Yes, securing fast business loans with bad credit is absolutely possible. In fact, for many entrepreneurs I’ve worked with, it’s a necessary and achievable step toward growth.

Think of it this way: a traditional bank loan is like a single, rigid bridge. If your credit score doesn't meet its strict requirements, the gate is closed. But alternative lending is more like a whole network of high-speed ferries. They’re built to get you where you need to go now, and they navigate based on your business's real-time performance, not just old maps.

Your Credit Score Is an Obstacle, Not a Barrier

Getting a loan rejection can feel like hitting a brick wall, especially when a critical opportunity or an unexpected expense pops up. Many business owners mistakenly believe a low FICO score automatically shuts them out of any chance for funding.

The truth is, your personal credit score is just one chapter in your business's story. It’s a snapshot from the past, not a live feed of your current success.

Modern lenders and finance partners get it. They know a business's real health is measured by its current cash flow, consistent revenue, and operational history. They care far more about what your business is doing today than what your credit report said yesterday. This simple shift in focus opens up a whole new world of financing possibilities.

The New Rules of Lending

For businesses in fast-moving industries like construction, trucking, or retail, waiting around for a bank’s six-week approval process just isn't an option. Cash flow is everything. Delays can halt projects, ground fleets, or cause you to miss out on crucial inventory.

This is exactly where an experienced lending partner like FSE - Funding Solution Experts comes in, helping you navigate the alternative funding landscape to find options that actually fit your situation. These lenders are looking at a different set of rules.

To them, your business's recent performance speaks volumes. Here's what they're actually evaluating:

- Consistent Monthly Revenue: Can you show that your business generates reliable income? This is often the single most important factor.

- Time in Business: A proven track record, even just for a year or two, demonstrates stability and resilience.

- Healthy Bank Statements: Lenders want to see consistent deposits and a stable average daily balance. It’s a clear signal that you manage your cash well.

This table breaks down the core factors alternative lenders evaluate, helping you see where your business's true strengths lie.

Key Metrics Lenders Prioritize Over Credit Score

| Alternative Lending Factor | What Lenders Actually Look For | Why It Matters More Than Your Score |

|---|---|---|

| Cash Flow | Consistent daily/monthly deposits and a stable average bank balance. | It's the most direct indicator of your ability to handle repayments. Strong cash flow proves you can afford the loan. |

| Revenue History | Proof of at least $10,000 - $20,000 in monthly sales, verified through bank statements. | This shows your business has a solid customer base and a viable operating model, reducing the lender's risk. |

| Time in Business | At least 6-12 months of operational history at a minimum. | A longer history demonstrates you've navigated early challenges and built a sustainable business. |

| Industry Risk | Your specific industry’s stability and performance trends. | Some industries have more predictable revenue cycles, making them a safer bet for lenders regardless of credit. |

Ultimately, lenders are looking for momentum. If your business is on an upward trajectory, they’ll see potential where a traditional bank might only see a past mistake.

Data Proves Funding Is Accessible

This isn't just a hunch; the numbers back it up. A 2026 study revealed a powerful trend: a full 20% of all approved small business loan applicants had personal credit scores of 659 or below.

Even more telling, the analysis showed that 80% of these approvals went to businesses pulling in at least $500,000 in annual revenue. This highlights a clear reality: strong business performance can and does trump a challenging credit history. You can explore more about these small business funding trends and see how they're reshaping approvals.

The key takeaway is this: Modern lenders are more interested in your company's ability to generate revenue and manage its finances than they are in a three-digit score from your past. Your business's momentum is your greatest asset.

So, while a bad credit score is a hurdle, it's one you can definitely clear. With the right strategy and a clear presentation of your business's current financial health, the path to fast funding is paved with your recent bank statements and proof of revenue, not old credit reports.

Why Today's Lenders Care More About Your Cash Flow Than Your Credit Score

If you've ever applied for a traditional bank loan, you know the feeling. Your business's fate seems to hang on a single number: your personal credit score. One dip, one past mistake, and the door slams shut, no matter how well your company is doing right now. This is where modern lenders have completely changed the game.

Think of your credit score as an old, black-and-white photograph. It shows a single moment from your past, but it says absolutely nothing about your business today. Alternative lenders, on the other hand, want to see the live video stream.

