When a game-changing opportunity lands on your desk, waiting weeks for a traditional bank loan just isn't an option. You can literally watch the opportunity slip away. This is where quick-approval business loans come in, giving you a vital alternative with access to capital in as little as 24-48 hours.

That kind of speed means you can act decisively, whether you're pouncing on a growth opportunity or navigating an unexpected emergency.

Why Fast Business Funding Is No Longer Just an Option

In today's market, speed is everything. It's a genuine strategic advantage. The ability to access capital quickly can be the single factor that separates you from the competition—the difference between landing a huge project or losing it.

Let's be honest, the slow, paper-heavy process of traditional lending feels completely out of sync with the pace of modern business.

Think about it. A construction firm wins a massive contract but needs to buy materials now to hit an aggressive deadline. Waiting on a bank committee for weeks is a non-starter. Or consider a retail shop that needs to stock up on seasonal inventory before a competitor beats them to it and captures all the holiday shoppers. These aren't edge cases; this is the reality for entrepreneurs who need to move fast.

The Widening Gap in Business Lending

The frustrating part is that as the need for speed has grown, traditional lenders have actually gotten more cautious. For a lot of small businesses, the old way of getting capital is simply broken.

It's a tough pill to swallow, but large banks now approve only 14.6% of small business loan applications. That creates a massive funding gap. This reality is exactly what has spurred the growth of alternative lenders and brokerage platforms built for speed and flexibility. If you want to dig deeper, you can explore the latest trends in the state of small business lending to see just how much the landscape has shifted.

This disconnect is glaring: businesses are expected to be more agile than ever, yet the conventional funding sources have become slower and more restrictive.

Quick-approval business loans aren't just a fallback for businesses rejected by the big banks. They're a primary strategic tool for proactive owners who understand that speed and opportunity are more valuable than a drawn-out, bureaucratic process.

Real-World Scenarios Demanding Speed

The need for fast funding cuts across every industry imaginable. Here are a few real-world situations I see all the time:

- Urgent Equipment Replacement: A restaurant's main oven dies in the middle of a dinner rush. A fast loan gets a new one installed overnight, preventing thousands in lost revenue.

- Inventory Opportunities: A supplier offers a huge bulk discount on a best-selling product, but the deal is only good for 48 hours.

- Cash Flow Shortfalls: A logistics company gets hit with a surprise spike in fuel costs and needs to make payroll before their client invoices are paid.

In every one of these scenarios, waiting for a traditional loan would mean taking a direct financial hit. Having access to quick-approval business loans turns these potential disasters into manageable business decisions, allowing you to keep your momentum without missing a beat.

Choosing the Right Fast Funding Option for Your Business

Getting cash in the door quickly is one thing, but making sure it’s the right kind of cash is another. When you're under pressure, it's tempting to grab the first loan that gets approved. That's a mistake I've seen business owners make too often, and it can create more problems than it solves. The key is to match the funding structure to how your business actually operates day-to-day.

Let's look at a real-world example. A popular downtown restaurant sees a huge spike in business during the summer tourist season. For them, a Merchant Cash Advance (MCA) is often a perfect match. They get a lump sum upfront and pay it back with a small percentage of their daily credit card sales. When they're slammed, they pay back more; when things quiet down in the off-season, the payments shrink. The repayment schedule ebbs and flows with their actual cash flow.

Now, consider a completely different business, like a logistics company with a fleet of trucks. Their biggest headache isn't seasonality, but unpredictability—a sudden engine repair or a spike in fuel costs. A Revolving Line of Credit is their lifeline. They can draw funds whenever an unexpected expense pops up and only pay interest on what they’ve used. It's a financial safety net, not a big chunk of debt they don't immediately need.

