There's nothing quite like the dread of watching an old oven die in the middle of a Friday night dinner rush. It's a moment every restaurant owner fears—service grinds to a halt, your kitchen crew is stressed, and hungry customers start walking out the door. That's precisely where smart restaurant equipment financing steps in, turning a potential disaster into a strategic upgrade. It’s how you get the tools you need without wiping out your cash reserves.

Equip Your Restaurant for Growth with Smart Financing

It’s easy to think of financing as just another form of debt, but that’s the wrong way to look at it. Think of it as an investment in your restaurant's future—its efficiency, its capacity, and ultimately, its profitability. This is a specific type of funding designed to get everything from a new walk-in freezer to a top-of-the-line combi oven into your kitchen.

By spreading the cost out over time, you keep your working capital free for the daily essentials, like making payroll and ordering inventory. For most independent restaurants, this kind of financing is the only practical way to bridge the gap between struggling with outdated gear and achieving real, sustainable growth. It's a direct path to upgrading the tools that make you money, especially when big banks, with all their red tape and slow "no's," just aren't an option.

Why Financing Is More Than Just a Loan

This isn't just about getting a check to buy a new machine. It's about what that new machine does for your business. Upgrading your equipment is about unlocking new potential and streamlining your entire operation.

- Boost Your Productivity: Imagine a new, high-powered dishwasher that cuts cycle times in half. That’s fewer labor hours spent on dishes and more clean plates ready for the pass during your busiest hours.

- Expand Your Menu: That modern convection oven or smoker you've been eyeing? It opens the door to menu items you could never execute consistently before, giving you a fresh way to attract new customers.

- Lower Your Operating Costs: Newer, energy-efficient refrigeration and cooking equipment can make a real dent in your monthly utility bills. That savings goes straight to your bottom line.

This push for better equipment isn't just happening on your block; it's a worldwide trend. The global restaurant equipment market is expected to jump from USD 4.8 billion in 2025 to USD 10.2 billion by 2035, a clear sign that successful operators everywhere are investing in smarter, more efficient kitchen technology. You can dig into more of this data in the global restaurant equipment market report from Future Market Insights.

In an industry this competitive, the right equipment gives you an operational edge. Financing it the right way gives you a financial one, letting you grow without strangling your cash flow.

At the end of the day, restaurant equipment financing gives you the power to make critical investments exactly when you need to. Whether you're opening your doors for the first time, expanding your dining room, or just replacing that freezer on its last legs, having access to flexible funding provides the agility you need to thrive. Let’s walk through how to navigate the options and make the right call for your business.

Comparing Your Financing Options

Figuring out financing can feel like trying to follow a complicated recipe in another language. But don't worry—it really just boils down to a few key choices, each with its own unique flavor. Once you get a handle on the main differences, you can pick the restaurant equipment financing option that perfectly fits what your business needs.

The most important thing is to think past just getting the money. You need to consider how each option will affect your cash flow, whether you'll own the gear, and what it means for your restaurant's financial health down the road. Let's break down the most common paths restaurant owners take.