That "live stream" is your recent bank statements, your daily sales, and your monthly revenue. It's a real-time, dynamic picture of your company's health, and it's a much better way to gauge if you can handle a new loan. For any business owner looking for fast business loans with bad credit, this shift is a game-changer.

It’s All About Present Performance

Alternative lenders built their entire model on a simple truth: past financial struggles don't have to define a business's future. They focus on what’s happening in your business right now. Their first question isn't "What happened five years ago?" It's "How did you do last month?"

They look for a few key indicators that tell a much more powerful story than any credit report:

- Consistent Cash Flow: They want to see regular deposits hitting your business bank account. It’s direct proof that you have customers and a steady income stream.

- Strong Monthly Revenue: Hitting a certain revenue target, often around $10,000 to $20,000 a month, shows that your business model actually works.

- Time in Business: Having at least a year under your belt proves you've cleared the initial startup hurdles and found your place in the market.

This approach lets lenders make smart decisions, fast. Instead of getting bogged down in old credit histories for weeks, they use technology to analyze your recent financials in a matter of hours.

A lender's real goal is to understand one thing: can you make the payments? A strong, consistent flow of sales provides far more convincing proof of that than a FICO score ever could.

Why Your Business's Health Trumps Your Personal Score

Let's be blunt: a business pulling in $30,000 a month with a low credit score is often a much better bet than a business with perfect credit but spotty, low sales. Why? Because revenue is what pays back the loan. Simple as that. A high credit score shows you were responsible in the past, but strong cash flow proves you have the capacity to pay right now.

This is a huge advantage for businesses in industries like construction or trucking, where you might have massive invoices coming in but your personal credit took a hit during a slow season. Your bank statements show the real story of your success. Alternative lenders are experts at reading that story, which is what makes them such a critical partner when you need funding without the wait.

When you need cash fast and your credit isn't perfect, it can feel like you're out of options. But the truth is, the lending world has changed. Today, your business's performance—specifically its revenue—can open doors that a credit score might have previously slammed shut.

Let's break down the most common routes to fast funding so you can see which tool is right for the job.