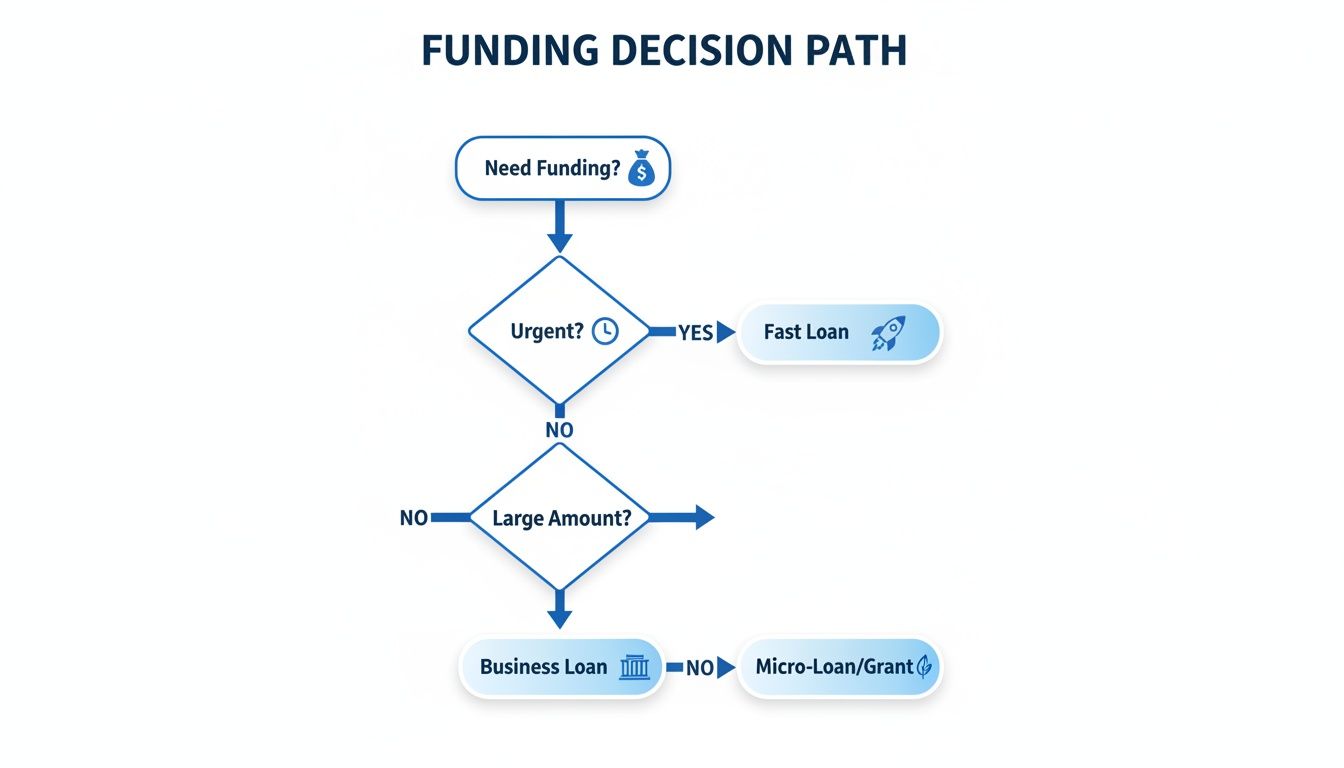

This decision tree gives you a visual for thinking through those initial steps when time is of the essence.

As the chart shows, once you've confirmed the need is urgent, a fast-approval loan is the clear path forward, which brings us back to finding the right fit among the various options.

Aligning Loan Types with Business Scenarios

Beyond MCAs and lines of credit, a few other common products are designed for very specific situations. Knowing when to use them can make all the difference.

A Working Capital Loan is the jack-of-all-trades for covering routine operational costs—think payroll, rent, or buying inventory to get you through a busy period. It's no surprise that this type of unsecured financing is exploding in popularity. The global market for these loans is projected to hit $561.3 billion, with short-term working capital loans accounting for over 39% of that. Businesses need liquidity, and these loans provide it. You can see the full market analysis on Straits Research to get a sense of the scale.

Then you have Equipment Financing. Picture a construction firm that just landed a huge contract but needs another excavator to get the job done on time. This loan is secured by the piece of equipment itself, which makes lenders feel more comfortable. That comfort often translates into faster approvals and better rates because the asset itself is the collateral.

The best funding strategy always starts with a clear-eyed assessment of your specific challenge. Are you trying to smooth out inconsistent revenue? Cover a single large purchase? Or just manage the daily grind of operational costs? Your answer points directly to the right loan.