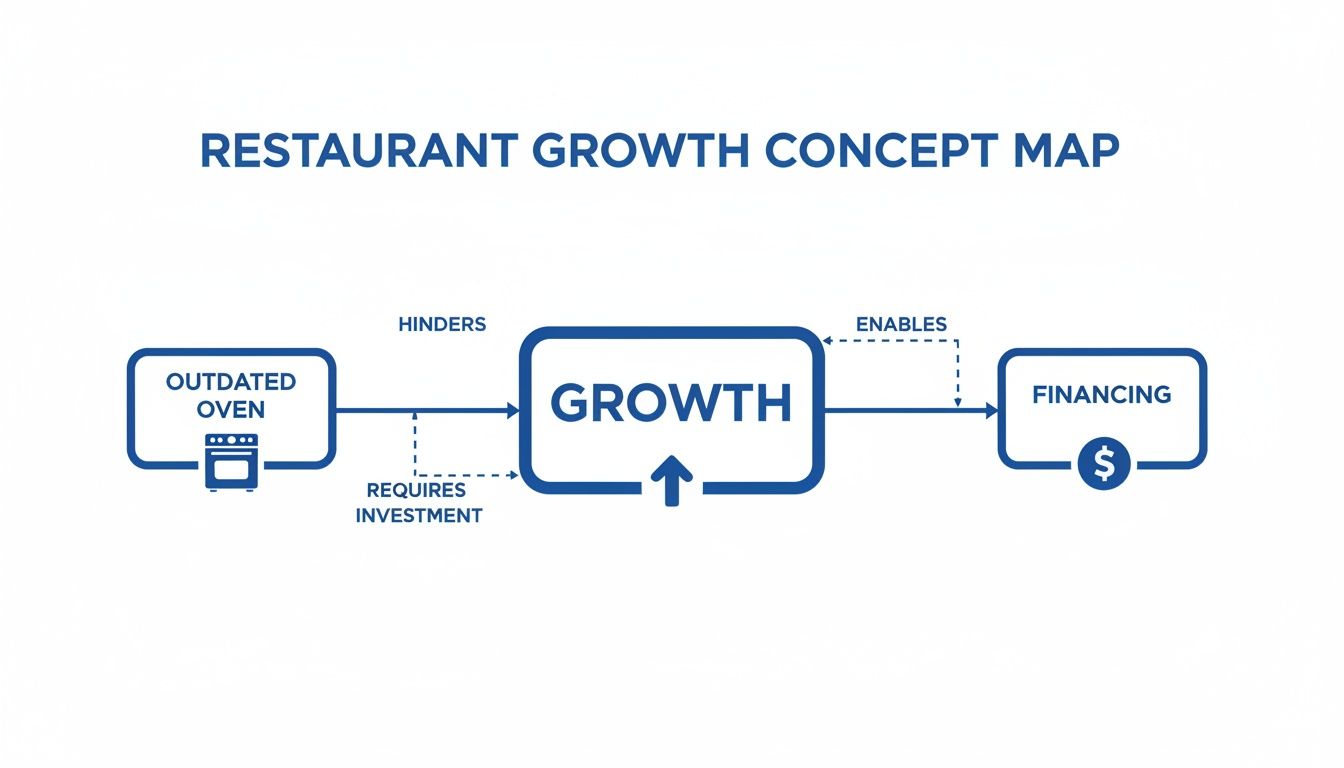

This visual really captures the journey from being stuck with old equipment to unlocking new growth through smart financing.

As you can see, financing is the bridge that turns a problem—like a worn-out oven—into a real opportunity for boosting your revenue and expanding your business.

To help you sort through it all, here's a quick side-by-side look at the most popular financing methods.

Comparing Restaurant Equipment Financing Methods

| Financing Type | Best For | Ownership | Typical Approval Speed | Credit Impact |

|---|---|---|---|---|

| Equipment Loan | Long-term, foundational equipment you want to own outright (e.g., ovens, walk-ins). | You own the equipment after the final payment. | 2-10 business days | Builds business credit; may require a hard credit pull. |

| Equipment Lease | Technology that becomes outdated quickly (POS systems) or preserving cash flow. | Lender owns the equipment; you have a purchase option at the end. | 24-72 hours | Can build business credit; often easier to qualify for than loans. |

| SBA Loan | Major expansions or large equipment packages for established businesses with good credit. | You own the equipment. | Several weeks to months | Builds strong business credit; intensive application. |

| Merchant Cash Advance | Emergency replacements when speed is critical and traditional financing isn't an option. | Not applicable; it's an advance on future sales, not an asset loan. | 24-48 hours | Doesn't typically report to business credit bureaus. |

| Business Line of Credit | Ongoing, flexible access to funds for repairs, small purchases, and unexpected needs. | You own any equipment purchased with the funds. | Varies; 1-2 weeks for initial setup | Can build business credit; usage impacts credit utilization. |

Now that you've seen the high-level comparison, let's dig into the details of what makes each of these options tick.

Equipment Loans: The Path to Ownership

An equipment loan is the most classic route. It works just like a car loan: you borrow money to buy a specific piece of equipment, make regular payments for a set period, and once you’ve paid it all off, it's yours. Simple as that. The equipment you buy also acts as the collateral for the loan.

This is the go-to choice for foundational pieces you’ll be using for years—think a heavy-duty walk-in cooler or a workhorse commercial range. Since you own it, you can also take advantage of tax breaks like the Section 179 deduction, which can make a big dent in the total cost of your investment.

Equipment Leases: The Flexible Rental Model

An equipment lease is more like renting an apartment than buying a house. You make smaller, regular payments to use the equipment for a set amount of time. When the lease term is up, you usually have a few choices:

- Give it back: This is a great move for technology that gets outdated fast, like your POS system.

