Let's be honest, the heavy equipment needed to run a successful construction business is expensive. A single new dozer or excavator can easily demand a six-figure investment, a cash outlay that could cripple even a well-established company. This is precisely where construction machinery finance comes in—it’s the financial tool that allows you to get the iron you need on the job site without draining your bank account.

Put simply, it's a way to acquire essential machinery by breaking down a massive one-time cost into a series of predictable, manageable payments. This lets you hold onto your cash for other critical parts of the business, like payroll, materials, and bidding on new projects.

The Foundation of Construction Business Growth

It’s best to think of machinery finance as a strategic move for growth, not just another loan. In this industry, having the right equipment is non-negotiable. The biggest roadblock for many contractors isn't finding work; it's affording the high-powered machinery needed to get the work done. A new mid-size bulldozer, for instance, can cost $500,000 or more—an expense that could wipe out a company's capital reserves in a single transaction.

This is why financing is such a game-changer. Instead of locking up your capital in a depreciating asset, you can get that machine working and earning revenue for you through manageable monthly installments. It's really no different than getting a mortgage for a property; you get to use a high-value asset immediately while paying for it over its useful life. This mental shift from seeing equipment as a huge upfront cost to a regular operating expense is what unlocks real growth.

Why Financing Is a Smarter Strategy

Opting for construction machinery finance is about more than just managing cash flow; it’s about creating new opportunities. When you preserve your working capital, you gain the financial agility to run your business better. That freed-up cash can be put to work on other things that directly boost your profitability.

Here are a few of the biggest advantages:

- Winning Bigger Contracts: Having the latest, most capable equipment means you can confidently bid on larger, more lucrative projects that might have been out of your league before.

- Improving Operational Efficiency: Modern machinery is more reliable and fuel-efficient. Upgrading from older equipment means less downtime for repairs and lower operating costs, which goes straight to your bottom line.

- Maintaining Healthy Cash Flow: A fixed monthly payment is easy to budget around. This protects your cash reserves for the unpredictable nature of the business—covering payroll, buying materials, and handling unexpected expenses without stress.

When you finance, you're not just buying steel; you're investing in your company's earning potential. The equipment starts generating revenue right away, often making the financing payment a self-liquidating part of your growth plan.

At the end of the day, financing is the bridge between the equipment your business needs and the capital you have on hand. It allows your construction company to scale up, compete more effectively, and jump on growth opportunities without taking on unnecessary financial strain. It makes your machinery an asset that works for you from day one, not a liability that drains your resources.

Exploring Your Financing Options

Once you’ve decided financing is the right move, the next big question is: which kind? Think of it like picking a tool from the truck. You wouldn't use a sledgehammer for a delicate job, and the best financing option hinges entirely on your business goals, your cash flow situation, and your long-term plans for the equipment.

The world of equipment finance has grown right alongside the construction industry itself. In just one year, the global market jumped from $59.01 billion to $63.63 billion, and it's on track to hit nearly $89.78 billion in the next five years. You can see more details on this growth at GII Research, but the bottom line for you is simple: more options and more competitive deals.

Let's walk through the most common ways to fund your next big purchase.

Term Loans: The Traditional Path to Ownership

When most people hear "financing," a term loan is what comes to mind. It's the classic model: a lender gives you a lump sum of cash to buy a piece of machinery, and you pay it back in fixed monthly installments, plus interest, over a set period. Simple and straightforward.

This is the go-to choice for businesses that want to own their equipment outright and build equity over time. If you plan to run that dozer or excavator for its entire useful life, a term loan is probably your best bet.

- Best For: Established businesses with predictable cash flow who see the equipment as a long-term asset for their balance sheet.

- Ownership: It's yours from day one. The lender just holds a lien on the machine—much like a mortgage on a house—until you've made the final payment.

- What to Expect: Term loans usually require a down payment and have stricter credit standards. The trade-off? You can often lock in excellent interest rates and get significant tax advantages by depreciating the asset.