Making the Strategic Choice

Before you even look at applications, take a minute to ask yourself a few critical questions. Getting this right from the start will save you countless headaches.

- What, exactly, is this money for? "Growing the business" is too vague. "Funding a $15,000 targeted social media campaign for our new spring collection" is a plan. Lenders love a clear plan.

- How does my cash actually come in? If your revenue comes from tons of daily credit card swipes, an MCA makes sense. If you wait weeks for B2B clients to pay their invoices, you should be looking at invoice financing instead.

- What can my cash flow realistically handle for repayment? A daily or weekly debit can cripple a business that gets paid in big, monthly chunks. Be honest about your payment cycles.

Answering these questions will stop you from just taking the first offer that lands in your inbox. It empowers you to find a funding partner that will actually help you build something lasting.

How to Prepare Your Business for a Fast Approval

Getting a quick "yes" from a lender isn't about luck. It's about preparation. When you're chasing after quick approval business loans, the groundwork you lay beforehand makes all the difference. It's about showing up with a clear, compelling financial story that leaves no room for doubt. By getting your documents in order and understanding what underwriters are really looking for, you can sidestep the delays that trip up most applicants.

Think of it less like gathering paperwork and more like building a case for your business. Every document you provide tells part of your story, and you want that story to communicate one thing loud and clear: reliability.

Build Your Digital Document Package

In the world of fast financing, stacks of paper are ancient history. Modern lenders rely on clean, digital documents that can be fed directly into their underwriting systems. This is your first opportunity to accelerate the process. Having an organized digital folder ready to go can easily shave days off your approval time.

I tell my clients to create a "financing go-bag." It's a single folder on their computer with everything a lender might need, ready to be sent at a moment's notice.

Here’s what should be in it:

- Recent Bank Statements (3-6 Months): This is where lenders look first. They're verifying your revenue, checking your cash flow, and looking for consistency. Healthy daily balances and steady deposits go a long way in building trust.

- Business Tax Returns (Last 1-2 Years): These documents give a bird's-eye view of your company's profitability and stability over a longer period.

- Government-Issued Photo ID: A straightforward identity check for all owners with 20% or more of the company.

- Voided Business Check: This simply confirms your bank account details so the funds can be deposited without a hitch once you’re approved.

Articulate a Clear Use of Funds

This is a step most business owners gloss over, but it's incredibly important. Simply writing "working capital" on an application is a red flag for lenders. It sounds vague and unplanned. Instead, you need to show them you have a concrete strategy for how their money will generate a return.

For example, don't just say you need money for "inventory." A much stronger pitch is: "We need $25,000 to secure a bulk purchase of seasonal merchandise from our supplier, which gives us a 15% discount and ensures we're stocked for the holiday rush." See the difference? One is a request; the other is a strategic investment.

A well-defined plan for the funds does more than fill a box on a form. It shows the underwriter you're a serious operator who has thought this through, making their decision to approve you that much easier and faster.

Review Your Business Credit Profile

Before you even think about applying, pull your business credit reports. You can get them from agencies like Dun & Bradstreet or Experian. While many quick-approval lenders are more flexible on credit than traditional banks, a strong profile can still open doors to better rates and an even faster process.

Scan for any errors or old disputes you can clear up. A clean credit profile is an easy win. It shows you’re an organized and responsible borrower—exactly the kind of partner every lender is looking for.

Proven Tactics to Get Your Loan Approved Faster

Having all your ducks in a row is a great start, but it’s the proactive moves you make during the application process that can truly speed things up. When you need a quick business loan, every minute counts. It’s not just about submitting the right documents; it’s about playing the game smart.

Here's a simple trick I’ve seen work wonders: submit your application early in the day, preferably between Monday and Thursday morning. Underwriters are at their desks and ready to work. An application that lands on their screen at 9 AM is far more likely to get reviewed and pushed forward that same day than one submitted at 4 PM on a Friday.