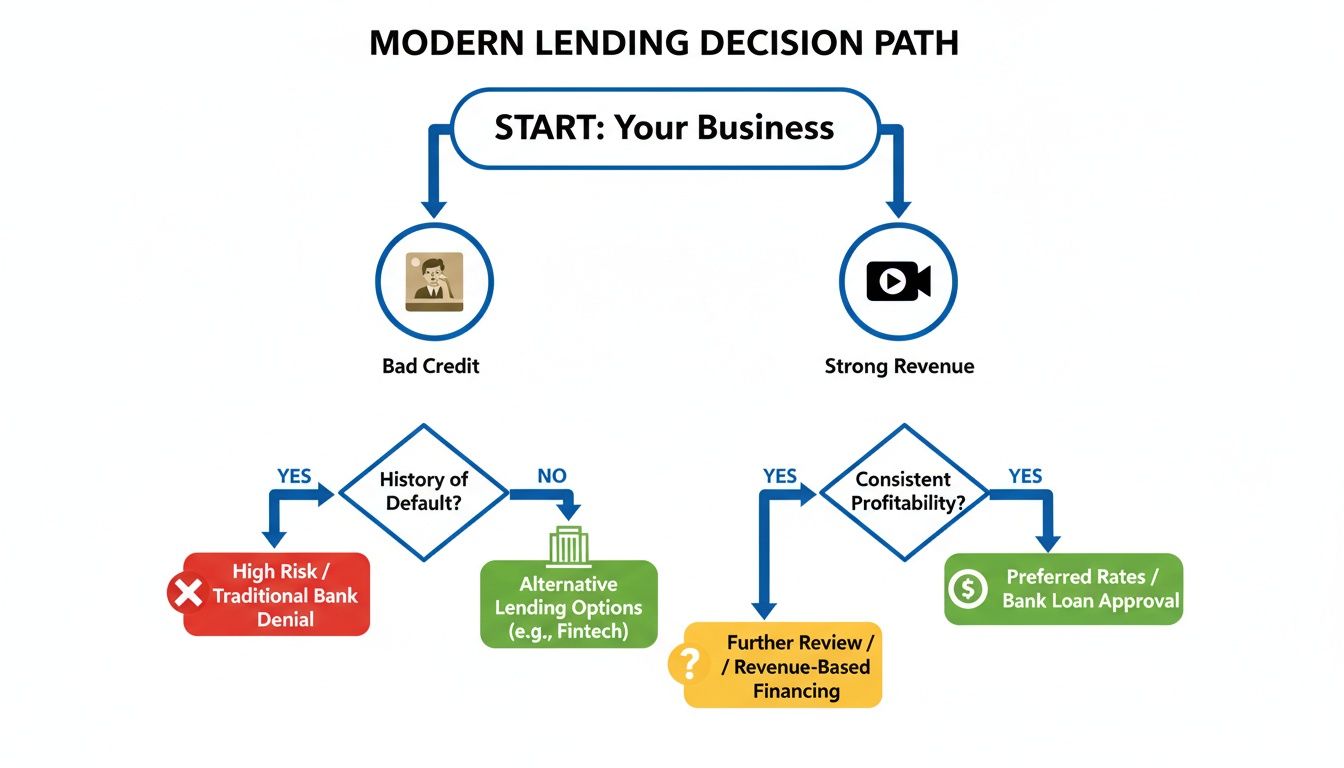

The modern lending path isn't a single road. Lenders now evaluate businesses on two parallel tracks: historical credit data and current financial health. For business owners with a few dings on their credit report, that second track is everything.

As you can see, strong, consistent revenue creates a direct line to funding, bypassing the traditional roadblocks of a low credit score.

With that in mind, let's look at the different kinds of funding that prioritize your cash flow over your FICO score.

Merchant Cash Advance (MCA)

First things first: a Merchant Cash Advance (MCA) isn't actually a loan. Think of it more as a sale. You're selling a small slice of your future credit and debit card sales in exchange for cash in your hand right now.

Imagine you run a bustling coffee shop and need $20,000 to buy a new espresso machine. An MCA provider gives you that cash today. In return, they'll automatically take a small, agreed-upon percentage (say, 10%) from your daily card sales until the advance is paid back. On a slow Monday, you pay less. After a packed weekend, you pay more. Your payments breathe with your business.

Best For:

- Restaurants, retail shops, and salons with high daily card sales.

- Businesses that need capital immediately, often without a hard credit pull.

- Owners who value repayments that align directly with their daily revenue.

The real beauty of an MCA is that its repayment structure is tied to your daily sales. This flexibility is a game-changer during slow seasons because you’re never stuck with a massive fixed payment you can’t afford.

Online Term Loans

Traditional bank loans are often a non-starter if you have bad credit, but online lenders have stepped in to fill that gap. These are typically short-term loans that give you a lump sum of cash, which you then repay over a set period—usually 6 to 24 months—with predictable, regular payments.

A construction firm, for instance, might land a big project and need $50,000 for materials upfront. An online term loan can deliver that capital quickly. The firm gets a clear repayment schedule with fixed weekly or monthly payments, making it easy to budget for the project and manage cash flow. For these fast business loans bad credit options, lenders are far more interested in your annual revenue and how long you've been in business than your credit score.

Invoice Financing

If you run a B2B company, you know the pain of waiting 30, 60, or even 90 days for clients to pay their invoices. Invoice financing (also known as factoring) is the solution. It lets you sell those outstanding invoices to a financing company and get most of their value in cash almost immediately.

Let's say a logistics company completes a $30,000 shipment, but the client's payment terms are 60 days. Waiting two months for that cash just isn't feasible. With invoice financing, they can get up to 90% of that invoice ($27,000) within a day or two. The financing company then collects the full payment from the client, sends the logistics company the remaining balance, and keeps a small fee for their service.

Business Lines of Credit

A business line of credit is your financial safety net. It operates just like a credit card: you're approved for a set credit limit (e.g., $25,000), and you can draw funds from it whenever you need to, up to that limit. You only pay interest on the money you've actually used.

The best part? As you repay the funds, your available credit gets replenished, ready for the next time you need it.

This is the perfect tool for managing unexpected costs or bridging cash flow gaps. A plumbing contractor could use their line of credit to make payroll while waiting for a big client check to clear, or to pay for an emergency repair on their main service vehicle.