- Renew the lease: If the equipment is still working great for you, you can simply extend the agreement.

- Buy it out: Many leases give you the option to purchase the equipment, often for a fair market value or a pre-set price.

Leasing is a fantastic strategy when you need to hang onto your cash, since it almost always requires less money upfront than a loan. It’s also perfect for specialty items you might only need for a seasonal menu, like a top-of-the-line soft-serve machine for the summer months.

SBA Loans: The Government-Backed Powerhouse

Don't let the name fool you—the Small Business Administration (SBA) doesn't lend you the money directly. Instead, the SBA guarantees a large chunk of the loan for a bank or other lender, which makes them much more willing to lend to small businesses. In return, you often get fantastic terms, like lower interest rates and longer repayment periods.

The trade-off? A much tougher application process and a longer wait for approval. An SBA loan is an excellent choice for an established restaurant with a solid credit history that's planning a major expansion or buying a whole suite of expensive equipment.

Merchant Cash Advances: The Fast-Cash Solution

A Merchant Cash Advance (MCA) isn’t really a loan at all. A provider gives you a lump sum of cash right now in exchange for a slice of your future credit and debit card sales. Repayments happen automatically, with a small percentage taken from your daily or weekly sales until the advance is paid back.

This option is incredibly fast, with funds often hitting your account in just 24 to 48 hours. It’s the perfect fix for emergencies—like when your main fryer gives up the ghost right before a holiday weekend—and you need cash yesterday.

That speed and convenience come at a price, though. MCAs use a "factor rate" that is almost always more expensive than the interest rate on a traditional loan. They are a powerful tool for short-term, urgent needs but aren't meant for long-term financing.

Business Lines of Credit: The Revolving Safety Net

A business line of credit is basically a credit card for your restaurant. You get approved for a certain credit limit, and you can pull money from it whenever you need to, paying interest only on what you’ve actually used. Once you pay it back, your full credit limit is available again.

This gives you incredible flexibility. You could use it to cover an unexpected dishwasher repair one month and then buy a new prep table the next. A line of credit is the ideal financial safety net, giving you immediate access to capital to jump on opportunities or handle emergencies without having to apply for a new loan every single time.

What Lenders Look For in Your Application

When you apply for restaurant equipment financing, you’re not just filling out forms—you're telling your restaurant's financial story. Lenders, from big banks to specialized funders, are all trying to answer one core question: "Is this business a good bet to pay us back?" To figure that out, they zero in on a handful of key indicators that show just how healthy and stable your operation really is.

Think of your application package as a professional pitch for your restaurant. Every document, every number helps the lender see your track record and your potential for future growth. Getting your ducks in a row before you even start the conversation can make a world of difference, speeding up approvals and landing you much better terms.

The Three Core Pillars of Approval

While every lender has its own secret sauce for underwriting, their decisions almost always boil down to three fundamental areas. These pillars give them a quick, reliable snapshot of your restaurant's viability.

- Time in Business: This is all about stability. A restaurant that’s been open for two or more years has proven it can handle the ups and downs and keep customers coming back. A newer business is more of an unknown, which naturally translates to higher risk in a lender’s eyes.

- Monthly Revenue: Cash flow is king in this business, and lenders know it. They need to see strong, consistent revenue that can comfortably cover the new payment. Expect them to ask for your last three to six months of bank statements to see the real numbers.

- Credit Score: Your personal and business credit scores are both on the table. A solid credit history is your proof that you know how to manage debt responsibly. You don't need a perfect score, but a higher one will almost always unlock better interest rates and more favorable terms.

Key Documents You Will Need

To back up the claims in your application, you'll need to provide some specific paperwork. Having these documents organized and ready to go will make the whole process feel less like a headache and more like a smooth transaction. It's like having your mise en place ready before the dinner rush—it just makes everything work better.

- Bank Statements: Lenders will want to see your last 3-6 months of business bank statements. This is how they verify your revenue claims and get a feel for your cash flow patterns.

- Tax Returns: Your most recent business and personal tax returns give a wider view of your restaurant's financial health and profitability over time.

- Equipment Quote: You'll need an official quote from your vendor. This document spells out exactly what you're buying and how much it costs, so the lender knows precisely where their money is going.

