If you're juggling multiple business payments every month, you know how chaotic it can get. You’re definitely not alone. Debt consolidation for small business is a financial strategy designed to solve exactly this problem by rolling several debts into one single, manageable loan. It’s a smart, proactive move that can free up your cash flow and get you back to focusing on growth.

Why Smart Businesses Consolidate Their Debt

Think about all your current business debts for a moment. You might have vendor invoices, an equipment loan, a few credit card balances, and maybe a merchant cash advance from a slow month. Each one has its own due date, interest rate, and terms. It's a logistical nightmare that eats up your time and mental energy.

Debt consolidation cuts through that chaos. It streamlines everything into one predictable monthly payment. This isn’t just a survival tactic; it’s about reclaiming control. Instead of juggling a half-dozen payment reminders, you have one. That simplicity alone is a huge weight off your shoulders, letting you focus on what you do best—running your business.

Unlocking Financial Flexibility

Beyond making your life easier, the real power of consolidation lies in improving your financial standing. By replacing a handful of high-interest debts with a single loan, the goal is to secure a lower overall interest rate. This often translates into a lower total monthly payment, which directly boosts your most vital asset: your cash flow.

Healthy cash flow is the lifeblood of a small business. With more cash on hand, you can:

- Meet payroll without scrambling.

- Invest in new inventory to keep up with demand.

- Fund marketing campaigns to land new customers.

- Build a cash reserve for unexpected repairs or exciting opportunities.

Overcoming Modern Debt Hurdles

Managing debt smartly has never been more important. Small business debt is at an all-time high, with almost 40% of small businesses now carrying balances over $100,000. The Federal Reserve's Small Business Credit Survey paints a clear picture: this debt load is a major obstacle. In fact, 41% of businesses that were denied financing were told it was because they already had too much debt. A Bankrate analysis dives deeper into these statistics.

This is where strategic debt consolidation for a small business becomes so powerful. It’s not just about managing what you owe today; it’s about cleaning up your balance sheet to qualify for the funding you’ll need tomorrow.

By organizing your liabilities into one structured loan, you send a clear signal to lenders that you are a disciplined, proactive business owner. It shows you’re serious about your company's financial health, making you a much stronger candidate for the capital needed to expand, innovate, and thrive.

Choosing Your Debt Consolidation Pathway

Okay, you've decided that debt consolidation for your small business makes sense. Now comes the critical part: picking the right road to get there. There isn't a one-size-fits-all solution. Each method has its own strengths and is designed for different business situations.

Think of it like choosing a vehicle. You wouldn't use a sports car to haul lumber, and you wouldn't use a semi-truck for a quick trip to the store. The best choice depends entirely on your company's financial health, credit history, and where you want to go in the long run. Let's break down the most common routes.

Traditional Bank and Credit Union Term Loans

For a business with a solid track record and great credit, a term loan from a traditional bank or credit union is often the best-case scenario. It's clean and simple: you get a single lump-sum loan, use it to wipe out your other debts, and then make one predictable monthly payment over a set period.

This is the most direct route. It’s perfect for businesses that need to consolidate a specific pile of debt once and for all and prefer the stability of a fixed interest rate.

The catch? The bar for approval is high. Lenders will want to see:

- Excellent personal and business credit scores, usually 680 or higher.

- A proven history of profitability, often for several years.

- A full suite of financial documents, like tax returns, balance sheets, and P&L statements.

Government-Backed SBA Loans

What if your business is healthy but you don't quite tick all the boxes for a conventional bank loan? That's where SBA loans come in. These loans aren't directly from the government; instead, the Small Business Administration guarantees a portion of the loan, making lenders more willing to say "yes."

This government backing often translates into fantastic terms—lower interest rates and much longer repayment periods. Think 10 years for working capital or even up to 25 years for real estate. That extended timeline can slash your monthly payment, freeing up a massive amount of cash flow.

SBA loans are a huge part of the small business economy. In a single recent fiscal year, the program backed over 70,000 loans worth $31.1 billion, marking a 13% jump in funding. The trend continued, with the first quarter of the next year seeing an $8.73 billion lending volume—a 38% increase over the previous Q1. You can find more details in these small business lending statistics.

Flexible Business Lines of Credit

A business line of credit (LOC) is less about a one-time fix and more about ongoing financial agility. Instead of a single loan, you get a revolving credit limit you can tap into whenever you need it. You only pay interest on the funds you actually use.

This option is like having a financial safety net. It’s best for businesses with fluctuating cash flow who need to pay off smaller debts over time while also covering unforeseen expenses without having to apply for a new loan each time.