For business owners in service industries, working with specialized brokers can be a huge advantage. These firms have relationships with dozens of lenders and can often secure funding in just 24-48 hours for companies with over $10,000 in monthly revenue. You can learn more about how these bad credit business loan options work to find a fit for your specific operational needs.

Comparing Fast Business Loan Options for Bad Credit

Feeling a bit overwhelmed? This side-by-side comparison helps you quickly evaluate the most common financing types based on speed, requirements, and best-fit scenarios.

| Loan Type | Typical Funding Speed | Primary Requirement | Best Use Case |

|---|---|---|---|

| Merchant Cash Advance (MCA) | 1-2 Days | Consistent daily credit/debit card sales | Quick cash for retail, restaurants, and other businesses with high card transaction volume. |

| Online Term Loan | 1-3 Days | Strong annual revenue and at least 1-2 years in business | A lump sum for a specific project, equipment purchase, or expansion. |

| Invoice Financing | 1-3 Days | High-quality B2B invoices from creditworthy customers | Solving cash flow gaps caused by slow-paying clients. |

| Business Line of Credit | 2-5 Days | Consistent monthly revenue and business operating history | Managing ongoing, unpredictable expenses or having a flexible cash reserve. |

Each option has its place. The key is to match the funding product not just to your immediate need, but to how your business actually operates and earns money.

How to Prepare a Winning Loan Application

Getting approved for a fast business loan isn't about luck—it's about preparation. Think of your loan application as the complete story of your business's health and its potential. When you're dealing with bad credit, that story is even more important because it has to prove that your current performance is stronger than your financial past.

A messy, incomplete application sends a loud and clear signal to lenders: this business might be a risk. On the other hand, a well-prepared package shows you're professional, stable, and have a firm grasp on your finances. It’s your best shot at making a lender feel confident in your ability to succeed.

The whole point is to paint a picture of reliability and growth, making the approval of a fast business loan for bad credit an easy "yes" for the lender.

Your Essential Document Checklist

Before you fill out a single form, get your documents in order. Having everything on hand doesn't just speed things up; it proves to the lender that you're serious and organized. Lenders specializing in fast funding want a real-time snapshot of your business, so these documents are almost always non-negotiable.

Here’s what you'll most likely need:

- Recent Bank Statements: Lenders will ask for your last 3 to 6 months of business bank statements. They're scanning for consistent monthly deposits, a healthy average daily balance, and very few (if any) overdrafts or negative balance days.

- Proof of Revenue: This could be your credit card processing statements or a recent profit and loss statement. The idea is to confirm your business hits their minimum revenue targets, which is often at least $10,000 per month.

- Government-Issued Photo ID: A simple driver’s license or passport to verify who you are.

- Business License and Formation Documents: This proves your business is a legitimate, registered entity.

- Voided Business Check: This is needed to set up the direct deposit for your funds and for automatic repayments.

Get these files scanned and saved in a digital folder. This one simple step can shrink a multi-day process down to a matter of hours.

Strategies to Strengthen Your Application

It’s not just about submitting documents; it’s about how you tell your business's financial story. Your application is a marketing tool for your company's stability. Use these strategies to put your best foot forward, even if your credit history has some bumps.

A winning application doesn't hide weaknesses; it explains them concisely while emphasizing current strengths. Lenders appreciate transparency and are more likely to fund a business owner who can demonstrate self-awareness and control over their finances.

First, make your revenue consistency the star of the show. If your sales are seasonal, be ready to explain the ebbs and flows. Lenders get it—a construction company’s revenue might dip in the winter—but showing predictable, strong peaks builds a lot of confidence.

If there's a specific, one-time reason for your bad credit, like a past medical emergency or a major client who went bust, write a brief letter of explanation. Just one paragraph. Keep it factual, professional, and unemotional. Taking this step shows you own it and have since moved on.

Finally, clean up your bank accounts before you apply. In the weeks leading up to your application, try to keep a higher average daily balance and avoid non-sufficient funds (NSF) fees like the plague. Underwriters see those as massive red flags for cash flow problems. A clean bank statement is one of your most powerful assets.

Maximizing Your Approval Odds

Even without perfect credit, the opportunity for funding is real for small and mid-sized businesses. One study found that 22% of approved loans went to businesses with under $500,000 in annual revenue, as long as they met the lender's minimums. You can dig into the data behind these fast business loan approvals to see just how much strong revenue can open doors. A solid application is the key to unlocking these opportunities and making the strongest possible case for your business.

