A merchant cash advance (MCA) isn't a loan in the traditional sense. Think of it less like borrowing and more like selling a slice of your future income for cash you can use right now. A funding company advances you a lump sum, and in return, they purchase a small, fixed percentage of your future card sales until the agreed-upon amount is paid back.

So, What Exactly Is a Merchant Cash Advance?

Let's break it down with an analogy. Imagine your business is a thriving coffee shop. A traditional bank loan is like getting a fixed-payment mortgage on your shop—you owe the same amount every month, rain or shine, whether you sell 50 lattes or 500.

An MCA, however, is like selling a portion of your future coffee sales. You get a lump sum of cash today to buy a new espresso machine. In exchange, the funder gets a small percentage of every credit card swipe—say, 10 cents of every dollar—until they’ve received the total amount they purchased. On a blockbuster Monday, you pay back more. On a slow, rainy Wednesday, you pay back less. The payment flexes with your cash flow.

This is the key distinction. Because it’s structured as a sale of future revenue, an MCA is considered a commercial transaction, not a loan. This is a crucial point because it means MCAs aren't subject to the same federal lending laws that cap interest rates. Instead of an interest rate, they use something called a factor rate to calculate the total repayment amount.

The Three Pillars of an MCA

To really get how an MCA works, you need to know three core components that define every deal:

- Advance Amount: This is simple—it’s the cash you get upfront. It’s the money that hits your bank account, ready to be put to work on inventory, marketing, or an unexpected repair.

- Factor Rate: This is a simple multiplier, usually between 1.1 and 1.5, that determines your total payback amount. If you get a $20,000 advance with a 1.2 factor rate, your total repayment will be $24,000 ($20,000 x 1.2). It's a fixed cost, calculated from day one.

- Holdback Percentage: This is the percentage of your daily credit and debit card sales that the MCA provider will collect to chip away at your balance. It’s automatically deducted from your daily batches, so you never have to remember to make a payment.

This repayment system is what sets an MCA apart. Since the amount you pay back each day is directly tied to your sales volume, the model has a built-in flexibility that fixed-payment loans just can't match. This makes it a popular choice for businesses with seasonal or unpredictable revenue, like retail shops, restaurants, and construction contractors.