Imagine a landscaping company. They could use an LOC to pay off high-interest credit cards used for equipment, while also having a reserve to cover payroll during a slow winter month.

Specialized MCA Consolidation Solutions

Merchant Cash Advances (MCAs) can be a lifeline in a pinch, but their daily or weekly repayment schedules can absolutely crush a business's cash flow. If you're juggling multiple MCAs, a specialized MCA consolidation program (sometimes called a reverse consolidation) can offer a way out.

Here’s how it works: instead of a loan that pays off the MCAs, this service deposits cash into your account on a regular schedule to help you meet those aggressive MCA payments. You then make a single, more manageable payment to the consolidation company. It doesn't erase the MCA debt, but it stops the daily bleeding from your bank account.

This is a strategic play for businesses caught in the MCA debt cycle. The immediate goal is to stabilize your cash flow and give you the breathing room needed to get back on solid ground.

Comparing Small Business Debt Consolidation Methods

To make the choice clearer, we've broken down the key features of each option. This table should help you quickly see which path might be the best fit for your business's current situation.

| Consolidation Method | Best For | Typical Interest Rate | Common Repayment Term | Key Advantage |

|---|---|---|---|---|

| Bank Term Loan | Businesses with strong credit and financials | Low to Moderate | 2-7 years | Predictable payments and low rates |

| SBA Loan | Healthy businesses that don't meet strict bank criteria | Low (Prime + Spread) | 7-25 years | Very long terms and competitive rates |

| Business Line of Credit | Managing ongoing cash flow and smaller debts | Moderate | Revolving | Flexibility to draw and repay as needed |

| MCA Consolidation | Businesses with multiple, high-cost MCAs | Varies (Factor Rate) | 6-18 months | Stabilizes cash flow from daily payments |

Ultimately, the right choice depends on a careful analysis of your debts, your business's performance, and your long-term goals. Each of these methods offers a valid way forward, but only one will be the perfect fit for your journey.

What It Really Takes to Qualify (and What It'll Really Cost)

Getting a lender to say "yes" to a consolidation loan isn't just about filling out a form. They're trying to build a complete picture of your business's health, and your application is the only information they have.

Think of them as a very cautious investor. They need to see a stable, reliable operation that can comfortably handle a new, single payment. Your credit score is part of that story, but so are your sales figures, your time in business, and the consistency of your cash flow.

What Lenders Are Actually Looking For

While every lender has their own secret sauce for approvals, a few key ingredients are always on the list. Before you even start an application, you need an honest assessment of where you stand on these core metrics.

Here’s what they’ll be digging into:

- Credit Scores: Expect them to pull both your personal and business credit. For many small businesses, your personal score carries a lot of weight, and a score of 680+ often opens the most doors. Your business credit history shows them how you’ve handled vendor and trade accounts in the past.

- Time in Business: Lenders get nervous about brand-new businesses. They typically want to see at least one to two years of operational history. This track record proves your business model isn't just a flash in the pan and that you've navigated the initial startup hurdles.

- Revenue: This is the big one. Consistent revenue proves you have the means to repay the loan. Many lenders set a floor, often looking for a minimum of $10,000+ in monthly revenue, to ensure you can cover your operating expenses and the new loan payment without strain.

At the end of the day, lenders are just managing risk. They're looking for a predictable financial pulse. Consistent cash flow is the single best indicator that your business can successfully manage a consolidated payment schedule.

Looking Past the Interest Rate: The Hidden Costs

The interest rate is what gets all the attention, but it’s rarely the full story. The true cost of your loan is often buried in the fine print, and overlooking these details is where many business owners get into trouble.

A loan with a temptingly low interest rate can easily become more expensive than a higher-rate option once you factor in all the fees. This is why you must focus on the Annual Percentage Rate (APR). The APR gives you a much more accurate, all-in picture by bundling the interest rate with most of the associated fees.

Uncovering the Fine Print

To really understand what you're signing up for, you have to play detective and investigate every line item. Knowing what to look for will save you from nasty surprises down the road and help you compare offers on an apples-to-apples basis.

Be sure to ask about these specific costs:

- Origination Fees: This is the lender’s fee for processing your application and funding the loan. It's almost always a percentage of the total loan amount—typically 1-5%—and is often taken directly out of the funds you receive.

- Closing Costs: Just like a mortgage, some business loans have a bundle of fees for things like appraisals, background checks, and legal paperwork. Insist on getting a detailed breakdown so you know exactly what you're paying for.

