Construction business loans are a specific type of financing built for the unique financial rollercoaster of the construction industry. They provide the essential cash needed to cover everything from raw materials and heavy machinery to simply making payroll while you wait for a project invoice to clear.

Why Traditional Bank Loans Often Miss the Mark for Contractors

You just won a massive bid—it's a game-changer for your company. The problem? Most of your cash is tied up in another job that won't pay out for another 60 days. This cash flow crunch is a daily reality in construction, where big upfront expenses and project-based revenue create a constant financial juggling act.

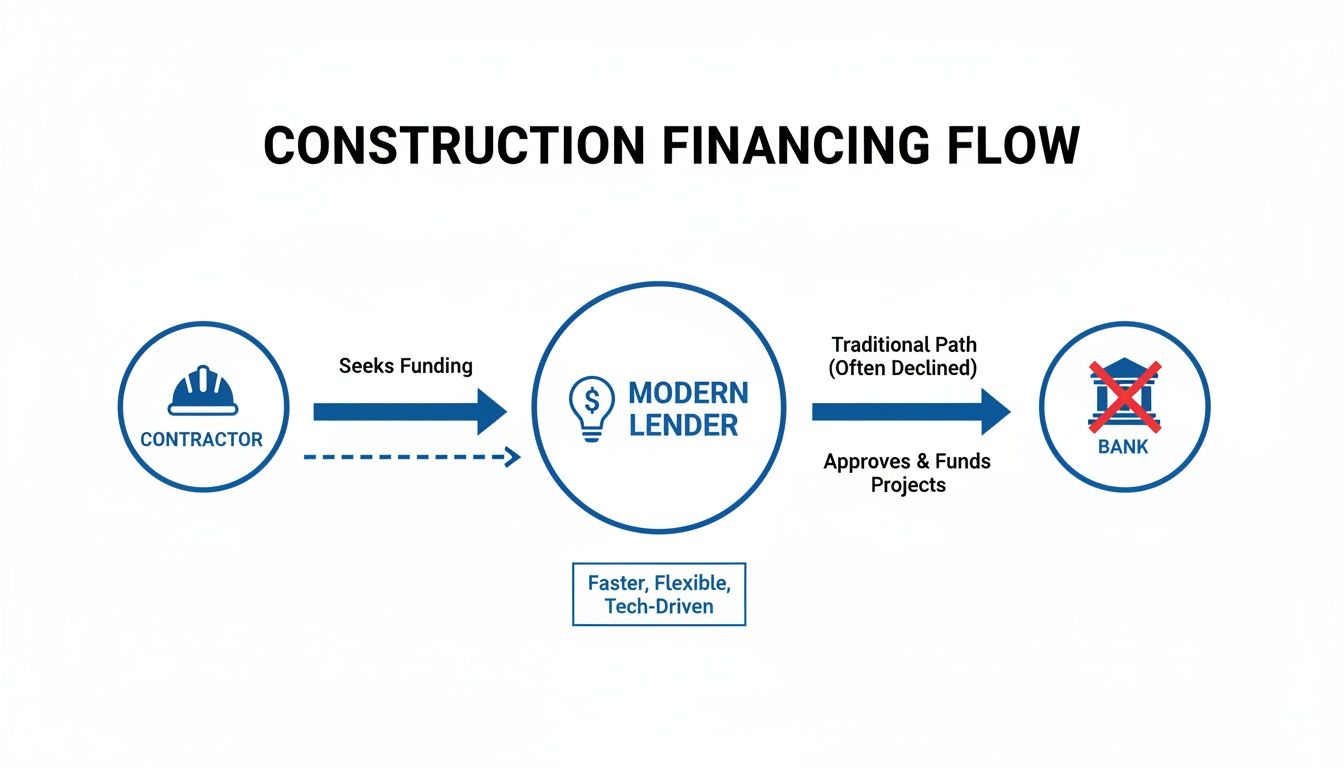

While your first instinct might be to walk into a traditional bank, their slow-moving, rigid processes are often out of sync with the fast-paced needs of a contractor. This gap leaves many construction business owners in a tough spot. A bank's approval process can drag on for weeks, even months—a lifetime when you need to order materials or bring on subs now.