Be Ready to Pounce on Lender Inquiries

The moment you hit "submit," your job isn't done. The lender’s clock starts ticking, and they will almost certainly have follow-up questions or want to clarify a specific transaction they see on your bank statement. How quickly you respond can be the difference between approval today or approval next week.

Turn on your phone and email alerts. If a lender needs one more document, you should be able to send it over in minutes, not hours. Being this responsive shows them you’re organized, serious, and easy to work with—all things that make them feel more confident about funding you.

The fintech revolution has made this even more crucial. Over 50% of small business loans are now sourced through digital platforms, and the global fintech lending market has soared to $590 billion. This is especially true for businesses in construction, e-commerce, and hospitality, where approvals can happen in hours. Your speed matters more than ever. You can dig deeper into the latest business lending trends on Fintech Market.

Pro Tip: Keep your phone handy. When a lender calls, be prepared to give them a confident, two-minute rundown of your business's cash flow and exactly how you plan to use the funds. A clear, concise explanation builds trust and can shave significant time off their internal review.

Partner With an Expert Funding Advisor

Trying to find the right lender on your own is like throwing darts in the dark. There are hundreds of them out there, and each one has a different appetite for risk, favors certain industries, and has its own quirky underwriting rules. This is exactly why working with a funding advisor, like our team at FSE, gives you a massive advantage.

An experienced advisor is more than just an application-filler; they're your advocate. They already have a network of trusted lenders and know exactly who to approach based on your business’s unique situation.

Think about it this way:

- You run a construction company? An advisor knows which lenders understand project-based income and won’t flinch at large, sporadic deposits.

- You own an e-commerce store? They’ll connect you with funders who get inventory financing and aren't spooked by seasonal sales spikes.

Getting it right the first time saves you from the soul-crushing cycle of applying, waiting, and getting rejected by lenders who were never a good fit. A good advisor manages everything from the initial application to negotiating the final terms, making sure you get the best deal without wasting precious time.

The right moves can make your application fly through the system, while a few simple missteps can bring everything to a grinding halt. Here’s a quick look at what separates a fast approval from a frustrating delay.

Approval Timeline Accelerators vs Delays

| Action That Accelerates Approval | Common Mistake That Causes Delays |

|---|---|

| Submitting a complete, error-free application with all required documents uploaded. | Leaving fields blank or providing inconsistent information (e.g., mismatched addresses). |

| Responding to lender emails and phone calls within minutes. | Waiting hours or even a day to reply to requests for more information. |

| Having a clear, concise explanation for how the funds will be used to generate ROI. | Being vague about the purpose of the loan, raising red flags for underwriters. |

| Proactively providing context for unusual transactions or dips in revenue. | Forcing the lender to guess what happened, which often leads to a denial. |

| Working with an advisor who can match you with the right lender from the start. | Applying to multiple random lenders online, triggering credit inquiries and getting stuck. |

Ultimately, a fast and smooth approval process comes down to preparation and communication. By being organized and responsive, you put yourself in the driver's seat.

Common Mistakes to Avoid When You're in a Rush for Funding

When you’re racing to get a business loan approved quickly, it's incredibly tempting to grab the first offer that lands in your inbox. I get it. But moving too fast without doing your homework can turn a quick fix into a long-term headache. Most of the biggest mistakes happen when business owners feel the clock ticking.

Let's walk through the most common traps I've seen clients fall into and, more importantly, how you can sidestep them.

Miscalculating the Real Cost of the Loan

One of the most frequent blunders is getting fixated on the interest rate and completely overlooking the total cost of capital. A loan with a "low" rate can easily be loaded with origination fees, service charges, or prepayment penalties that balloon the actual amount you pay back.

You have to look beyond the advertised rate. The true cost of any loan is best understood through its Annual Percentage Rate (APR), which wraps in all those extra fees and expenses. It’s the only way to get a clear picture.

Some fast-funding options, like a Merchant Cash Advance (MCA), don't even use an interest rate. They use a factor rate. For example, a $50,000 advance with a 1.3 factor rate means your payback is $65,000. If you pay that back in six months, the effective APR can soar into the triple digits. Always, always ask your lender—or a trusted funding advisor—to break down the APR for you. It lets you make a true apples-to-apples comparison.