- Prepayment Penalties: This one can really sting. Some lenders charge a fee if you try to pay off your loan ahead of schedule. They do this to make up for the interest they'll lose. If there’s any chance you’ll want to clear the debt early, you need to know if this penalty exists.

By getting a firm handle on both the qualification standards and the complete cost structure, you can approach the small business debt consolidation process from a position of strength. This knowledge helps you put together a winning application and, more importantly, choose a loan that genuinely helps your business without saddling it with unexpected expenses.

Deciding If Consolidation Is Your Best Move

Debt consolidation can be a fantastic move for a business, but it's not a magic fix for every financial headache. Before you jump in, you need to take a hard, honest look at your company's finances, where you're headed, and the specific debts you're carrying. This isn't just about shuffling payments around; it's about choosing a path that makes your business stronger for the long haul.

The first step is to get to the "why." What's driving you to even consider this? Are you buried under a mountain of different payment due dates? Are high interest rates slowly bleeding your cash flow dry? Or is it the unpredictable payment schedule that’s making it impossible to forecast your cash? Nailing down the root cause helps you see if consolidation is the right strategic play or just a temporary band-aid.

Green Lights for Consolidation

Some situations practically scream for consolidation. If any of these sound familiar, it's a strong sign that you should seriously explore your options for debt consolidation for your small business.

- You're Juggling Multiple High-Interest Debts: This is the classic scenario. If you’re paying off several merchant cash advances, short-term loans, or high-APR business credit cards, rolling them into one loan with a single, lower average interest rate can save you a ton of money and simplify your life.

- Your Monthly Payments Are All Over the Place: Debts with variable rates or daily payment structures, like MCAs, can create a cash flow nightmare. A fixed-rate consolidation loan gives you one predictable, stable monthly payment, which makes budgeting infinitely easier.

- You Need to Improve Your Credit Profile: Successfully managing a single, structured loan is a great way to show credit bureaus you’re financially responsible. Making those on-time payments consistently will, over time, help boost your business credit score and open up better funding options down the road.