Equipment Leases: Lower Payments and Greater Flexibility

Think of an equipment lease as a long-term rental. Instead of borrowing money to buy the machine, you're paying a leasing company a monthly fee to use it for a specific timeframe. This is a game-changer for companies focused on managing monthly expenses and staying nimble.

Leases typically fall into two buckets: operating and capital. An operating lease is a pure rental; you get lower payments and simply return the equipment when the term is up. A capital lease acts more like a loan, often ending with a buyout option that lets you take ownership.

Key Insight: Leasing is a brilliant strategy for technology-driven equipment like GPS-enabled graders or advanced surveying drones that become outdated fast. It lets you cycle into new models every few years without getting stuck with obsolete iron.

By leasing, you're only paying for the machine's depreciation during the time you use it, not its total cost. That's why the monthly payments are almost always lower than a loan payment for the same piece of equipment.

Equipment Finance Agreements: A Hybrid Approach

An Equipment Finance Agreement, or EFA, neatly blends the features of a loan and a lease. Like a loan, it’s a contract designed for you to purchase equipment over time. But its structure is often much simpler and more direct.

With an EFA, the agreement lays out the total cost, the exact number of payments, and what each payment will be. There's no separate interest rate to calculate; it's a clear, straightforward installment plan to ownership.

- Best For: Businesses that want a simple, transparent path to owning their equipment without the formal hoops of a traditional bank loan.

- Ownership: You get the title and become the full owner as soon as you make that last payment.

- Typical Speed: EFAs are built for speed. They're usually offered by specialized financiers who understand the industry, so the approval and funding process can be dramatically faster than a conventional loan.

A Quick Comparison to Guide Your Choice

Sometimes seeing the options side-by-side makes the decision clearer. Here’s a quick-glance table to help you match the financing type to your company's immediate needs.

Comparing Construction Machinery Finance Options

| Financing Type | Best For | Ownership | Typical Speed |

|---|---|---|---|

| Term Loan | Long-term asset ownership, building equity, stable businesses. | Immediate ownership with a lender's lien. | Moderate (1-4 weeks) |

| Equipment Lease | Lower monthly payments, frequent equipment upgrades, preserving cash flow. | Leasing company owns it; you have an option to buy. | Fast (2-7 days) |

| Equipment Finance Agreement (EFA) | A simple, fast path to ownership with clear payment terms. | You own it after the final payment. | Very Fast (1-5 days) |

| Chattel Mortgage | Businesses in specific regions (like Australia) seeking tax benefits. | Immediate ownership with a lender's lien. | Moderate (1-3 weeks) |

This table is a starting point. The best choice always comes down to the specifics of your operation, your financial health, and what you want to achieve with the new equipment.

Other Powerful Financing Tools

Beyond these core three, a few other tools can be incredibly useful for your business.

- SBA Loans: Backed by the Small Business Administration, these loans can offer fantastic rates and long repayment terms. The catch? They are very competitive, and the application process is notoriously detailed and can take a while.

- Business Lines of Credit: This gives you a revolving credit line you can tap into as needed. It's not for a single big purchase but is perfect for covering unexpected repairs, short-term rentals, or even making a down payment on a larger financing deal. It’s all about flexibility.

- Dealer/In-House Financing: Many equipment dealers offer their own financing at the point of sale. It's incredibly convenient, and you can sometimes find 0% financing deals on new machinery. Always read the fine print, but don't overlook this option.

- Merchant Cash Advance (MCA): An MCA provides a lump sum of cash in exchange for a percentage of your future sales. It's very fast but is also one of the most expensive forms of financing. It should only be considered for urgent, short-term needs when other options aren't available.

Ultimately, choosing the right type of construction machinery finance is a strategic business decision. By matching the financing structure to your goals—whether that's long-term ownership, low monthly payments, or sheer speed—you can turn that next equipment purchase into a powerful engine for growth.