Navigating Rates, Risks, and Repayment Terms

Let's talk about the most important part of this whole process: understanding the true cost of the money you're borrowing. When you have less-than-perfect credit, the rates and terms will look different from a traditional bank loan, and that's okay. But they shouldn't be a mystery. Getting a firm grip on these numbers is what separates a smart growth investment from a new financial headache.

You'll run into two main ways lenders talk about cost: Annual Percentage Rate (APR) and factor rate. They both tell you the price of borrowing, but they work in completely different ways. Mixing them up can lead to some nasty surprises when you see how much you actually owe.

APR vs. Factor Rate: An Analogy

Think of it like planning a road trip.

An APR is like paying for gas by the gallon. Your total cost depends on how long the trip is (the loan term) and the price you pay at the pump (the interest rate). It’s a rate that adds up over time, which is what you see with traditional loans and lines of credit.

A factor rate, on the other hand, is like buying a single, all-inclusive train ticket. You know the exact cost of the entire journey before you even leave the station. It’s a simple multiplier that’s applied to your loan amount, fixing the total payback from day one, no matter how fast you repay it.

Factor rates are the language of fast-funding options like Merchant Cash Advances. If you take a $20,000 advance with a 1.25 factor rate, you’ll pay back a total of $25,000. The math is simple: $20,000 x 1.25. Your cost is a flat $5,000. Period.

This predictability is a huge advantage when you’re managing tight cash flow. There are no shifting goalposts; you always know exactly what you’re on the hook for.

Calculating the True Cost of Capital

Knowing the total payback amount is step one. Step two is making sure that money will actually make you more money. Before you sign anything, you have to ask yourself one simple question: "Will this funding generate a bigger return than what it's costing me?"

If you're taking a $10,000 advance that costs $2,500 to buy inventory that will net you $7,000 in profit, that’s a no-brainer. You're walking away with a $4,500 gain. But if you’re just using it to cover payroll without a solid plan to increase revenue, you might just be kicking a bigger financial can down the road.

Here's a quick checklist to gut-check the ROI:

- What’s the Goal? Pinpoint the specific, revenue-generating activity this money will fuel. Think: buying a new piece of equipment, launching a targeted marketing campaign, or stocking up on in-demand inventory before a busy season.

- What's the Payoff? Realistically estimate the profit you expect this investment to create.

- Does it Add Up? Does your projected profit comfortably cover the total cost of the funding?

The Danger of "Loan Stacking"

One of the biggest traps business owners fall into is loan stacking. This is when you take out multiple cash advances or loans from different lenders at the same time. It might feel like an easy way to get more cash in the door, but it can create a death spiral for your cash flow.

Each new advance comes with its own daily or weekly payment, and before you know it, multiple withdrawals are draining your bank account every single day. It becomes nearly impossible to keep up.

Reputable lenders know this, which is why most will turn you down if they see you already have several active advances. They know that loan stacking dramatically increases the risk of default for everyone involved. The best strategy is to focus on paying down one source of funding before you even think about taking on another.

Even with these risks, the right financing at the right time can be a game-changer. For example, some of the best online lenders can get you funded in just one day with manageable terms from 12-24 months, giving you a clear path to repayment. For businesses with revenue under $500k/year, a long history can work in your favor; 71% of approved owners in this group had been in business for at least five years, which helped offset a low credit score. You can dive deeper into how these bad credit business loan options work to find the terms that best fit where your company is today.

Building a Stronger Financial Future

Getting a fast business loan when you have bad credit can feel like a lifeline. But it’s more than just a quick fix for a cash crunch—it's a real opportunity to start building a healthier financial foundation for your company.

Think of it as a bridge loan, not just for your immediate cash flow, but for your creditworthiness. If you manage it well, this loan can be the stepping stone that helps you graduate from high-cost, short-term options to more traditional, affordable financing down the road. You’re not just paying back a debt; you're actively rewriting your business's financial story.

Turning Repayment into a Credit-Building Tool

The most powerful thing you can do is make every single payment on time. It sounds simple, but it’s everything. When you work with alternative lenders who report to the major business credit bureaus—like Dun & Bradstreet, Experian Business, and Equifax Business—your on-time payments start building a positive track record.

