When your business needs cash now, waiting weeks for a bank to make a decision simply isn’t an option. Short-term small business loans are designed to fill this exact gap, acting as a financial bridge to get you from a pressing need to a profitable outcome.

Think of it less as a last resort and more as a strategic tool. It's the funding you use to cross a temporary cash flow crunch, jump on a surprise opportunity, or handle an unexpected expense without derailing your operations. Unlike the slow, rigid process of a traditional bank, these loans are all about speed and flexibility.

Unlocking Growth with Fast, Flexible Funding

Let's say your main delivery van breaks down right before a busy season. Or maybe a supplier offers you a massive, can't-miss discount on inventory—but only if you can pay in full this week. In these real-world scenarios, time is money, and short term small business loans are built for these moments.

What makes them so different is how they're structured. Lenders in this space can often get funds into your account in just 24 to 48 hours. They care more about your recent business performance—like your monthly revenue and cash flow—than a flawless, years-long credit history. This practical approach opens the door to funding for many small and mid-sized businesses that might not fit the banks' narrow criteria.

The Core Difference: Speed and Simplicity

At its heart, the biggest split between a short-term loan and a conventional bank loan comes down to the timeline. Getting a traditional loan is a marathon, filled with mountains of paperwork, multiple layers of approval, and a long, drawn-out wait. Short-term loans are the sprinters of the finance world, engineered to get you the capital you need in days, not months.

This need for speed is a huge driver of their popularity. These loans took the top spot in the unsecured lending market in 2023, and the segment is forecast to grow by an incredible USD 4,023.4 billion by 2029. This explosive growth shows just how critical this type of funding has become for businesses everywhere. For a deeper dive, you can explore more data on this market growth to see the full picture.

In essence, a short-term loan trades a longer repayment period for immediate access to capital. It’s a calculated decision to solve a pressing problem or capture a fleeting opportunity today, rather than waiting for a slower, more rigid funding source.

The best uses for this type of financing are situations with a clear and quick return on investment. A construction firm might grab a short-term loan to buy materials and start a profitable new job right away. A local shop could use the funds to load up on inventory just before a big holiday rush, ensuring they don’t miss out on sales.

To put it all in perspective, here’s a straightforward look at how these two funding paths stack up against each other.

Short Term Loans vs. Traditional Bank Loans At a Glance

This table offers a quick comparison of the key features separating fast short-term financing from conventional bank loans.

| Feature | Short Term Small Business Loans | Traditional Bank Loans |

|---|---|---|

| Funding Speed | Typically 24-72 hours | Weeks or even months |

| Loan Term | 3 to 18 months | 3 to 10+ years |

| Application Process | Simple online forms, minimal documents | Extensive paperwork, business plans |

| Approval Basis | Primarily business revenue & cash flow | Strict credit scores, collateral, history |

| Ideal Use Case | Inventory, cash flow gaps, emergencies | Major expansion, real estate purchase |

As you can see, they are fundamentally different tools designed for completely different jobs. One is built for agility and immediate needs, while the other is meant for long-term, foundational investments.

What Are My Options for Fast Business Funding?

When you’re in a pinch and need cash fast, it’s easy to lump all quick funding options into one bucket. But in reality, the world of short-term small business loans is more like a specialized toolkit. You wouldn't use a sledgehammer for a finishing nail, and you shouldn't use the wrong funding product for your specific business need.

Getting familiar with how each one works is crucial. The way you get the money, pay it back, and handle the costs can either feel like a perfectly tailored solution or a constant headache. Let's break down the three most common types so you can see which tool is right for the job.

1. Short-Term Loans

A short-term loan is the most classic option of the bunch. Think of it as a condensed version of a traditional bank loan—you get a lump sum of cash upfront and pay it back with interest over a set period, usually somewhere between three to 18 months.

The payments are typically fixed and automatic, pulled from your business bank account either daily or weekly. That predictability is its biggest strength, making it ideal for a one-off investment where you know exactly what the return will be.

- Best For: Making a single, large purchase with a clear purpose, like buying new equipment, stocking up on inventory for a big order, or funding a targeted marketing campaign.

- Repayment: Fixed, predictable payments withdrawn automatically on a daily or weekly schedule.