In today's climate of inflation and staff shortages, getting financing is often non-negotiable for U.S. hospitality businesses. The problem? Traditional banks often shut the door on promising startups with just one year in business and $10,000 in monthly revenue. This is where financing brokers have become so critical, connecting restaurants to networks of over 50 lenders who can often approve equipment leases in just 24-48 hours. Since 2018, these alternative routes have provided over $500 million in funding to more than 1,500 businesses, filling a huge gap left by conventional banking. You can find more details on how alternative financing is changing the game at Peppr.com.

A complete and organized application sends a powerful message. It tells a lender you're a serious, professional operator who has a firm grasp on your finances. That alone builds the confidence needed to get to a faster "yes."

At the end of the day, your goal is to present a clear, verifiable case that your restaurant is a sound investment. By understanding what lenders care about and preparing your documents ahead of time, you put your business in the best possible position to get the equipment you need to grow.

Calculating the True Cost of Your Equipment

That shiny new walk-in cooler or high-capacity oven has a sticker price, but that’s just the starting point. To make a smart financial decision for your restaurant, you have to look beyond the initial price tag and understand the total cost of ownership. This means getting into the weeds of any restaurant equipment financing agreement to see how every fee and percentage point will hit your bottom line.

Think of it like buying a car. You wouldn't just look at the MSRP; you'd ask about the interest rate, loan term, and any dealer fees buried in the contract. The same exact principle applies here. The goal is to see the complete financial picture, not just the upfront cost of the gear itself.

Unpacking the Key Cost Components

There are a few key terms that really determine the true cost of your financing. Getting a handle on these will give you the power to compare offers accurately and avoid any nasty surprises down the road.

- Interest Rate: This is the lender's charge for borrowing the money, plain and simple. A lower interest rate means a lower overall cost.

- Factor Rate: You'll see this with Merchant Cash Advances. It's a multiplier (like 1.3) applied to the loan amount to calculate your total repayment. The key difference? It doesn’t shrink as you pay down the balance.

- Origination Fees: This is a one-time fee some lenders charge just for processing the loan. It's usually a small percentage of the total loan.

- Down Payment: Some deals require you to pay a slice of the equipment's cost upfront. This lowers your loan amount, but it also means you need more cash on hand right now.

All these pieces work together to set your monthly payment and, more importantly, the total amount you'll pay back. A tiny difference in an interest rate or a single origination fee can easily add up to thousands of dollars over the life of the agreement.

A Real-World Example

Let's put this into practice. Imagine you need to finance a $25,000 walk-in cooler to get through the busy summer season. You get two different offers on the table.

Offer A: A Traditional Loan

- Loan Amount: $25,000

- Interest Rate: 8%

- Term: 60 months (5 years)

- Monthly Payment: Roughly $507

- Total Repayment: $30,420

- Total Cost of Financing: $5,420

Offer B: An MCA with a Factor Rate

- Advance Amount: $25,000

- Factor Rate: 1.35

- Term: 12 months

- Total Repayment: $33,750 (calculated as $25,000 x 1.35)

- Total Cost of Financing: $8,750

As you can see, the MCA might get cash in your hand faster, but its total cost is dramatically higher. This is exactly why you have to compare the total repayment amount to understand the true price of your financing.

The best financing deal isn't always the one with the lowest monthly payment. It's the one that costs you the least amount of money over the entire term of the agreement.

Leveraging Tax Benefits to Your Advantage

Now for the good news. One of the best tools for chipping away at the net cost of your equipment is the Section 179 deduction. This IRS tax code lets businesses deduct the full purchase price of qualifying equipment from their gross income in the year it’s put into service.

So, instead of slowly depreciating the asset over several years, you could write off the entire $25,000 for that walk-in cooler on this year's taxes. For a restaurant in a 25% tax bracket, that could mean a tax savings of $6,250.

This move effectively lowers the net cost of the cooler to just $18,750 (before you even factor in financing costs). It’s a powerful strategy that can turn a necessary expense into a savvy financial play that boosts your cash flow and accelerates your return on investment.

How to Choose the Right Financing Partner

Getting approved for restaurant equipment financing is only half the job. Finding the right partner to work with is just as critical to your success.

Who you choose to do business with—be it a traditional bank, an online lender, or a finance broker—will shape everything that comes next. Their process, their transparency, and the support they offer can make or break your experience. Think of this partner as a key supplier for your restaurant's financial health. The wrong one can easily spoil the whole dish.