How Lenders Evaluate Your Application

When you're ready to finance a new piece of construction machinery, it’s helpful to see things from the lender’s point of view. They’re essentially trying to answer one big question: "Is this a good investment for us?" They’re not just looking at a single number on a form; they're piecing together a complete picture of your company's financial health to gauge your ability to handle the new debt.

Think of it as a risk assessment. Lenders need to be confident that you can, and will, make your payments on time. To get there, they dig into your business performance, your credit history, and even the specs of the machine you want to buy.

Your Business Financials Under the Microscope

First and foremost, lenders want to see a stable, healthy business. A track record of consistent revenue is the best indicator that you can manage a new loan or lease payment without breaking a sweat.

While every lender has its own specific criteria, they almost always focus on three core factors:

- Time in Business: How long have you been operating? Lenders feel much more comfortable with established companies. A business that's been around for at least two years is seen as a much safer bet than a startup still finding its footing.

- Annual Revenue: Your top-line numbers show your capacity to take on new payments. Strong, predictable revenue tells a lender that you have the cash flow to handle the financing comfortably.

- Credit History: This one is a biggie. Lenders will pull both your business and personal credit scores. A clean report showing a history of paying your bills on time is a powerful signal that you’re a responsible borrower.

The Role of the Equipment Itself

Your business profile is only half the story. The specific piece of machinery you're financing is also a critical part of the lender's calculation. Why? Because that equipment serves as collateral.

If, for some reason, you were to default on the payments, the lender’s backup plan is to repossess and sell the asset to get their money back.

Naturally, this means the age, condition, and type of the equipment are incredibly important. A newer excavator from a top-tier brand will hold its value far better than an older, obscure piece of equipment, making it much lower risk for the lender. This focus on quality collateral is a major reason why term loans hold a dominant 34.7% share of the global market, as contractors finance high-tech, efficient machinery. Earthmoving equipment alone is projected to represent a financing market of $56.29 billion by 2032. You can discover more about these market trends in construction equipment finance.

