Refinancing your commercial real estate means replacing your current mortgage with a new one—ideally, one with better terms. It's a strategic financial tune-up for your business. You swap an old loan for a new one that can help you lower your interest rate, adjust your loan term, or tap into your property's built-up equity. This move can free up cash flow or provide capital for growth.

Why Should I Consider Refinancing My Commercial Property?

Refinancing your commercial real estate is about making your biggest asset work smarter. For most businesses, the building is a dynamic financial tool. A commercial real estate refinance loan is how you put that tool to work.

This could mean:

- Slashing Monthly Payments: A lower interest rate directly cuts your mortgage bill.

- Unlocking Working Capital: A cash-out refinance lets you borrow against your equity for expansions or renovations.

- Changing Your Loan Term: Shorten the term to pay off the property faster, or extend it to lower monthly payments.

Staying Ahead of Market Shifts

The current economic climate makes refinancing a key topic. Many existing loans were signed in a much lower interest rate environment. Now, business owners must find new financing at today’s higher rates. You can explore commercial real estate loan dynamics on Agorareal.com.

Different Goals for Different Businesses

The "why" behind refinancing often comes down to your specific industry and needs. A logistics company might refinance to fund a warehouse expansion, while a restaurant owner might need capital to modernize their dining room.

Refinancing isn't just about managing debt. It's about actively steering your property's value toward your biggest business goals.

Top Reasons to Refinance Your Commercial Property

| Refinancing Goal | How It Helps Your Business | Best For Businesses That... |

|---|---|---|

| Lower Monthly Costs | Improves cash flow by reducing your largest fixed expense. | Have a high-interest loan and want to boost profitability. |

| Fund Expansion/Renovation | Provides a lump sum of capital by tapping into property equity. | Are growing and need capital to scale operations. |

| Consolidate Debt | Combines multiple high-interest debts into a single, lower-rate loan. | Are managing several debts and want to simplify payments. |

Understanding these options is the first step toward a smart, strategic decision.

Exploring the Different Flavors of Commercial Real Estate Refinancing

When refinancing, there's no magic bullet. You need to pick the right tool for the job. Each loan type is built for a specific purpose.

Rate-and-Term Refinance

This is the most straightforward option. You're swapping your current mortgage for a new one, usually to get a lower interest rate or change the loan's duration. The goal is to improve your monthly cash flow.

Cash-Out Refinance

Here, you’re tapping into your property's value to pull out a lump sum of cash. Your new loan will be larger than the old one. It’s a powerful move for business owners who need capital to grow.

A rate-and-term loan stabilizes finances. A cash-out loan fuels growth. Your choice should align with your business strategy.

Once you know your goal, you can dig into specific loan products. Recent data shows commercial lending momentum hitting its highest level since 2018. You can review these commercial real estate lending trends from CBRE.

Comparing Commercial Refinance Loan Types

| Loan Type | Best For | Typical LTV | Key Consideration |

|---|---|---|---|

| Conventional Bank Loan | Established businesses with strong credit. | Up to 75% | Rigorous underwriting process. |

| SBA 7(a) & 504 Loan | Small to mid-sized owner-occupied businesses. | Up to 90% | Government-backed, more paperwork. |

| CMBS (Conduit) Loan | Borrowers with non-standard properties. | Up to 75% | Less strict on borrower financials but inflexible. |

| Bridge Loan | Short-term needs, like acquiring a new property. | Up to 80% | Fast funding but higher interest rates. |

Let's explore what makes each unique.

Conventional Bank Loans

These are offered by banks and credit unions. They're a fantastic option for businesses with a solid track record and clean financials. They offer competitive rates but have strict qualification criteria.

SBA 504 and 7a Loans

The Small Business Administration (SBA) guarantees a portion of the loan, reducing the bank's risk. This makes SBA loans a lifeline for small and mid-sized businesses, especially for properties the business occupies.

CMBS Loans

Commercial Mortgage-Backed Securities (CMBS) loans are a different breed. Lenders pool multiple loans and sell them as bonds to investors. They can be more forgiving for borrowers who don't meet a conventional bank's standards. The trade-off is a lack of flexibility.