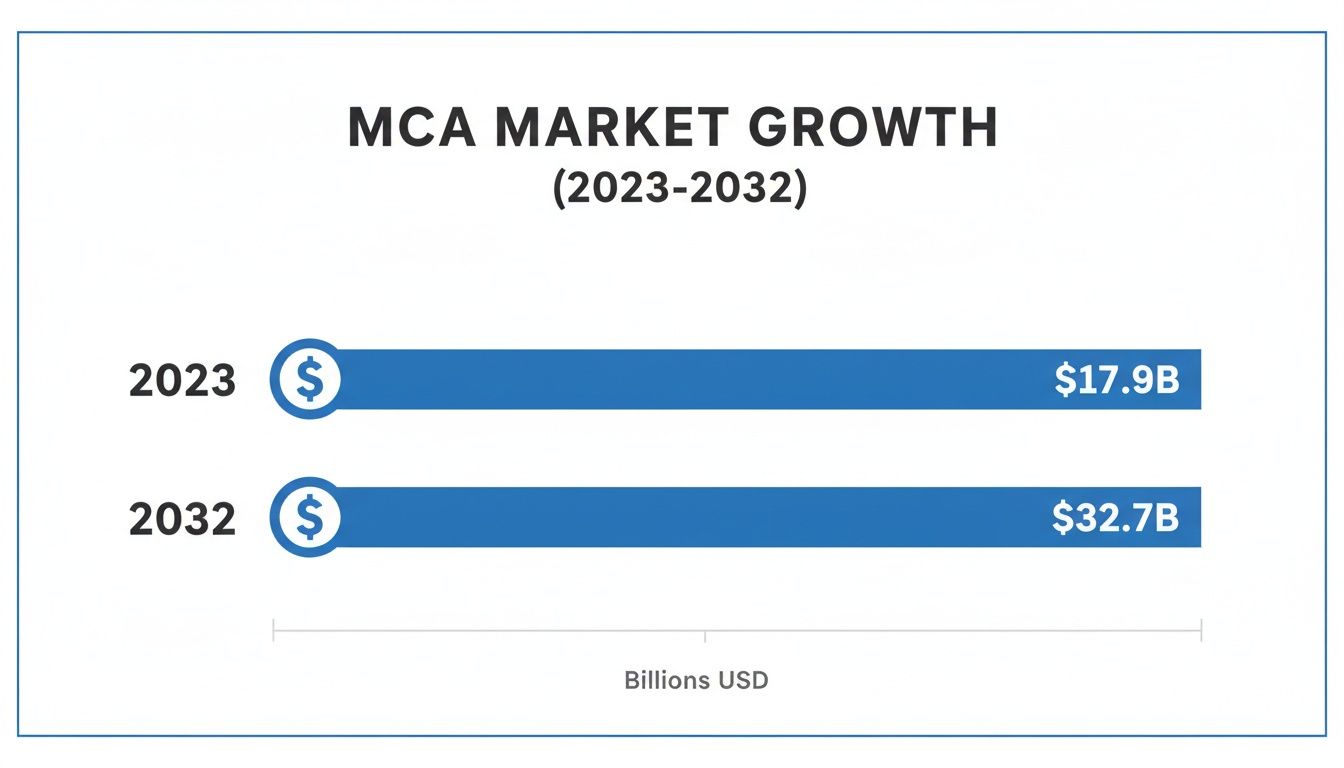

It's no surprise that this model has become a major player in business funding. The global merchant cash advance market was valued at a staggering $17.9 billion in 2023 and is on track to hit $32.7 billion by 2032. This explosive growth, detailed in this industry report on MCA growth, shows just how many small and mid-sized businesses are looking for fast, accessible capital when the doors to traditional banks are closed.

Merchant Cash Advance at a Glance

For a quick summary, here are the essential features of a merchant cash advance.

| Feature | Description |

|---|---|

| Product Type | Purchase of future receivables, not a loan. |

| Funding Amount | Typically $5,000 to $500,000, based on sales volume. |

| Repayment Method | Automatic daily or weekly deductions from sales. |

| Cost Structure | A fixed factor rate (e.g., 1.1 - 1.5) determines the total payback. |

| Repayment Term | Varies; typically 3 to 18 months, depending on sales performance. |

| Funding Speed | Extremely fast, often within 24-48 hours. |

| Credit Requirement | Lenient; poor credit is often acceptable as sales history is key. |

| Collateral | Unsecured; no personal or business assets are required. |

This table highlights why MCAs are a go-to for businesses needing immediate cash without the red tape of conventional financing.

How MCA Costs Are Calculated

If there’s one part of a merchant cash advance that trips people up, it’s the cost. It doesn’t work like a traditional loan, which uses an Annual Percentage Rate (APR). Instead, an MCA is built around a factor rate, and understanding this difference is the key to knowing what you’re really paying.

A factor rate is just a simple multiplier, usually somewhere between 1.1 and 1.5. The MCA provider applies this rate to the cash advance amount right at the start, which sets your total repayment amount in stone. You know the full cost from day one, and it never changes.

This kind of straightforward pricing is one reason MCAs have become so popular, fueling some serious market growth.

As you can see, the market is projected to skyrocket from $17.9 billion to $32.7 billion by 2032. It’s a clear sign that more and more small businesses are turning to this type of funding.

Factor Rate in Action: A Real-World Example

Let's break this down with a practical example.

Imagine your retail shop needs a quick $20,000 to stock up on inventory before the holiday rush. An MCA company offers you the funds with a factor rate of 1.25.

Here's how the math plays out:

- Advance Amount: $20,000

- Factor Rate: 1.25

- Total Repayment Amount: $20,000 x 1.25 = $25,000

Simple as that. The cost of your funding is a flat $5,000. This upfront clarity is a hallmark of how MCAs are priced.