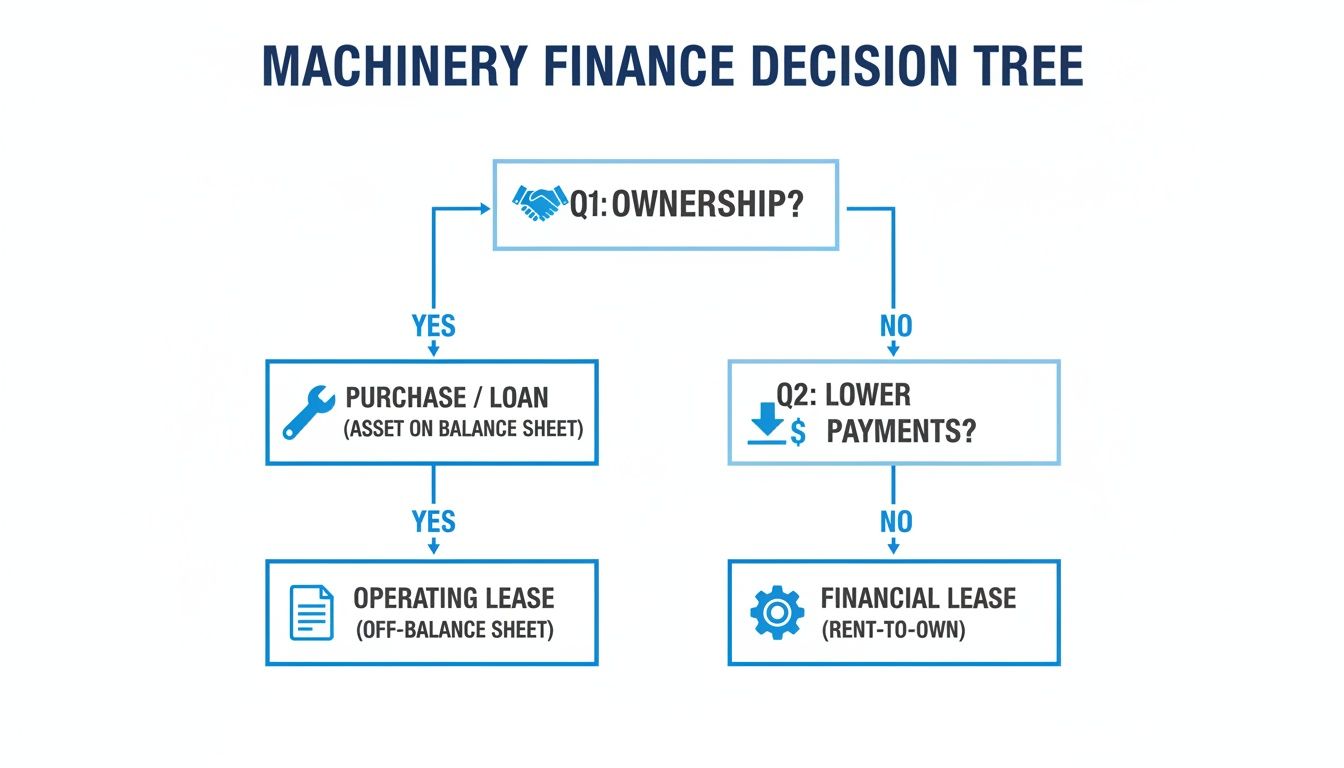

This decision tree can help you map your business priorities—like owning the asset versus keeping monthly payments low—to the right financing product.

It’s a simple visual guide that quickly shows how your primary goal, whether it’s building equity or preserving cash, points you toward a specific path.

Key Takeaway: A strong application tells a clear story. It shows a stable business with a proven track record, good credit habits, and a sensible plan to acquire a valuable, revenue-generating asset.

Now, if your business doesn't check every single box on a traditional bank’s list, don't sweat it. That’s where working with a broad funding network comes in handy. Many alternative lenders specialize in the construction industry. They understand the seasonal ups and downs and are often more flexible with businesses that have minor credit dings or a shorter operating history.

Your Step-By-Step Guide to Getting Funded

Getting financing for new construction machinery might sound like a headache, but it’s a lot more straightforward than you might think. Forget the old days of endless paperwork and weeks of waiting on a bank. Today's process is fast, efficient, and broken down into a few simple stages.

The whole point is to get that new piece of revenue-generating iron on your job site without the runaround. Let's walk through what that actually looks like, from the first click to the final handshake.

Stage 1: The Quick Application

This first step is usually the easiest. Most modern lenders and financing partners have a simple online form that takes just a few minutes. You’ll plug in the basics: company name, how long you've been in business, a rough idea of your annual revenue, and what kind of equipment you're looking to buy.

Think of it as the initial conversation—a quick, no-pressure way for the finance provider to get a feel for your business. Based on this snapshot, they can instantly get an idea of which financing programs are the best fit, saving everyone a ton of time right out of the gate.

Stage 2: Gathering Your Documents

Next, you'll need to provide a few documents to back up the info from your application. This part can sound like a drag, but it's usually just a handful of standard items you can pull together quickly. Being ready here is the single best way to fly through the approval process.

Here’s what you’ll typically need:

- Bank Statements: Most lenders want to see the last three to six months of your business bank statements to confirm your cash flow is steady.

- Equipment Quote: You'll need an official quote or invoice from the seller for the specific machine you want. This locks in the asset's value.

- Driver's License: A simple copy of your driver's license to verify your identity.

- Business Registration: Documents like your articles of incorporation that prove your company is a legitimate, registered entity.

Having these files on hand before you even start can turn a multi-day process into a same-day approval.

By having your documents ready to go, a good funding partner can often get you a preliminary approval within 24 hours. That's a world away from traditional bank loans, which can easily drag on for weeks or even months.

Stage 3: Comparing the Offers on the Table

This is where working with a financing marketplace or broker really pays off. Instead of you filling out application after application for different lenders, your one application gets shopped around to a whole network of them. This makes lenders compete for your business, which almost always means you get a better deal.