- Real-World Example: A local construction company lands a big contract but needs a new excavator to get it done. They take out a $30,000 short-term loan, buy the machine, and start the project immediately. The new revenue from the job easily covers the fixed weekly loan payments.

2. Merchant Cash Advances (MCAs)

Here’s where things get a little different. A Merchant Cash Advance (MCA) isn't technically a loan at all. It's an advance on your future sales. A provider gives you a lump sum of cash, and in return, they get a small, fixed percentage of your future credit and debit card sales until the advance is paid back.

This is a game-changer for businesses with high card sales volumes, like retail shops or restaurants. Your repayment is directly tied to your daily revenue. When business is booming, you pay back more; when things are slow, you pay back less. This built-in flexibility is a huge cash flow protector.

A Merchant Cash Advance moves in lockstep with your business. It’s a funding solution that breathes with your revenue rhythm, making it a powerful ally for navigating seasonal rushes or seizing unexpected opportunities.

- Best For: Businesses where sales can swing wildly from day to day, such as restaurants, cafes, and retail stores.

- Repayment: A fixed percentage of your daily credit card sales is automatically sent to the funder. No manual payments needed.

- Real-World Example: A restaurant owner needs $15,000 for high-end ingredients and extra staff to handle the holiday rush. She gets an MCA. As holiday sales pour in, a small slice of each card transaction goes toward repayment. After the holidays, when sales return to a normal pace, the repayment amount naturally drops with them.

3. Business Lines of Credit

A business line of credit is your financial safety net. Instead of getting a single chunk of cash, you're approved for a credit limit—a pool of funds you can dip into whenever you need to. The best part? You only pay interest on the money you actually draw, not the whole amount.

It's the perfect tool for managing the unpredictable ups and downs of running a business, not for a single big purchase. Once you repay what you've used, the full credit line becomes available again, ready for the next time without a new application.

- Best For: Juggling uneven cash flow, covering payroll during a slow month, or handling surprise equipment repairs.

- Repayment: You typically make monthly payments based only on your outstanding balance.

- Real-World Example: A small consulting agency has a $50,000 line of credit. One month, a major client payment is late, but payroll is due. They draw $20,000 to make sure everyone gets paid. The next month, the client pays up, and the agency repays the $20,000 plus interest. Just like that, their full $50,000 safety net is back in place for whatever comes next.

Understanding the True Cost of Your Loan

Figuring out the real cost of a short-term business loan can feel like you're trying to solve a puzzle. It's about more than just the interest rate. To really get a handle on what you'll owe, you need to look past the sticker price, especially since many of these loans don't use a traditional Annual Percentage Rate (APR).

Instead, you'll often come across something called a factor rate. This is a much simpler way to think about cost. It’s a straightforward multiplier that tells you the total amount you’ll repay from day one, fees and all. No complex interest calculations, just a clear, predictable number.

Let's say you borrow $10,000 with a 1.25 factor rate. The math is simple: $10,000 x 1.25 = $12,500. That means the total cost of borrowing is a flat $2,500. This kind of clarity is incredibly helpful for budgeting because you know the exact cost before you commit.

From Factor Rate to APR

The simplicity of a factor rate is great, but it makes it tricky to compare your offer against other options, like a business credit card or a traditional bank loan that uses APR. APR shows you the cost of borrowing over a full year, so learning how to translate a factor rate into a comparable APR is a crucial step for making a smart decision.

You can do a rough calculation to get a ballpark APR. While it's not a perfect science, it gives you a solid benchmark to see how different financing products stack up against each other.

Key Takeaway: A factor rate gives you a simple, upfront total repayment amount. But to truly compare its cost against other types of financing, you have to convert it into a representative APR.

This quick conversion often reveals that a loan with a what seems like a low factor rate can actually have a very high effective APR, especially if the repayment period is just a few months. This is exactly why comparing offers based on APR is non-negotiable.