Bridge Loans

A bridge loan builds a short-term bridge over a financial gap, like buying a new property before selling an old one. They are fast but pricey, with higher interest rates and short terms.

How to Qualify for a CRE Refinance Loan

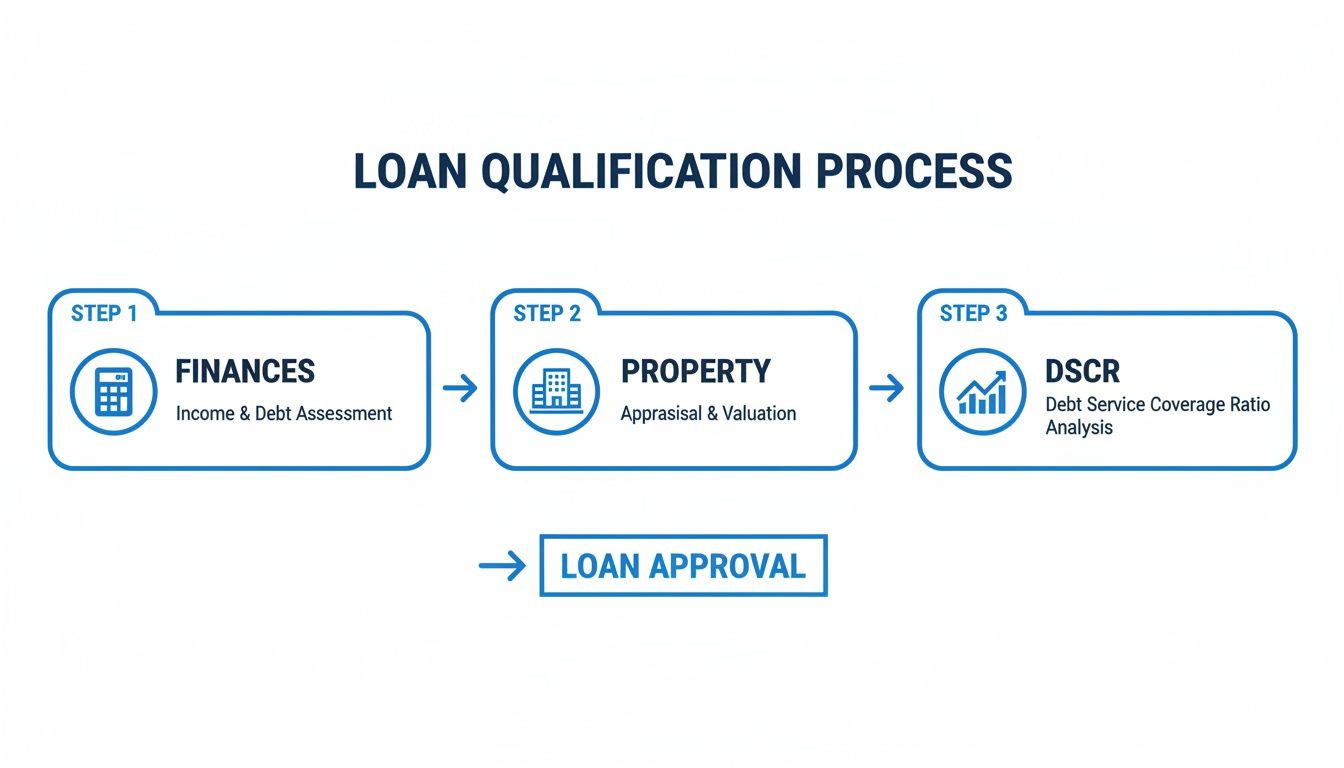

Getting approved is about building a compelling case that your property is a sound investment. Lenders look at three core pillars: the property's financial strength, your company's health, and your credit.

The Property’s Power to Pay

Lenders focus on the property's ability to generate cash flow. This is where the Debt Service Coverage Ratio (DSCR) is key. It answers one question: does the property make enough money to cover its mortgage payments?