The Disconnect Between Banking and Building

Simply put, many traditional lenders don't get the financial rhythm of the construction world. They're comfortable with businesses that have nice, steady, predictable monthly revenue. That’s the polar opposite of how most construction firms operate, where financial statements show huge cash infusions followed by periods of intense spending.

This fundamental lack of industry insight creates some common hurdles for contractors:

- Painfully Slow Approvals: A bank might take 60-90 days to say yes. By that time, the project you needed the funds for could be long gone.

- Strict Collateral Rules: Big banks often demand significant collateral that a growing construction company might not have free and clear.

- Inflexible Repayment Schedules: A fixed monthly payment doesn't work well when your income is tied to project milestones. This can create a cash flow squeeze even when you're profitable on paper.

At its core, the problem is that banks are designed for stability, but the construction industry runs on agility. A lender who doesn’t understand concepts like retainage, change orders, or mobilization costs can’t really meet a contractor's immediate capital needs.

The Need for a More Practical Solution

When you can't get funds quickly, your growth grinds to a halt. You miss out on bids, projects get delayed, and your reputation can take a hit. This is exactly why specialized financing solutions have become so critical.

Alternative lenders and financing experts offer construction business loans designed to fill this void. They provide the fast, flexible funding you need to jump on opportunities, manage day-to-day operations, and keep your projects on track without the bureaucratic friction. These options are built to work with your project timelines, not against them.

Understanding Your Construction Financing Options

Trying to navigate construction financing can feel like deciphering a complex blueprint for the first time. The jargon is thick, the options seem endless, and one wrong move could be a very expensive mistake. But just like any successful build, it all starts with understanding your tools.

Think of it this way: you wouldn't use a sledgehammer for finish carpentry. In the same vein, the financing you choose has to fit the job. Let's break down the most common types of construction business loans, so you can pick the right financial tool for whatever your project demands.

The modern funding landscape has shifted. Contractors no longer have to wait on slow, traditional banks and can instead partner with more agile lenders for faster access to the capital they need to grow.

The takeaway here is that specialized lenders provide a more direct, efficient path to funding, helping you sidestep the typical roadblocks and red tape you'd find at a conventional bank.

To help you get a clear picture, here's a quick comparison of the most common financing options available to contractors.

Comparing Construction Financing Options at a Glance

This table breaks down the key features of each loan type, making it easier to see which one aligns with your immediate business needs.

| Financing Type | Best For | Typical Loan Amount | Repayment Structure |

|---|---|---|---|

| Working Capital Loan | Daily operations, payroll, materials, bridging cash flow gaps | $5,000 - $500,000 | Short-term (3-24 months) with fixed daily or weekly payments |

| Equipment Financing | Purchasing new or used heavy machinery and vehicles | $10,000 - $5 million+ (based on equipment value) | Mid- to long-term (2-7 years) with fixed monthly payments |

| Business Line of Credit | Unexpected expenses, managing cash flow, seizing opportunities | $10,000 - $250,000 (revolving) | Pay interest only on what you use; funds replenish as you repay |

| Commercial Real Estate Loan | Buying land, constructing buildings, major property renovations | $250,000 - $10 million+ | Long-term (10-25 years) with fixed monthly payments |

Each of these tools has a specific purpose. Choosing the right one is about matching the solution to the problem you're trying to solve right now.

Working Capital Loans: The Fuel for Daily Operations

A working capital loan is the all-purpose fuel that keeps your business running day-to-day. It’s not designed for buying a new fleet of trucks, but rather for covering the short-term, operational costs that are a constant in the construction world.

Picture this: you're waiting on a client payment that's 30 days out, but you have payroll due this Friday. A working capital loan is what bridges that gap, making sure your crew gets paid and your project stays on schedule. They are essential for navigating the classic "feast or famine" cash flow cycles of this industry.