The Hidden Impact of Repayment Speed

While the factor rate itself is easy to grasp, how fast you repay the advance dramatically changes its "true" cost. This is where people get confused comparing MCAs to loans.

An APR measures the cost of financing over a full year. MCAs, on the other hand, are typically paid back much faster—often in 3 to 12 months. When you try to express the fixed cost of an MCA as an annualized rate, the number can look shockingly high.

A faster repayment term means a higher effective APR. Since the total cost is fixed, paying it back over a shorter period concentrates that cost, making it more expensive in annualized terms.

Let’s go back to our $20,000 advance that costs $5,000.

- If you repay it in 12 months: The cost is spread out, resulting in a more moderate effective APR.

- If you repay it in 4 months: You're packing the same $5,000 cost into a much shorter timeframe, which makes the effective APR shoot way up.

The total cash you paid out is still $5,000 in both cases. But this illustrates why a direct APR-to-APR comparison between a short-term MCA and a long-term bank loan is often like comparing apples to oranges.

Why MCAs Are Not Governed by Usury Laws

The difference between a factor rate and an APR isn't just financial jargon; it's a critical legal distinction. An MCA is structured as the purchase of a portion of your future sales, not a loan. Because of this, MCAs have historically been exempt from state usury laws, which put a cap on the interest rates that lenders can charge.

But the ground is shifting here. States like New York and Texas are taking a closer look, and some are pushing for new regulations to bring more transparency and protection to business owners. It’s an evolving landscape, which really underscores the importance of working with a knowledgeable funding advisor who can help you read the fine print and understand exactly what you're signing up for.

Understanding the Repayment Process

One of the most defining—and honestly, most misunderstood—features of a merchant cash advance is how you pay it back. It’s not like a traditional loan where you’re cutting a fixed check on the 15th of every month. Instead, an MCA’s repayment system is built to work with the natural ebb and flow of your business.

The whole process is designed to be automated and hands-off, so you can keep your focus on running your business, not on juggling another payment deadline. Let's break down the two main ways funders collect on the receivables they've purchased: split withholding and automated (ACH) withdrawals. Each has its own mechanics, and one is usually much friendlier to your cash flow than the other.

The Split Withholding Method

The most common and, frankly, the most intuitive structure is split withholding. This method links your repayments directly to your daily credit and debit card sales. It's simple. A small, agreed-upon percentage of your daily card sales is automatically routed to the MCA provider before the rest hits your bank account.

Think of it like paying a sales rep on commission. If your holdback percentage is 10%, your credit card processor simply sends 10% of each day's batch to the funder and the remaining 90% to you.

Let’s look at a real-world example.

Imagine a popular local coffee shop that just got an MCA to buy a new, high-end espresso machine. Their agreement has a 10% holdback.

- On a busy Friday, they do $3,000 in credit card sales. The MCA provider gets its cut of $300 (10% of $3,000), and the coffee shop is left with $2,700.

- But on a slow, rainy Tuesday, sales drop to $800. That day’s repayment is only $80 (10% of $800), leaving them with $720.

This self-adjusting payback is the real magic of a true MCA. It’s a built-in safety net. Your payments are bigger when business is booming and smaller when things are slow, protecting your cash flow when you need it most.

To see this in action, let's look at how a week of sales might affect the repayment balance.

Sample MCA Daily Repayment Calculation (Split Method)

This table shows how daily repayments would fluctuate for a business with a 10% holdback on a starting advance balance of $20,000.

| Day | Daily Card Sales | Holdback (10%) | Remaining Balance |

|---|---|---|---|

| Monday | $2,000 | $200 | $19,800 |

| Tuesday | $1,500 | $150 | $19,650 |

| Wednesday | $2,200 | $220 | $19,430 |

| Thursday | $1,800 | $180 | $19,250 |

| Friday | $3,500 | $350 | $18,900 |

As you can see, the payment amount is never fixed. It rises and falls in perfect sync with the business's daily performance.

