest spending controls, there are times when a small business just needs an injection of capital. It might be to survive a temporary shortfall, jump on a sudden growth opportunity, or simply smooth out the cash flow bumps from a seasonal business cycle.

When you're dealing with cash flow problems, small business financing can feel like a tangled, confusing world. But getting to know the tools available means you can choose the right one for your specific situation, turning a potential crisis into a strategic step forward.

Finding the Right Tool for the Job

Not all funding is created equal. Grabbing the wrong kind of financing can actually make things worse, locking you into bad terms or a repayment schedule that strangles your revenue cycle. The trick is to match the solution to the specific problem you're trying to solve.

Let’s walk through some of the most common and effective options.

Common Financing Solutions Explained

Revolving Lines of Credit: Think of this as your business's financial safety net. A line of credit gives you access to a pool of funds you can draw from whenever you need it and repay over time. Critically, you only pay interest on what you use, making it perfect for covering unexpected costs or bridging short-term gaps between paying your bills and getting paid.

Merchant Cash Advances (MCA): For businesses with a high volume of daily credit and debit card sales—like restaurants, coffee shops, or retail stores—an MCA is a fast way to get cash. A funder provides a lump sum in exchange for a percentage of your future card sales. Since repayments adjust automatically with your sales volume, they ease up when business is slow.

Equipment Financing: If a vital piece of machinery goes down or you need to add capacity to land a big new contract, this is the tool you need. This type of loan is specifically for buying new or used equipment, and the asset itself usually serves as the collateral. It’s a great way to get the tools you need to make money without draining your bank account.

Navigating the Lending World with a Partner

When you're in a pinch, the last thing you have time for is filling out stacks of paperwork at a traditional bank, only to wait weeks for a "no." This is where working with a strategic funding partner changes the game. At FSE - Funding Solution Experts, we specialize in finding the right capital for businesses, especially those who don't fit the rigid mold of conventional lenders.

We become your dedicated advisor, connecting you to a network of over 50 different lenders to find the absolute best fit for your unique circumstances. We know that cash flow issues are urgent, so our process is built to be fast and painless.