Common uses include:

- Covering payroll when client payments are delayed.

- Buying smaller tools and materials for an upcoming job.

- Paying for an unexpected repair on a critical piece of equipment.

- Funding marketing efforts to bid on bigger and better projects.

Equipment Financing: Acquiring Your Heavy Hitters

Every construction firm lives and dies by its machinery—excavators, bulldozers, cranes, you name it. Equipment financing is a loan created for one purpose: to help you buy that new or used heavy machinery. It works a lot like a car loan, where the piece of equipment you're buying acts as its own collateral.

This is an incredibly powerful tool because it lets you get your hands on revenue-generating assets without wiping out your cash reserves. Instead of a huge upfront payment, you make predictable monthly payments over the life of the loan, freeing up your working capital for everything else.

The demand is huge. The global construction equipment finance market is ballooning from $59.01 billion to $63.63 billion this year alone, and it's projected to hit nearly $90 billion by 2029. This surge shows just how much contractors rely on financing to stay competitive. It’s a vital lifeline, especially when 14.3% of large banks have made it harder to get traditional construction loans. You can discover more insights about this growing market and see how it impacts the industry.

Business Lines of Credit: Your Financial Safety Net

Think of a business line of credit as your financial safety net, always there when you need it. It’s a revolving source of funds that gives you access to a preset amount of capital, but here’s the key: you only pay interest on the money you actually use. Once you pay it back, the full amount is available to you again.

This flexibility is a perfect match for the construction industry, where surprises are just part of the job. A sudden spike in material costs or an emergency repair can derail a budget in a heartbeat. A line of credit lets you handle these costs immediately without having to go through a new loan application every single time.

A business line of credit gives you incredible flexibility. You can draw funds for emergencies or opportunities, repay them when you get paid, and have that capital ready for the next challenge. It’s a reliable financial buffer.

Commercial Real Estate Loans: Building Your Foundation

When you’re ready to think bigger—beyond a single project—and want to purchase or develop property, a commercial real estate (CRE) loan is the tool you need. These are long-term loans designed for buying land, constructing a new office, or undertaking a major renovation on a commercial building.

Given the large sums involved, these loans are more complex and have a much longer approval process. Lenders will want to see everything: the project's feasibility study, your company's financial history, and detailed construction plans. A CRE loan is a major commitment, but it’s how you fund the foundational assets of your business—a new headquarters, a workshop, or a storage yard—and build long-term equity.

What's the Lending Climate Like for Construction Today?

If you've tried to get a construction loan recently, you’ve probably noticed things feel different. The easy-money days of just a few years ago are gone, and the entire financial landscape has shifted. For construction business owners, understanding this new reality is the first step to getting the funding you need.

Think of it like planning a build during a volatile season. A few years ago, we had clear skies and a steady supply of affordable materials (low interest rates, accessible credit). Now, we’re dealing with unpredictable weather and supply chain issues (higher rates, tighter rules). Every single move has to be more deliberate and well-planned. Lenders are simply triple-checking the blueprints before they pour the foundation.

This isn’t personal—it's just business. Lenders are navigating their own economic pressures, like inflation and market uncertainty, and managing their risk accordingly. That, in turn, directly affects the kinds of loans and terms they can offer you.

Why Rates and Terms Have Toughened Up

The era of historically low interest rates is firmly in the rearview mirror, a change felt sharply across the construction industry. The cost for lenders to get their hands on capital has gone up, and they're passing that cost along to borrowers. The result is a general tightening of credit across the board.

For contractors, this means the goalposts have moved. A project that might have sailed through the approval process a couple of years ago now demands more from you: deeper financial documentation, a healthier down payment, and a rock-solid track record. It's definitely a more demanding environment, but it's far from impossible to navigate.

The bottom line is that lenders are betting on stability. They need to see that you have a firm grip on your business and a solid plan to handle today's realities, like rising material costs and potential labor delays. They need to know their investment is safe with you.