The gold standard for DSCR is 1.25x. This tells a lender that for every $1.00 of mortgage debt, your property generates $1.25 in net income.

A ratio below 1.0x is an immediate deal-breaker.

Your Business Financials and Personal Credit

Your business financials and personal credit history are essential. Lenders need to see a track record of responsible financial management. They’ll ask for:

- Profit & Loss (P&L) Statements

- Business Tax Returns

- Personal Credit Score: You’ll generally need a score of 680 or higher.

Understanding Loan-to-Value (LTV)

The Loan-to-Value (LTV) ratio compares the loan amount to the property’s appraised value. If you need a $750,000 loan for a property valued at $1 million, your LTV is 75%. Most commercial refinance loans max out at an LTV of 75-80%. This is important as delinquency rates on some commercial loans have climbed. You can find more commercial real estate market risks from S&P Global.

Navigating the CRE Refinance Process Step by Step

The path to refinancing is a structured journey with clear stages. Knowing what's coming helps you prepare and avoid delays.

Stage 1: The Application and Document Submission

This is where you make your case on paper. You submit your loan application and provide a detailed financial snapshot. A typical document checklist includes:

- Business Financials: P&L statements and business tax returns.

- Personal Financials: Personal tax returns for all principal owners.

- Property Information: Current mortgage statement and a rent roll.

- Debt Schedule: A comprehensive list of all business debts.

Stage 2: Underwriting and Due Diligence

The underwriting team verifies your information and assesses risk. They will order a third-party appraisal to determine your property's current market value. This is used to calculate the final LTV ratio.

Underwriting is the most time-intensive part of the process. Respond immediately to any requests for additional information.

This flowchart breaks down the three core pillars an underwriter evaluates.

Stage 3: Approval and Closing

After underwriting, you’ll receive a loan commitment or term sheet. Review this document carefully. Once you accept, the process moves to closing. You'll sign the new loan agreement, and the lender will wire the funds. Your old loan is paid off, and any cash-out funds are transferred to your business account. The entire journey for a commercial real estate refinance loan typically takes 45 to 90 days.

How FSE Makes Your Refinance Happen

At Funding Solution Experts (FSE), we aren’t a bank—we’re your strategic partner. As an independent brokerage, FSE gives you direct access to a curated network of over 50 different lenders. This reach lets us find the perfect match for your situation.

Your Direct Path to Faster Funding

A slow "yes" can mean missing a critical opportunity. At FSE, we've stripped away the red tape. Our application is straightforward, and we can typically deliver a preliminary decision within just 24 hours.

We don’t just forward your application; we champion it. Our job is to pinpoint the lender most likely to say "yes," saving you time and energy.

More Options Mean a Better Deal

Working with FSE opens up a world of possibilities. Our network provides:

- Flexibility on Your Terms: We connect you with lenders who can work around challenges.

- Competitive Offers: Multiple interested lenders often result in better rates.

- Personalized Support: A dedicated advisor guides you through the entire process.

Common Questions About CRE Refinancing

Here are answers to common questions about a commercial real estate refinance loan.

How Long Does a CRE Refinance Take?

A traditional bank can take 60 to 90 days. Working with alternative lenders or a brokerage can cut that time down dramatically, often to just a few weeks.

What Is the Difference Between Commercial and Residential Refinancing?

A residential refinance is about your personal income and credit. A commercial refinance is all about the property and the business. Lenders analyze property income, and loan structures are different, often with shorter terms. The documentation is also far more intense.

A commercial refinance is a business transaction. The lender’s decision is driven by the property’s performance.

Can I Refinance with Less-Than-Perfect Credit?

Yes. While a high credit score is key for traditional banks, many alternative lenders are more flexible. They put more weight on factors like the asset's cash flow (DSCR) and its loan-to-value (LTV) ratio. A building that generates strong income can often make up for a ding on your personal credit.

Ready to see what your options are without the traditional bank runaround? The team at FSE - Funding Solution Experts can help you find the right commercial real estate refinance loan for your goals. You can start a no-obligation application today and get the expert answers you need to move your business forward.