This decision directly impacts how fast you get funded, how clear your terms are, and what kind of support you have when questions pop up. A great partner acts as a guide through the sometimes-murky waters of financing. A poor one can leave you feeling lost, confused, and locked into a bad deal.

Direct Lenders vs. Financing Brokers

Your first fork in the road is deciding who to apply with. You can go straight to the source of the money or work with an expert who can shop around for you.

Direct Lenders (Banks and Online Lenders): Applying directly means you’re working with a single institution. This can be straightforward, but it's a bit like only visiting one car dealership—you only see their inventory and their pricing. You won’t know if a better offer is right down the street unless you fill out another application and start the process all over again.

Financing Brokers (Like FSE - Funding Solution Experts): A good broker works for you. They take your single application and present it to a whole network of lenders they have relationships with. It’s like having a personal shopper who visits every dealership in town to find the best car at the best price, saving you a ton of time and legwork. They bring multiple competitive offers back to the table for you to compare.

Key Criteria for Evaluating Partners

As you start comparing your options, keep these three critical areas in mind. They’ll help you make a sound decision for your restaurant's future.

Speed and Efficiency: How fast can they get things done? In the restaurant business, opportunities—and emergencies—don't wait. A partner who can turn around approvals and funding in 24-48 hours gives you a massive advantage over one that takes weeks to make a decision.

Transparency and Honesty: Are the terms crystal clear? A trustworthy partner will take the time to walk you through every detail of the agreement, from interest rates to the total cost of repayment. If anyone uses confusing jargon or seems to be rushing you through the paperwork, that’s a major red flag.

Customer Support and Expertise: Do they actually get the restaurant industry? The best partners have deep experience in our world. They understand your cash flow cycles, your specific equipment needs, and the unique pressures you’re under. That expertise allows them to offer much more relevant advice and solutions.

Choosing a partner is a long-term decision. You want an ally who is invested in your growth, not just in closing a one-time transaction. A good financing partner helps you secure the capital you need to thrive.

In a tough market, smart financing is a powerful competitive advantage. With chain restaurants seeing spending dips of -3.4% and independents down -1.4%, strategic operators are using equipment financing to expand and upgrade while others pull back. This trend is fueling growth in the commercial foodservice equipment market, which is projected to jump from $33.28 billion in 2024 to $35.0 billion in 2025.

By working with the right partner, you can get the fast, flexible funding needed to join success stories like Chili's, which saw a massive 31.6% sales surge after a major kitchen overhaul. You can find more insights in the Bank of America restaurant industry report.

Common Questions About Restaurant Equipment Financing

As you get serious about upgrading your kitchen, you're bound to have some questions. It's only natural. Getting straight answers is the best way to feel confident about moving forward.

Let's walk through some of the most common questions we hear from restaurant owners just like you.

Can I Finance Used Restaurant Equipment?

Yes, absolutely. Most lenders are happy to finance used or refurbished equipment, which can be a brilliant move for your budget. There’s just one main condition: you have to buy it from a recognized dealer or vendor, not just a private seller you found online.

The process for financing used gear is pretty much the same as for new. The lender will just need to see an official invoice from the seller. This confirms the price and shows them they’re investing in a solid piece of equipment that will last. It’s a great way to get a top-tier brand in your kitchen for a fraction of the cost.

How Quickly Can I Get Funding?

This is where alternative lenders and brokers really shine. A traditional bank loan can drag on for weeks, sometimes even months. But specialized financing partners move a lot faster.

In many cases, you can get a preliminary decision on your application within 24 hours. Once you're approved and all your paperwork is in, the funds can be in your account in as little as 24 to 48 hours. When a critical piece of equipment goes down, that kind of speed is a lifesaver.

What If I Have Bad Credit?

Don't assume a low credit score means you're out of the game. While great credit always helps you get the best rates, it's not the only thing lenders look at. They're often more interested in the overall health of your business.

Factors like how long you've been in business and, most importantly, your monthly revenue carry a lot of weight. If you can show a history of strong, steady sales, many lenders will be ready to work with you. You may see a slightly higher interest rate, but financing is still very much on the table.

Ready to get the equipment your restaurant needs to thrive? The dedicated advisors at FSE - Funding Solution Experts can match you with the best financing options from a network of over 50 lenders, getting you fast approvals and expert guidance. Apply in minutes and find your funding solution today.