The Fixed ACH Withdrawal Method

The other, less flexible option is a fixed ACH withdrawal. Instead of taking a percentage, the MCA provider debits a set daily or weekly amount directly from your business bank account. This figure is usually calculated based on an estimate of your future sales.

While this approach gives you a predictable payment amount, it completely loses the flexible, revenue-based nature that makes MCAs appealing in the first place.

Think back to our coffee shop. If they had a fixed $250 daily ACH payment and had that slow Tuesday with only $800 in sales, that $250 payment would still come out. That’s a huge chunk of their revenue for the day, putting a serious strain on their cash flow.

This is a critical distinction. A lot of products marketed as MCAs are actually just short-term loans in disguise, precisely because they use these fixed ACH payments. This structure has even faced legal challenges, with courts arguing that because the payment isn't tied to actual sales, it's a loan, not a true sale of future receivables.

What About Reconciliation?

To get around the rigidity of fixed ACH payments, some providers offer a reconciliation or "true-up" clause. This feature allows you, the business owner, to contact the funder (usually once a month) with proof of your sales.

If your actual revenue was lower than what they based the fixed payment on, they might adjust future payments or even refund the difference.

But here’s the catch: the burden is almost always on you. It's not automatic. You have to track your sales, spot the discrepancy, contact the provider, and formally request the adjustment. This adds an administrative headache that simply doesn't exist with the split withholding method. If you’re considering an MCA with fixed ACH payments, you absolutely need to know if it has a reconciliation clause and exactly how that process works.

Is a Merchant Cash Advance Right for Your Business? Let's Break It Down

A merchant cash advance can be a game-changer, putting cash in your hands when you need it most and every bank has said no. But it's not a magic bullet. Think of it less like a traditional loan and more like a high-octane fuel for your business—incredibly powerful, but you have to know when and how to use it.

Getting this decision right means looking past the sales pitch and weighing the real-world pros against the very real cons. For the right company in the right spot, an MCA can unlock serious growth. For the wrong one, it can become a costly burden.

The Upside: Why Businesses Turn to MCAs

When you're facing a can't-miss opportunity or an unexpected cash crunch, the rigid process of traditional financing just won't cut it. This is where an MCA really shines.

Seriously Fast Funding: The number one reason business owners choose an MCA is speed. Forget the weeks or months of underwriting and endless paperwork that come with a bank loan. With an MCA, it’s not uncommon to see cash in your account in as little as 24 to 48 hours. This is perfect for emergencies, like when your primary delivery van breaks down, or for grabbing a massive, time-sensitive inventory discount from a supplier.

Bad Credit? No Problem: MCA providers care more about your sales than your FICO score. Their decision is based on the health of your daily cash flow, not a years-old blemish on your credit report. This opens the door for newer businesses, owners with less-than-perfect credit, or those without significant collateral to pledge.

Payments That Rise and Fall with Your Sales: This is a huge advantage for businesses with unpredictable revenue streams—think seasonal retailers, restaurants, or construction contractors. Instead of a fixed payment that can cripple you during a slow month, MCA repayments are tied to a percentage of your daily sales. When business is booming, you pay back more; when things quiet down, your payment shrinks to match.

The Downside: What to Watch Out For

That speed and accessibility come at a cost, and it's a detail you absolutely cannot ignore. Before you sign on the dotted line, you need to understand the trade-offs.

The biggest hurdle is the high cost. An MCA isn't a loan, so it doesn't have an APR. But if you were to calculate an equivalent rate, it would often be in the triple digits. The cost is front-loaded into a fixed factor rate, and since you're paying it back over a short term (often just a few months), the effective cost is concentrated. While comparing it directly to a multi-year bank loan's APR isn't quite apples-to-apples, the takeaway is the same: an MCA is one of the most expensive ways to fund a business.

You have to treat an MCA as a tool for generating a clear return on investment. If you're using the funds to buy inventory that you can flip for a profit far greater than the cost of the advance, it's a smart move. If you're just using it to cover payroll, the high cost can quickly erode your profits.