You can see the impact in the numbers. Current commercial construction loan rates are hovering between 6.8% and 13.8% for shorter-term financing, with residential projects falling somewhere between 6.25% and 9.75% APR. These rates are a direct response to a market with less available cash and lenders pulling back on how much of a project they're willing to fund. You can learn more about the factors driving construction loan interest rates and how to position your business for success.

Speaking the Lender's Language: Key Metrics You Need to Know

To get ahead in this climate, you have to talk the talk. That means getting comfortable with two critical terms: the Loan-to-Cost (LTC) ratio and the Loan-to-Value (LTV) ratio. These aren't just industry jargon; they are the core metrics lenders use to measure risk and decide how much they're willing to lend.

Loan-to-Cost (LTC) Ratio: This is a straightforward comparison of the loan amount to the total project cost. Not long ago, lenders might fund 80-85% of a project. Today, that number has dropped, with most lenders capping their LTC around 70-75%. That means you need to be prepared to bring more of your own cash to the table—often 25-30% of the total cost.

Loan-to-Value (LTV) Ratio: This ratio looks ahead, comparing the loan amount to the projected market value of the finished building. Lenders use this to ensure that if the worst happens, the completed asset will be valuable enough to cover the outstanding debt. It's their safety net.

Having to put more "skin in the game" with a lower LTC ratio shows lenders you're serious and financially invested in seeing the project through. It proves your confidence in the build and reduces their risk, which is exactly what they're looking for right now. Factoring in this larger equity contribution is no longer optional—it's an essential part of your initial project planning.

Your Step-by-Step Loan Application Checklist

Getting a construction loan isn't about crossing your fingers and hoping for the best—it's about solid preparation. Think of your loan application as the blueprint for your project. The more organized and detailed it is, the smoother and faster the build will go. Lenders are looking for a clear, convincing story about your business's financial stability and its potential for growth.

This checklist will help you gather every document you need, ensuring you present a professional and complete package that gives any lender confidence in your business. When you understand why each document matters, you can build a narrative that dramatically increases your chances of approval.

Phase 1: Assembling Your Core Financials

First things first, you need to establish your business's identity and track record. Lenders use these documents to verify that your company is legitimate and to get a baseline understanding of how it performs. This is the foundation of your entire application.

Here’s the core package you’ll need to pull together:

- Business and Personal Tax Returns: Lenders will want to see the last 2-3 years of returns to gauge your long-term profitability and confirm you're compliant.

- Bank Statements: Have 3-6 months of recent statements ready. This is how you demonstrate consistent cash flow, which is a key signal that you can manage your day-to-day finances.

- Financial Statements: This means your Profit & Loss (P&L) statement, balance sheet, and cash flow statement. Together, these reports provide a snapshot of your company's financial health at a specific moment in time.

- Business Licenses and Legal Documents: Don't forget your articles of incorporation, business licenses, and any other relevant permits that prove you are operating legally.

Think of this stage as building your business's resume. Each document contributes to a picture of a stable, well-managed company that a lender would see as a sound investment. A complete and organized package signals professionalism right from the start.

Phase 2: Outlining the Project and Its Profitability

Once you've established your financial history, the conversation shifts to the future. With a construction loan, lenders need to know exactly what you plan to do with the money and, more importantly, how it will generate revenue. This is your chance to sell the vision and prove it's a viable one.

This is especially true in the current market. Recent data shows a 7.5% surge in U.S. small business lending, with SBA 7(a) approvals hitting over $10 billion in a single quarter. At the same time, a 'Great Divide' is emerging as most banks tighten their lending standards, making it tougher for contractors to get approved. Construction businesses actually lead the pack in SBA approvals, which points to a huge opportunity for firms that can present a solid case to alternative lenders. You can read the full report on small business lending trends to see how your business can take advantage.

To build a compelling case for your project, you'll need:

- A Detailed Business Plan: This document should clearly lay out your company's mission, market analysis, and growth strategy. If the loan is for a specific project, explain how it fits into your bigger business goals.