A lower interest rate doesn't always mean a cheaper loan. Hidden fees and short repayment terms can make one offer far more expensive than another. Your job is to understand the complete financial picture before committing.

Overlooking Your Actual Repayment Ability

A loan that suffocates your daily cash flow isn't a solution—it's just a different kind of crisis. I’ve seen it happen time and again: a business takes on a loan with daily payments that seem tiny on paper, only to find themselves constantly scrambling to make ends meet. This is a nightmare for businesses with seasonal sales cycles or those that rely on project-based invoices.

Before you sign on the dotted line, you need to map out your projected income and expenses for the entire loan term. A realistic cash flow forecast is your best friend here. It will tell you, in no uncertain terms, what you can actually afford to pay back each week or month. This simple exercise can save you from accepting terms that will starve your business of the very working capital it needs to grow.

Borrowing More Than You Genuinely Need

When a lender approves you for more than you asked for, it’s easy to get starry-eyed. The idea of having extra cash "just in case" feels like a smart safety net. In reality, it's a dangerous trap.

Every single dollar you borrow has a cost attached. Taking $75,000 when you only needed $50,000 means you're paying interest and fees on $25,000 of capital that's just sitting there, not generating a return.

Stick to your plan. A precise use-of-funds strategy not only strengthens your application but also keeps you disciplined. Securing a quick business loan should be a strategic move to solve a specific problem, not a free pass to take on debt you don't need.

Answering Your Top Questions About Quick Business Loans

When you're trying to get funded fast, you don't have time for a runaround. It's completely normal to have questions about how the process works, what it means for your credit, and just how quickly you'll actually see the money. Let's clear up some of the most common uncertainties we hear from business owners every day.

Getting straight, practical answers is the best way to move forward with confidence and keep your business on track.

Will Applying Ding My Credit Score?

This is probably the number one question we get, and it’s a valid concern. The good news is that the initial exploration process is designed to be completely risk-free for you.

Most modern lenders and brokers, including our team here at FSE, start with a 'soft credit pull'. Think of it as a preliminary peek at your credit profile that doesn't leave a mark or affect your score. A 'hard pull'—the kind that can temporarily lower your score—only happens after you’ve reviewed your funding offers and decided to officially accept one. This gives you the freedom to see what you qualify for without any penalty.

What Do Lenders Actually Look For?

Forget the rigid, often unattainable standards set by traditional banks. Alternative lenders are much more interested in the current health and real-world performance of your business. While the specifics vary from one lender to another, there are a few common benchmarks that will give you a solid idea of where you stand.

Generally, lenders in our network are looking for businesses with:

- At least one year under your belt: This shows you’ve built a stable operation.

- A minimum of $10,000 in monthly revenue: This proves you have consistent cash flow to manage repayments.

These metrics paint a much more accurate picture of your ability to succeed with a loan than an old credit report ever could.

Here's the key takeaway: Your recent revenue and cash flow patterns often carry more weight than your credit history. This is exactly why many businesses that are turned down by a bank can still get approved for fast funding.

How Fast Is "Fast"? When Does the Money Actually Arrive?

"Quick approval" isn't just a catchy phrase; it's the whole point. The entire system is built for speed.

You can typically fill out a short online application in just a few minutes. From there, it's not uncommon to get a preliminary decision within a few hours. Once you review your options and accept an offer, you'll submit a handful of final documents. The funds are then usually wired directly into your business bank account within 24 to 48 hours. It’s entirely possible to go from application to having cash in hand in just a day or two.

I Was Turned Down by a Bank. Do I Still Have a Shot?

Absolutely. In fact, this is one of the main reasons alternative financing exists. A "no" from a traditional bank is far from the end of your funding journey.

Alternative lenders look at your business through a completely different lens. They place a much higher value on things like your recent bank statements and the consistency of your daily sales. If you can show that your business has healthy, predictable revenue, your chances of getting approved are strong, regardless of what a bank has said in the past.

Ready to find the right funding without the endless waiting? At FSE - Funding Solution Experts, our advisors are on standby to connect you with the perfect lender from our network of over 50 partners. You can start a no-obligation application today and get a decision in hours.