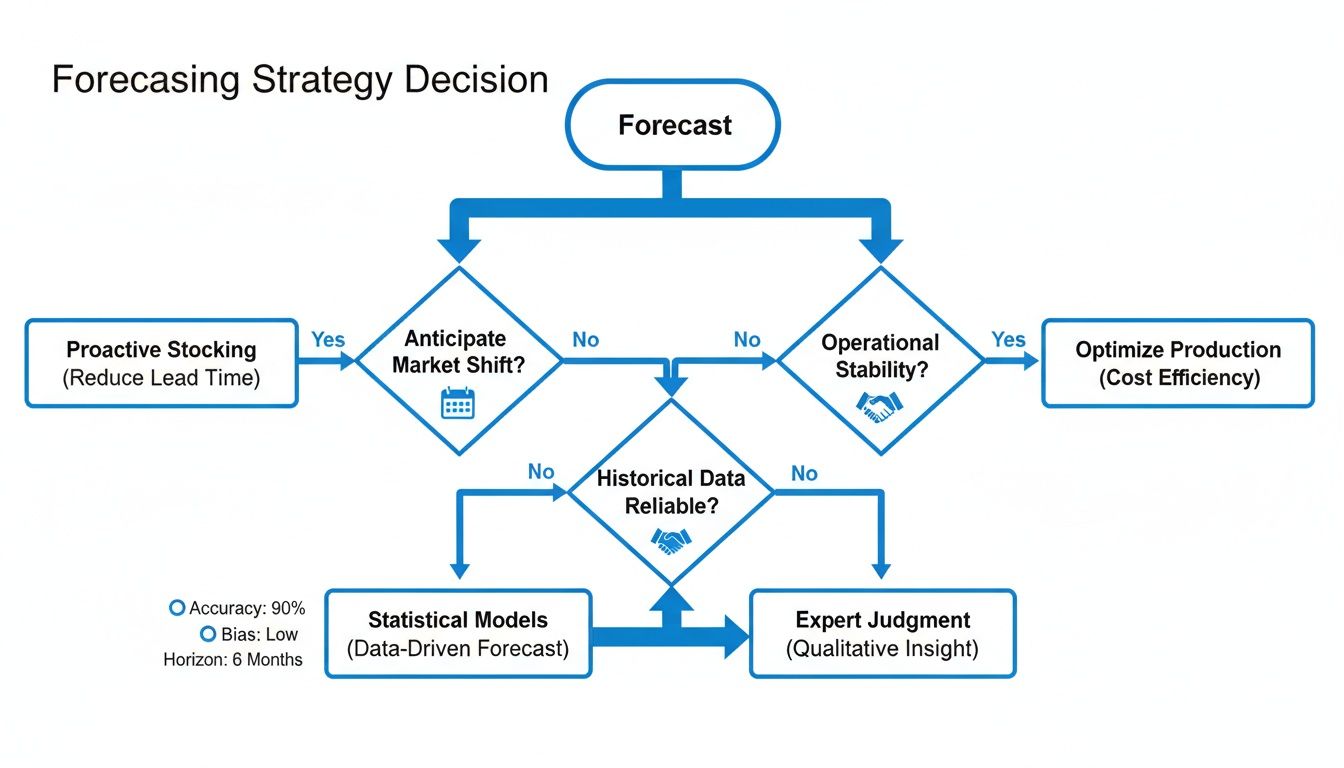

The flowchart below shows how a good forecast helps you see shortages coming and demonstrates to lenders that you have your finances under control—making you a much stronger applicant.

This decision tree highlights a key point: a solid forecast gives you the power to either brace for impact or prove to lenders that you’re a safe bet.

Comparison of Small Business Financing Solutions

Choosing the right financing option requires a clear-eyed look at the pros and cons of each. A solution that’s perfect for a local trucking company might be a disaster for a downtown boutique. To help clarify your options, we've put together a comparative overview of common financing products.

This table breaks down the key differences to help you see which solution might align best with your business's immediate needs and long-term goals.

| Financing Option | Best For | Key Benefit | Main Consideration |

|---|---|---|---|

| Revolving Line of Credit | Ongoing, flexible access to working capital for unexpected expenses or seasonal dips. | Flexibility. You only draw and pay interest on what you need, when you need it. | Often requires a stronger credit profile and more documentation than other options. |

| Merchant Cash Advance (MCA) | Businesses with consistent credit/debit card sales needing very fast cash. | Speed and Accessibility. Funding can be secured in as little as 24 hours with minimal paperwork. | The cost of capital can be higher than traditional loans; payments are tied to daily sales. |

| Equipment Financing | Acquiring specific machinery or vehicles without a large upfront cash payment. | Preserves Cash Flow. Allows you to get revenue-generating assets working for you immediately. | The loan is secured by the equipment, meaning the asset is at risk if you default. |

| Reverse Consolidation | Businesses juggling multiple expensive daily or weekly payments from other advances. | Cash Flow Relief. Consolidates payments into a single, smaller, more manageable payment. | This is a debt management tool, not new working capital; it’s designed to improve daily cash position. |

Understanding these distinctions is the first step toward making a confident decision that supports your business instead of hindering it.

When to Seek Expert Guidance

It’s easy to feel overwhelmed by the choices, especially when you're under pressure to make payroll. If you’re spending more time worrying about your bank balance than focusing on your customers, that’s a pretty clear sign it’s time to ask for help. An experienced funding advisor can quickly size up your situation and point you toward solutions you may not have even known existed.

At FSE, we keep the qualification process simple because we know how small businesses operate.

Our eligibility criteria are straightforward:

- At least one year in business

- A minimum of $10,000 in monthly revenue

If you meet those two simple benchmarks, you could be well on your way to securing the capital you need. Our job is to remove the stress and guesswork from the funding process, presenting you with clear, understandable offers so you can make an informed decision with confidence.

Ultimately, financing is a tool. When used correctly, it can solve the immediate cash flow problems small business owners face and pave the way for long-term stability and growth. You don't have to face these challenges alone; the right expertise is out there.