- Comprehensive Project Plans: Provide any architectural drawings, engineering specs, and a detailed scope of work. Lenders want to see that the project is well-thought-out and professionally planned.

- Itemized Budget and Cost Estimates: Break down every single anticipated cost—from materials and labor to permits and a contingency fund. A thorough budget proves you've done your homework.

- Signed Construction Contracts: If you already have contracts in place with clients or GCs, include them. These are powerful proof of guaranteed future revenue streams.

How To Compare Loan Offers And Avoid Common Pitfalls

Landing several financing proposals can feel like a victory lap. Yet the real work starts now: untangling each offer so you don’t end up trapped by unexpected fees or unfavorable terms. Think of it like sorting through bids from subcontractors—one quote looks cheap until you see the charges for every extra mile, tool or certification. The goal is to find the package that aligns with your budget, schedule and growth ambitions.

Looking Beyond The Interest Rate

It’s tempting to zero in on the stated rate, but that number rarely tells the full story. Instead, turn your attention to the Annual Percentage Rate (APR), which rolls in interest plus most fees. Below is a snapshot of common cost factors you’ll encounter:

| Cost Factor | What It Means | Typical Impact |

|---|---|---|

| Origination Fee | One-time processing charge (1%–5% of the loan amount) | Adds $1,000–$5,000 on a $100,000 loan |

| Prepayment Penalty | Fee assessed if you pay off the loan early | Can lock you into higher costs even after project wrap |

| Factor Rate | Fixed multiplier for MCAs (e.g., 1.3) | Turns a $50,000 advance into $65,000 owed |

By tallying these expenses over the loan’s life, you can place each estimate side by side and compare true costs.

Aligning Repayment With Your Cash Flow

A repayment schedule that clashes with your billing cycle is a recipe for stress. Daily or weekly debits may look reasonable on paper, but slow stretches between jobs can leave you scrambling. The secret is mapping payment dates directly to your invoicing calendar.

Selecting a loan isn’t just about getting the lowest rate—it’s about partnering with a lender whose terms echo your business’s heartbeat.

Before you sign, sketch out upcoming project milestones and invoice dates. Ask yourself: will I have reliable weekly cash inflows, or is a monthly installment plan safer? This honest exercise guards against surprises down the road.

Common Red Flags To Watch For

Even experienced contractors can fall prey to clever lender tactics. Watch for these warning signs:

- Vague or Hidden Fees: If the lender skirts specifics on charges, proceed with caution.

- High-Pressure Sales Tactics: A credible provider gives you space to review and ask questions.

- Unrealistic Promises: Claims like “guaranteed approval” or “zero risk” often mask harsh terms.

A transparent lender will hand over clear paperwork, spell out every cost and invite your scrutiny. By investing time in this comparison phase, you’ll secure financing that supports your projects instead of steering them off course.

Accelerating Your Funding with a Financing Partner

Trying to secure a construction loan can feel like navigating an obstacle course blindfolded. You're dealing with slow banks, a confusing maze of financing products, and loan agreements that seem designed to be confusing. These hurdles don't just slow you down; they can mean losing out on big projects and hitting the brakes on your company's growth.

But what if you didn't have to go it alone? Imagine having an expert guide who knows the terrain inside and out. That's the real advantage of partnering with a dedicated financing expert like FSE - Funding Solution Experts.

Why a Partner Outperforms a Bank

A true financing partner is your advocate, not just another gatekeeper processing paperwork. Their entire business is built on speed, flexibility, and a deep understanding of the unique cash flow cycles that define the construction industry. While a traditional bank might drag its feet for months, a good partner can often get you an approval in hours and have cash in your account in a matter of days.

This completely changes the game, turning the lending process from a headache into a powerful tool for your business. Here’s how it works:

- Access to a Broad Lender Network: You're not stuck with one bank's rigid rules. Instead, you get access to a whole network of lenders, each with different appetites for risk and different specialties.