Another critical point is the lack of federal regulation. Because MCAs are technically a "purchase of future sales," not a loan, they fall outside the scope of federal lending laws like the Truth in Lending Act. This means no federal caps on rates and fewer protections for the business owner, which has unfortunately allowed some less-than-reputable funders to engage in predatory practices.

Some states, like New York and California, are stepping in with their own disclosure requirements to create more transparency, but the rules aren't consistent nationwide. This regulatory patchwork makes it even more important to work with a trusted broker who can vet providers and help you understand exactly what you're signing.

At the end of the day, an MCA is a highly specialized product. It's built for speed and short-term, high-return scenarios, not for funding day-to-day operations over the long haul.

How to Qualify and Apply for an MCA

Getting a merchant cash advance is meant to be a simple, no-fuss process. It’s a world away from the hoops you have to jump through for a traditional bank loan. MCA providers aren't as concerned with perfect credit scores or years of business history; they focus on the lifeblood of your business—your recent sales.

This approach is what makes funding accessible for so many businesses that might not tick the right boxes for a bank. And because funders know that opportunities (and emergencies) don't operate on a banker's schedule, the entire process is built for speed.

What Do Funders Look For?

While the specifics can vary from one provider to the next, they all zero in on a handful of core metrics. These numbers paint a clear picture of your revenue stability and give them confidence in the future sales they're essentially buying a piece of.

Generally, here's what they're looking for:

- Time in Business: Most funders want to see that you’ve been up and running for at least one year. Some are more flexible and will consider businesses as young as six months old if the sales are strong.

- Monthly Revenue: Consistent cash flow is everything. A common benchmark is a minimum of $10,000 to $15,000 in gross monthly revenue.

- Card Sales Volume: Because repayment is often tied directly to your credit and debit card sales, providers need to see that you have a healthy, consistent volume of these transactions.

It's worth repeating: MCA funders are far more interested in your recent cash flow than your personal credit score. A low FICO score isn't an automatic "no" if your bank statements show a thriving, active business.

The Application and Documentation Process

One of the biggest draws of an MCA is how little paperwork is involved. You can often complete the entire application online in just a few minutes and get a decision in a matter of hours, not weeks.

To get the ball rolling, you’ll just need to pull together a few key documents that prove your sales history.

- The Application: This is usually a simple online form asking for your business basics—name, contact info, how long you've been in business, and a ballpark of your monthly sales.

- Bank Statements: You'll need your last 3-6 months of business bank statements. This is how funders verify your overall revenue and check for consistent cash flow.

- Processing Statements: The last 3-6 months of statements from your credit card processor are crucial. This document shows them exactly how much you're bringing in through card sales, which is the foundation of the whole deal.

And that's usually it. You can forget about digging up old tax returns, creating detailed financial forecasts, or writing a formal business plan. This streamlined approach is precisely what allows funders to get you an answer—and often the cash—in as little as 24 hours.

Partnering with a funding advisor like FSE - Funding Solution Experts can simplify things even further. Instead of filling out application after application, you submit your information just once. Your advisor then does the legwork, presenting your file to a network of trusted funders to find you the best rates and terms. It saves a ton of time and ensures you see all the offers on the table.

What Are the Best Alternatives to a Merchant Cash Advance?

While a merchant cash advance delivers on speed and accessibility, it's just one tool in a much larger funding toolkit. Getting a handle on your other options is the key to making a smart financial move—one that actually lines up with where you want to take your business.

In many cases, a more traditional product like a line of credit or a term loan might be a much better fit, often at a lower cost. Looking at these alternatives helps ensure you're not just plugging a short-term cash gap but building a stronger financial future for your company.

Let's break down some of the most common alternatives.

Business Line of Credit

Think of a business line of credit as a credit card, but for your company. You get approved for a certain credit limit, and you can draw funds from it whenever you need to, paying interest only on what you actually use. This flexibility makes it a fantastic tool for smoothing out the natural ups and downs of cash flow.