Your Action Plan for Mastering Small Business Cash Flow

Alright, we’ve covered a lot of ground—from spotting the warning signs to exploring real-world solutions. But just reading about it won't change a thing. The real power comes from putting that knowledge to work. This is the moment you shift from theory to building a stronger, more cash-healthy business.

Let’s make sure this guide doesn't just collect dust. This simple, time-based checklist is designed to help you build momentum. Start with one task, then the next. You'll be surprised how quickly these small steps add up to real financial stability.

Your First Steps to Financial Control

This isn't about overhauling your entire business overnight. It's about taking clear, manageable steps that create immediate relief while building good financial habits for the long haul.

This Week: Time for a quick cash flow diagnosis. Pull up your last 90 days of bank statements. Your mission is to find two things: your top three non-essential expenses to cut and the top three clients who always pay late. This is your ground zero.

Tomorrow: Pick one new invoicing tactic and run with it. Seriously, just one. Maybe it's offering a 2% discount for paying early or finally setting up those automated follow-up emails. Take a single, concrete step to get paid faster.

This Month: Build your first 13-week cash flow forecast. Don't overthink it—a simple spreadsheet will do. Mapping out your expected cash in and cash out is the single most important thing you can do to start making decisions proactively instead of reactively.

Next Month: Take an honest look at your financing needs. With your forecast in hand, you'll see any potential shortfalls coming. Now you can decide if a strategic funding option makes sense to bridge a gap, build a safety net, or jump on a growth opportunity.

You don't have to figure all this out on your own. The smartest business owners I know are the ones who aren't afraid to ask for expert advice when they're stuck or see a chance to get ahead.

If your diagnosis uncovers a serious cash gap or you’ve identified a major opportunity you can't afford to miss, it’s time to act. Speaking with a funding advisor can bring clarity to a confusing situation and help you secure the capital you need.

The team at FSE - Funding Solution Experts is here to help with a no-obligation consultation to walk through your options and find the right path forward. It's time to take control.

Frequently Asked Questions

When you're in the trenches running a business, financial questions are bound to come up. Let's tackle some of the most common ones we hear from owners who are trying to get a handle on their cash flow.

How Can My Business Be Profitable But Still Have No Cash?

This is the classic paradox that trips up so many entrepreneurs, and it's a great question. The answer lies in the difference between profit on paper and actual cash in the bank.

Profit is an accounting concept. You might close a $20,000 deal in May and record that as profit, but if your client has 60 days to pay, you won't see that money until July. That two-month gap between earning the revenue and actually collecting the cash is where profitable businesses get into trouble. You’ve got bills to pay now, but your money is still tied up in receivables.

What Is the Fastest Way to Get Cash Into My Business?

When you need cash immediately, you have two paths you can take at the same time. The first is to look inward. You can speed up your collections by offering a small discount for early payment or simply get more assertive with follow-ups on overdue invoices. Another quick win can be a flash sale to turn any slow-moving inventory into immediate cash.

The second path is external financing. If you need a capital injection fast, options like a merchant cash advance or a business line of credit can often get funds into your account in as little as 24-48 hours.

How Often Should I Review My Cash Flow Statement?

As a rule of thumb, you should sit down with your cash flow statement at least once a month to understand where your money has gone. But the real game-changer is your cash flow forecast—your projection of what's coming in and going out. That needs a weekly look.

A weekly check-in on your forecast allows you to spot potential shortfalls weeks in advance, turning a potential crisis into a manageable issue. This proactive habit is a key differentiator between businesses that struggle and those that thrive.

Will a Business Line of Credit Solve All My Cash Flow Problems?

Honestly, no. Financing is a powerful tool, but it's not a magic wand. A line of credit is fantastic for covering unexpected expenses or bridging those temporary gaps between invoicing and getting paid. It’s a financial safety net.

What it won't do is fix fundamental problems like consistently low profit margins, bloated overhead costs, or a broken collections system. Think of it as a bridge to get you over a rough patch, not a new road. You should use it to solve the immediate cash flow problems small business owners face while you work on fixing the root cause for good.

If you're dealing with a cash gap and need to understand your options, the dedicated advisors at FSE - Funding Solution Experts can help. We work with a network of over 50 lenders to find the right fit for your situation. Learn more and see if you qualify at https://www.fseb2b.com.