- Expert Guidance and Matching: A partner helps you pinpoint the exact right loan for your situation—whether for a new excavator, covering payroll, or kicking off a new build—and then connects you with the lender most likely to approve it.

- A Simplified Application Process: You fill out one simple application. Your partner then does the heavy lifting, presenting it to multiple lenders for you and saving you an enormous amount of time and energy.

A great financing partner does more than just find you money. They act as a strategic advisor, helping you weigh offers, understand the real cost of borrowing, and structure a deal that actually works with your project timelines and cash flow.

From Application to Funded in Days

The main objective is to get capital into your hands so you can get back to what you do best: building. This speed is what truly sets a financing partner apart. The process is designed from the ground up for efficiency, from the first conversation to the moment the funds hit your account.

At FSE, for example, we pair you with a dedicated advisor who takes the time to understand your business and your immediate goals. This person is your single point of contact, steering the entire process and making sure you get the best possible terms from our network of over 50 lending partners.

It's this relationship-driven approach that makes all the difference. By presenting your business professionally and transparently, we build a strong case that helps lenders see the opportunity, leading to a much smoother and faster approval.

If your construction business needs capital to jump on the next big opportunity, the right partner can change everything. Take the next step with FSE - Funding Solution Experts and secure the funding you need to grow.

Your Top Questions About Construction Loans, Answered

Even after reading through a detailed guide, you probably still have a few specific questions bouncing around. Let's tackle some of the most common ones I hear from construction business owners to give you that extra bit of clarity.

How Much Does My Personal Credit Score Really Matter?

This is a big one. For newer companies, your personal credit score carries a lot of weight. Lenders look at it as a reflection of your financial discipline. A solid score, usually something north of 680, can open doors to better rates and terms because it signals to them that you're a reliable borrower.

But what if your score isn't perfect? It's not necessarily a dead end. Many of the newer, alternative lenders are more interested in your business's vital signs—things like consistent cash flow, a healthy revenue history, and the value of your current contracts. If you can show steady monthly revenue, often $10,000 or more, you can absolutely find funding, even while you’re working on your personal credit.

Do I Always Have to Put Up Collateral?

Not at all. Whether or not you need collateral really comes down to the specific type of financing you're going after.

- Equipment Financing: This is a classic example where the collateral is built-in. The new dozer or excavator you're buying secures the loan itself.

- Secured Loans: For bigger loan amounts or for businesses still building their credit history, lenders might ask you to pledge an asset, like company real estate or other owned equipment.

- Unsecured Loans: Many options, like working capital loans or a business line of credit, are often unsecured. The lender's decision here is based purely on your business's financial health and credit profile.

At the end of the day, lenders are all about managing risk. The more you can prove your business has strong, reliable revenue and a track record of paying its bills, the less they'll need to ask for collateral to feel comfortable.

How Fast Can I Actually Get the Money?

The speed of funding is where you see the biggest difference between your options. If you walk into a traditional bank, be prepared to wait. Their approval process for a construction loan can easily take 60 to 90 days, a timeline that can completely derail a time-sensitive project.

This is where alternative lenders and financing partners completely change the game. They’re built for speed. Their applications are usually online and take just a few minutes to fill out. It's not uncommon to get an approval decision in 24 hours and see the cash hit your bank account within 24 to 48 hours after that.

What if a Bank Has Already Turned Me Down?

Getting a "no" from a bank feels like a major setback, but it’s rarely the final word. Banks operate with very strict, often outdated, underwriting rules and are notoriously cautious about industries like construction, which they see as high-risk.

Alternative lenders and specialized brokers, on the other hand, thrive in these exact scenarios. They look at the bigger picture of your business's health and potential. Your recent cash flow, signed contracts, and monthly revenue statements often mean more to them than a single FICO score. Think of a bank denial less as a failure and more as a sign that you just need a financing partner who actually understands your industry.

Don't let a slow "no" from a bank put the brakes on your next big project. FSE - Funding Solution Experts focuses on matching construction businesses with fast, flexible funding from a network of over 50 lenders. Get the capital you need to build and grow your business today.