This is critical because payment history is the single biggest factor in your business credit score. You're creating tangible proof that your business handles its obligations responsibly, which is exactly what future lenders want to see.

By successfully repaying a fast business loan, you are creating a new, positive data trail. This track record can gradually open doors to better terms, lower rates, and larger funding amounts in the future, making it easier to secure capital when your next growth opportunity arises.

Actionable Steps to Improve Your Financial Standing

Building a stronger financial future takes more than just good intentions. Beyond simply repaying your current loan, you need to be proactive. Here are some key strategies to work on improving both your business and personal credit profiles over the long term.

For Your Business Credit:

- Establish Trade Lines: Open accounts with suppliers and vendors who report your payment history. Every time you pay an invoice on time, you're adding another positive mark to your credit report.

- Monitor Your Reports: You'd be surprised how often errors pop up. Regularly check your business credit reports for mistakes and dispute them immediately. It's a simple way to clean up your profile and potentially boost your score.

- Keep Business Finances Separate: Always use a dedicated business bank account and credit card. It makes your books cleaner and shows lenders you’re serious about professional financial management.

For Your Personal Credit:

- Pay Down High-Balance Cards: Focus on chipping away at your personal credit card balances. Lowering your credit utilization ratio—the amount you owe versus your limit—can give your FICO score a significant lift.

- Automate Payments: The easiest way to avoid a late payment is to make it impossible to forget. Set up automatic payments for your personal bills and protect your score from accidental dings.

When you pair responsible repayment of your current fast business loans for bad credit with these smart habits, you create a powerful cycle. Today’s funding solves an immediate need, while your diligent financial management builds a more resilient and fundable business for tomorrow.

Frequently Asked Questions

When you're looking for fast funding with less-than-perfect credit, you're bound to have questions. It's a confusing space, so let's clear up some of the most common points to help you move forward.

Can I Really Get a Business Loan with No Credit Check?

You’ll see "no credit check" advertised everywhere, but the reality is a little different. Most lenders will still perform a soft credit check. The great news? A soft pull doesn't impact your credit score at all. It's mainly used to confirm you are who you say you are and to get a quick look at your financial background.

Think of it this way: these lenders are far more interested in your business's current health—your cash flow and monthly sales—than a credit score from your past. So while a true zero-check loan is extremely rare, the soft-check process is built for business owners just like you.

How Fast Is "Fast"?

It’s genuinely quick. For most of the financing options we've discussed, the speed is one of the biggest advantages.

Here's what a typical timeline looks like:

- Application: You can usually fill it out online in minutes.

- Decision: Approval can come through in just a few hours.

- Funding: Once you're approved, the money can hit your account in as little as 24 to 48 hours.

How is this possible? Online lenders use technology to connect to your bank accounts and instantly analyze your revenue data. This cuts out the weeks of manual paperwork and underwriting that bog down traditional bank loans.

What's the Lowest Credit Score I Can Have?

There isn’t a single number that works for everyone, especially in the world of alternative lending. Many providers of fast business loans for bad credit don't set a hard minimum FICO score. Instead, they weigh other factors much more heavily.

Lenders focus on your ability to make payments, and the best proof of that is consistent revenue. They'll typically want to see your business bringing in at least $10,000 in monthly revenue and operating for a minimum of one year.

If your business is hitting those numbers, a low credit score becomes much less of an issue. It’s no longer an automatic "no," which is a game-changer for entrepreneurs who’ve been shut out by banks.

Will Applying for These Loans Tank My Credit Score?

In nearly all cases, no—just applying won't hurt your score. Alternative lenders almost always use soft credit pulls for initial applications.

A hard inquiry, the kind that can ding your score by a few points, usually only happens much later in the process. It might come up if you decide to accept a specific offer, particularly for a term loan. This lets you shop around and compare your options without the fear of damaging your credit. Just be sure to ask the lender upfront to confirm they only do a soft pull to start.

Ready to see what you qualify for without the stress? At FSE - Funding Solution Experts, we specialize in connecting business owners with lenders who see your potential, not just your past. Find out your options in 24 hours with no obligation. Apply now on fseb2b.com