- Best Use Case: Perfect for managing inconsistent revenue, covering payroll during a slow month, or just having a financial safety net for those "just in case" moments.

- Key Difference from an MCA: This is a revolving line. As you pay back the funds you've borrowed, your available credit goes right back up. The cost is based on an interest rate, which often translates to a much lower effective APR than an MCA.

Short-Term Loans

A short-term loan gives you a single lump sum of cash that you pay back with fixed payments—usually daily or weekly—over a set period, typically anywhere from three to 18 months. Critically, this is a true loan, not a sale of future receivables. That means it comes with a stated interest rate and a clear repayment schedule.

While the approval process is still worlds faster than a traditional bank's, it can be a bit more rigorous than an MCA and might require a stronger credit history.

A short-term loan really shines when you need a specific amount of money for a project where you can confidently predict the return. The predictable payment structure makes budgeting a breeze.

Equipment Financing

Need a new piece of machinery, a delivery vehicle, or specialized tech? Equipment financing is designed for exactly that. The equipment you're buying acts as the collateral for the loan, which is a huge advantage.

Because the loan is secured by a hard asset, lenders are often willing to offer better rates and terms than you'd find with unsecured funding. The loan amount is tied directly to the equipment's value, and providers can often work with businesses that don't have perfect credit. It’s a straightforward way to get the tools you need to grow without tying up all your working capital in the purchase, making it a powerful alternative to a general-purpose merchant cash advance.

Frequently Asked Questions About MCAs

It’s completely normal to have a ton of questions when you’re looking into business funding. A merchant cash advance, in particular, has its own unique quirks, and getting your head around them is the first step to making a smart decision for your company.

Let's cut through the noise and get straight to the answers you're looking for.

Will an MCA Affect My Personal Credit Score?

For the most part, no. When you apply for an MCA, the provider is far more interested in your business’s sales history and cash flow than your personal credit report. They’ll typically run a soft credit pull, which is just for their eyes and won't ding your score.

Since an MCA is a sale of future receivables—not a loan—your payments aren't reported to personal credit bureaus like Equifax or TransUnion. But there's one big catch: almost every MCA agreement includes a personal guarantee. This means if the business can't pay back the advance, you’re personally on the hook for it.

What Happens if My Business Sales Slow Down?

This is where the design of an MCA can be a huge help. If your advance is structured with a percentage-based holdback, your payments flex with your revenue. When sales are down, the amount you pay back also goes down. It’s an automatic adjustment.

This flexibility is one of the biggest draws compared to a traditional loan, which requires the same fixed payment whether you had a record month or a terrible one. It gives you some breathing room when things get tight.

However, if your MCA uses a fixed daily or weekly ACH payment, a sales slump can create a serious cash flow problem. That's why it is absolutely critical to know exactly what kind of repayment structure you're agreeing to before you sign anything.

Is a Merchant Cash Advance a Loan?

Legally, a merchant cash advance is not a loan. It’s classified as a commercial transaction where you sell a portion of your future sales at a discount. This isn't just wordplay; it's a critical legal difference.

Because MCAs aren't loans, they don't fall under the same federal banking regulations, like usury laws that put a cap on interest rates. This is the reason providers use a "factor rate" instead of an APR. Grasping this distinction is key to truly understanding the cost of this type of funding.

How Quickly Can I Receive Funds From an MCA?

Speed is the name of the game with MCAs. If you need cash yesterday, this is often the fastest way to get it. While a bank loan can drag on for weeks or even months, an MCA is built for speed.

From filling out a simple application to seeing the funds hit your bank account, the entire process can take as little as 24 to 48 hours. This makes it a powerful tool for jumping on time-sensitive opportunities or handling unexpected emergencies without missing a beat.

Ready to explore your funding options without the wait? At FSE - Funding Solution Experts, we connect you with a network of over 50 lenders to find the best fit for your business. Get a no-obligation quote and see what you qualify for in minutes. Apply now and get funded fast.