Your funding advisor then lays out the best offers for you, side-by-side. They'll walk you through the differences in rates, the length of the terms, and how the payments are structured. They're in your corner, helping you weigh the pros and cons so you can confidently choose the construction machinery finance option that truly works for your company's cash flow and growth plans.

Stage 4: Closing the Deal and Getting Your Equipment

Once you’ve picked the winning offer and signed the agreements, it’s go-time. The lender sends the funds directly to the equipment dealer, and you arrange to get your new machine delivered to your yard or job site. From signing the final papers to the money being wired, this last step often happens within 24 to 48 hours.

This kind of speed is a direct result of a booming market. The global construction equipment finance market is already worth over USD 94 billion and is on track to blow past USD 157 billion in the next decade. You can read the full research on construction equipment finance trends to see why this growth is creating better, faster options for contractors.

Ultimately, this clear, step-by-step process is designed to get you the capital you need without the frustrating delays, so you can put that new equipment to work and start making money with it right away.

Common Mistakes To Avoid When Financing Equipment

Getting the right financing for your equipment can feel like a huge win, but the road is paved with potential mistakes that can cost you serious money and tie your hands down the line. It's easy to get lost in the fine print, so knowing what to watch out for before you sign on the dotted line is key. This ensures your financing deal is a springboard for growth, not a financial anchor.

The biggest trap? Only looking at the monthly payment. A low payment might look great on the surface, but it can easily hide a much higher total cost stretched over a longer term or mask some really restrictive conditions. You might feel like you're saving a few bucks each month, but you could end up paying thousands more over the life of the loan.

Overlooking Prepayment Penalties

Picture this: your business lands a massive contract, and you've got extra cash. You decide to be smart and pay off your equipment loan early to stop the interest from racking up. But then you get hit with a nasty surprise—a prepayment penalty. This is a fee lenders charge when you pay off the loan ahead of schedule because it cuts into their expected profit.

Before signing anything, ask your financing advisor directly if the agreement includes these penalties. A contract without them gives you the freedom to manage your debt on your own terms, which is a massive advantage.

Confusing Interest Rate with APR

Here’s another common mix-up: treating the interest rate and the Annual Percentage Rate (APR) as the same thing. They aren't. The interest rate is just the base cost of borrowing money. The APR, on the other hand, tells the whole story.

The APR combines the interest rate with all the other lender fees—like origination fees or closing costs—that get rolled into the loan. It's the true, all-in cost of borrowing.

When you're comparing offers from different lenders, always use the APR. It’s the only way to make a true apples-to-apples comparison and see which deal is actually better for your bottom line.

Not Preparing Your Documentation

Showing up to a meeting with a lender without your paperwork in order is a bad look. Lenders want to see that you're an organized and serious business owner. If you’re scrambling to find bank statements or chase down an equipment quote, it doesn't just slow things down; it can make a lender think twice about your application.

Get ahead of the game by having these documents ready to go:

- Recent Business Bank Statements: Most lenders will want to see the last three to six months.

- Official Equipment Quote: A proper, detailed invoice from the seller.

- Business Registration Documents: Proof that your company is legitimate.

- Valid Identification: A clear copy of your driver’s license will do.

Having everything prepared shows you mean business and makes the approval process a whole lot smoother. It instantly puts you in a better position, giving you more leverage to negotiate a great deal. Sidestepping these common blunders will help you secure construction machinery finance that truly works for you, protecting your cash flow and setting you up for long-term success.

How We Make Your Financing Journey Simple

Trying to finance heavy equipment can feel like hitting a wall. You know you need that new excavator or dozer to take on bigger jobs, but the process of actually getting the money can be a major roadblock.

Between the slow-moving banks, the confusing jargon from lenders, and the frustration of a sudden rejection, it’s easy to feel like your growth plans are stuck in the mud.