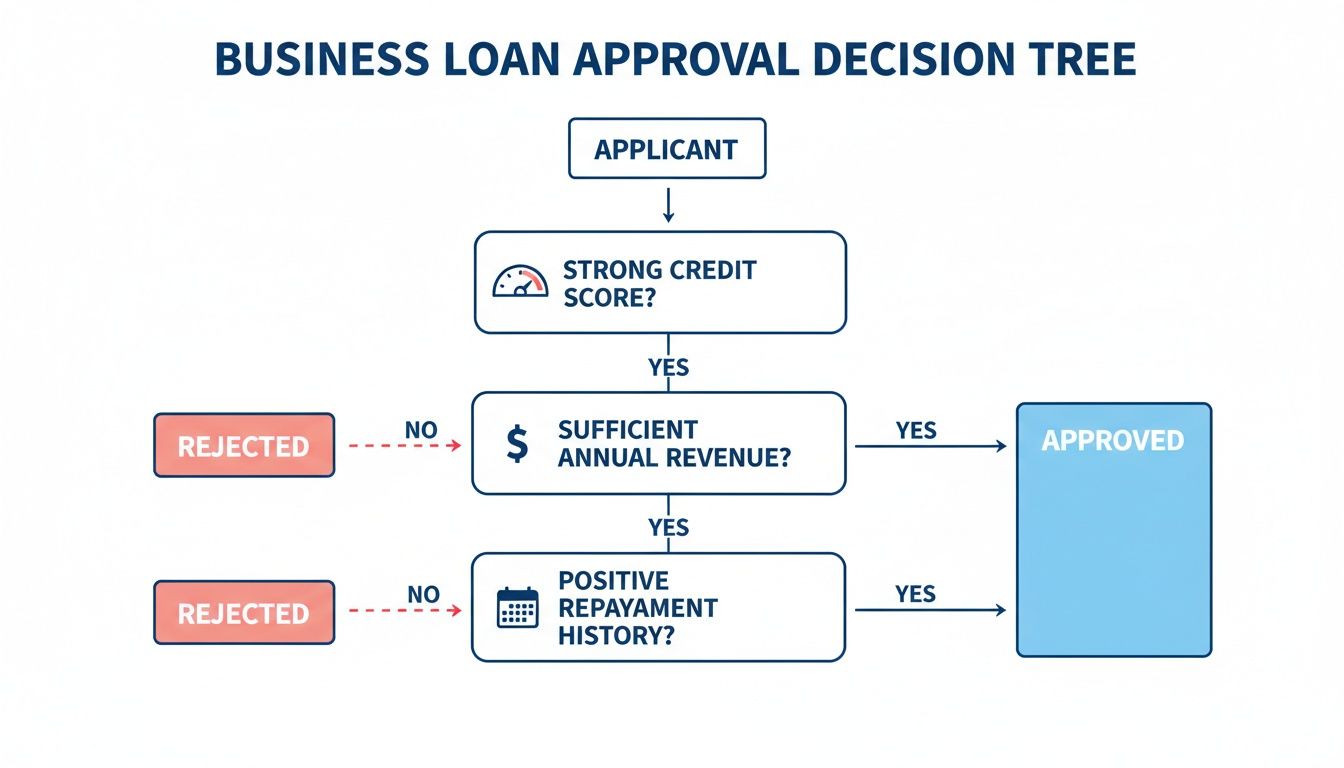

This chart gives you a simplified look at how lenders see your business when making a loan decision.

As you can see, lenders are looking at a mix of factors—your credit, revenue, and business history—to figure out if you're a good candidate for financing.

When to Consider Alternatives

On the flip side, there are times when consolidation just isn't the right answer. Rushing into a new loan without weighing the drawbacks can sometimes create more problems than it solves.

It's crucial to weigh the benefits of a new loan against the terms of your existing debt. Sometimes, the smartest move is to focus on other strategies that fix the root cause of your financial strain without taking on a new loan.

For instance, if most of your debt is already locked in at a low, fixed interest rate, consolidating probably won't save you much money and could even end up costing you more. Or, if your business is struggling with a core profitability problem, another loan won't fix that—you need to focus on improving your operations first.

In these cases, you might want to explore:

- Targeted Debt Negotiation: Pick up the phone and call your individual creditors. You might be surprised what you can work out, whether it's better terms, a temporary payment reduction, or even a settlement.

- Strategic Debt Payoff: Use a disciplined approach like the "snowball" (paying off smallest debts first) or "avalanche" (paying off highest-interest debts first) method to knock out your obligations one by one.

- Securing New Working Capital: If you're just facing a temporary cash crunch for a specific project, a targeted working capital loan might make more sense than reorganizing all of your existing debt.

This kind of thoughtful analysis ensures you’re choosing a path that actually moves your business forward.

It's also important to understand the current lending climate. Small businesses are caught in an "access-to-capital gap" as traditional banks continue to tighten their lending standards. In fact, for 13 consecutive quarters, banks have made it harder to get a loan, demanding more collateral and offering shorter repayment terms. This reality makes debt consolidation for small business an even more valuable tool, often allowing you to lock in better terms than what the big banks are willing to offer right now. You can get a deeper dive into these small business lending trends to see the full picture.

How to Prepare a Winning Application

A strong application does more than just list numbers on a page; it tells the story of your business's future. Lenders aren't just looking at data—they're looking for organized, proactive owners who have a clear plan to win. If you get your documents and your narrative in order ahead of time, you dramatically increase your odds of getting approved.

Think of it as building a business case for your own success. This preparation shows lenders you’re a reliable partner and that a debt consolidation for small business loan is the key to putting your company on much stronger financial ground.

Step 1: Assemble Your Financial Toolkit

Before you even think about filling out a form, get all your paperwork together. Having everything ready to go from the start shows you’re a professional and makes the entire underwriting process smoother and faster. Trust me, a lender who has to constantly chase you for missing information is not going to be your biggest fan.

Here's the essential checklist of what you'll need:

- Recent Bank Statements: Pull at least three to six months of your business bank statements. Lenders need to see consistent revenue and healthy cash flow.

- Business Tax Returns: You'll typically need the last two years of filed returns to verify your income and prove your profitability.

- Existing Debt Information: Make a detailed list of every debt you want to consolidate. Include the lender's name, the current balance, the interest rate, and the monthly payment for each one.

Step 2: Review Your Credit and Write Your Story

Your credit reports play a huge role in any lending decision. Make sure you pull both your personal and business credit reports to check for any errors or surprises. Knowing your scores upfront gives you a realistic idea of what kind of loan terms you can actually expect.

This is also where you need to craft your narrative. Write a short, clear summary explaining why you need to consolidate and—this is the important part—how it will improve your business. Will it free up cash flow to fund a new project? Will it finally stabilize your monthly budget? Be specific.

A clear, positive narrative can be the deciding factor. It transforms your application from a simple request for money into a strategic plan for growth that a lender can confidently get behind.