That's exactly where we come in. At FSE - Funding Solution Experts, we trade the confusion and delays for a clear, direct path forward. We know that in construction, waiting around isn't an option. When a lucrative contract is on the line, you can’t afford to spend weeks hoping for a bank to say "yes."

Our entire approach is built for speed and simplicity, giving you a serious competitive edge.

Your Direct Path to Over 50 Lenders

Forget spending days filling out separate applications and chasing down individual banks. We flip the script and bring the lenders directly to you.

With one straightforward application, we tap you into our network of over 50 specialized lending partners. These aren’t your typical high-street banks with their rigid, cookie-cutter rules. They’re funders who actually get the ins and outs of the construction industry and its unique cash flow cycles.

This model naturally creates competition for your business, which means you get the best rates and terms available. We do all the legwork, matching your specific needs with the right lender and financing product, which saves you a massive amount of time and hassle.

You’re not just another application in a pile. We connect you with a dedicated funding advisor—a real person who knows this industry—to walk you through everything, from comparing your offers to signing the final papers.

From Application to Action in 48 Hours

Our job is to help you slice through the red tape that ties up so many business owners. We’ve designed a process with one goal in mind: get the cash you need, so you can get the equipment on-site and earning its keep.

- Fast Approvals: You’ll often see preliminary decisions within 24 hours.

- Flexible Terms: We work to find financing that aligns with your business's cash flow, not the other way around.

- Expert Guidance: Your advisor will break everything down in plain English, so you can feel 100% confident in your decision.

If you need fast, no-nonsense construction machinery finance to jump on your next big opportunity, we're here to make it happen.

Ready to see what's possible? Start your no-obligation application today or schedule a call to talk through your equipment needs with an expert.

Frequently Asked Questions

When you're ready to get serious about financing equipment, a few practical questions always come up. Here are some straight answers to the things we hear most often from construction pros, clearing up the final details so you can move forward with confidence.

Can I Finance Used Construction Equipment?

Yes, absolutely. Financing used machinery isn't just possible; it's a smart and very common way to build your fleet. Lenders know that a well-maintained piece of equipment from a major brand like Caterpillar or John Deere holds its value and can be a workhorse for your business for years to come.

The process is nearly identical to financing new gear. The lender will look at the machine's age, hours, and overall condition, but a solid piece of pre-owned iron is a great asset to finance.

What Kind of Credit Score Do I Need?

There’s no single magic number, but a good rule of thumb is that a personal credit score of 600 or higher puts you in a strong position for most financing programs. Lenders who specialize in the construction world are often more flexible than traditional banks.

They’re looking at your whole business, not just one score. If you have solid, consistent revenue and have been in business for at least a year, that can often make up for a less-than-perfect credit history. Don't count yourself out before you even apply.

Expert Tip: A strong application tells a story. Lenders get excited about businesses with healthy cash flow, a good backlog of projects, and a clear plan for how the new equipment will make them money. That often matters more than a FICO score alone.

How Fast Can I Actually Get the Money?

This is where equipment financing really shines compared to old-school bank loans. Forget waiting weeks or months. Once you submit a straightforward application and the basic documents, you can often have a decision in your hands within 24 hours.

After you pick an offer and sign the documents, the funds are wired directly to the seller, usually within another 24 to 48 hours. That means you can go from application to having that new machine on a job site in just a few days.

What Happens at the End of My Equipment Lease?

When your lease term is up, you've got options. This flexibility is one of the biggest perks of leasing. Your choices usually boil down to one of these four paths:

- Buy it: Purchase the equipment for a set price agreed upon at the start of the lease.

- Walk away: Simply return the equipment to the leasing company and your obligation is done.

- Renew the lease: Keep using the machine, often with a new, lower monthly payment.

- Trade up: Start a new lease and upgrade to a newer, more advanced model.

At FSE - Funding Solution Experts, our job is to cut through the complexity. We connect you to the right lenders who understand your business, helping you get the capital you need without the runaround. See your financing options today.