Step 3: Create a Clean and Organized Submission

How you present your documents really matters. Scan everything and save them as clean, easy-to-read PDF files with logical names (e.g., "Company_Name_Tax_Return_2023.pdf"). When you finally submit your application, you want the lender to see a perfectly organized package.

It might seem like a small thing, but it reinforces the story you're telling. An organized application suggests an organized business, and that’s exactly the kind of company lenders want to work with. Following these steps shows you're a serious owner ready to move forward.

Let Us Handle the Search for You

Trying to find the right debt consolidation loan for your small business can feel like a second job you never wanted. Instead of spending your precious time hunting down lenders and filling out endless applications, what if you had an expert to do all the heavy lifting for you?

That’s exactly what working with Funding Solution Experts (FSE) is like. Our entire process is designed to turn a complicated, often stressful search into a straightforward, efficient experience. You fill out one simple application, and we immediately put our network of over 50 specialized lenders to work for you.

Your Guide Through the Funding Maze

Think of your FSE advisor as your personal guide in the financing world. Their sole focus is to dig through all the available options, bring you only the best offers, and then walk you through the fine print in plain English. This partnership means you'll understand every detail with complete clarity before making a commitment.

We help you cut through the noise and compare the factors that truly matter:

- Interest Rates and APR: What's the real, all-in cost of the loan?

- Repayment Terms: Does the payment schedule actually fit your company's cash flow?

- Loan Covenants: Are there any hidden restrictions or conditions you need to know about?

Our team has a knack for finding opportunities for businesses that don't fit into the perfect little box that traditional banks require.

We look at the big picture—not just a credit score. By focusing on the overall health and real-world potential of your business, we can uncover creative solutions and get a "yes" when others might say no.

Speed is Part of the Solution

We know that when you're looking to consolidate debt, you can't afford to wait around. The weeks or even months it can take to get an answer from a bank can put a massive strain on your operations. Our process was built from the ground up for speed.

Thanks to our strong, established relationships with a diverse range of lenders, we can often get preliminary decisions within 24 hours. Once you’ve been approved and have accepted an offer, the funds can be in your account in as little as 24 to 48 hours.

Our mission is simple: get you the right funding, right when you need it, so you can focus on running your business.

Frequently Asked Questions

When you're thinking about consolidating your business debt, it's natural to have a few questions pop up. Let's walk through some of the most common ones we hear from business owners.

Will Consolidating Debt Hurt My Business Credit Score?

This is a great question, and there are two sides to the coin. In the short term, applying for any new loan will trigger a hard credit inquiry, which might cause a small, temporary dip in your score. That's just part of the process.

But the long-term effect is what really matters, and it's almost always positive. Think about it: you're swapping out a handful of scattered, hard-to-manage payments for a single, predictable one. Making that payment on time, every time, builds a strong, positive payment history—and that's a huge factor in boosting your business credit score over the long haul.

Can I Get Approved with Bad Personal Credit?

While a great personal credit score certainly opens more doors, it's not always the make-or-break factor it used to be. Many lenders today, especially in the alternative funding space, are more interested in the health and performance of your actual business.

They'll look closely at things like:

- Your monthly revenue consistency

- Your overall cash flow

- How long you've been in business

If your company has solid sales and can clearly handle the new, single payment, many lenders will see that as a good risk, even if your personal credit has seen better days.

What Is the Difference Between a Consolidation Loan and MCA Consolidation?

It's easy to get these mixed up, but they're fundamentally different tools for different problems. A standard consolidation loan is exactly what it sounds like: you take out one larger loan, use that money to pay off all your smaller debts, and then you just have that one new loan to manage. Simple.

On the other hand, an MCA consolidation (often called a reverse consolidation) isn't about paying off your debts. It's a cash flow rescue mission. It gives you regular cash injections to cover your daily or weekly MCA payments, which you then repay over a more manageable term. It's designed to stop the immediate cash bleed from high-frequency payments.

How Quickly Can I Get Funded?

This is where working with a funding partner really shines compared to a traditional bank. The bank loan process can be a real grind, often dragging on for weeks or even months. When you're trying to get your finances under control, that kind of delay can be a killer.

Our process at Funding Solution Experts is built for speed. After you fill out a quick application, you can start seeing preliminary offers within 24 hours. From there, once you pick the right option and finalize everything, the funds can be in your account in as little as 24 to 48 hours. You can go from feeling overwhelmed to being back in control in just a couple of days.

Ready to simplify your finances and get your cash flow back on track? The team at FSE - Funding Solution Experts can connect you with the right debt consolidation solution from our network of over 50 lenders. Get your no-obligation funding estimate today.