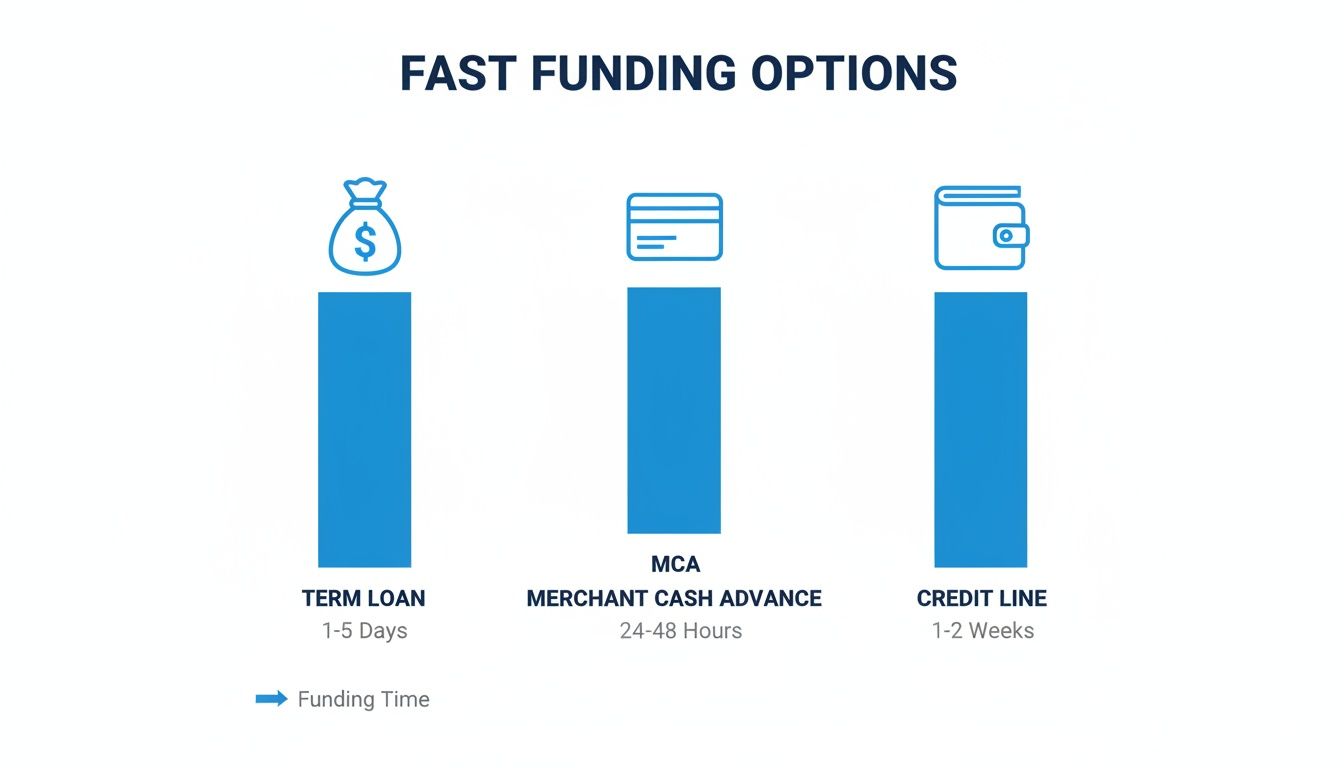

The chart below shows how quickly different types of short-term funding can be accessed, a factor that often plays a big role in their overall cost structures.

As you can see, options like a Merchant Cash Advance are typically the fastest, and that speed can be reflected in the total cost of the capital.

Uncovering Additional Fees

The main interest or factor rate is just one piece of the puzzle. A handful of other fees can creep in and bump up the total cost of your short term small business loan. Knowing what to look for helps you avoid any nasty surprises down the road.

Keep an eye out for these common fees:

- Origination Fees: Think of this as a processing fee. The lender charges it for setting up the loan, and it’s usually a percentage of the total loan amount, often taken right out of the funds you receive.

- Underwriting Fees: Very similar to origination fees, these cover the lender’s costs for doing their homework—vetting your application and your business's financial health.

- Late Payment Fees: This one is straightforward. If you miss a payment deadline, you'll almost certainly face a penalty. These can pile up fast and significantly drive up your borrowing costs.

Always make it a point to ask your lender for a complete, itemized list of every single fee. A good, transparent lender will have no problem laying everything out for you. This empowers you to compare offers based not just on the rate, but on the true, all-in cost of the money.

Knowing When to Use a Short Term Loan

When it comes to business financing, timing is everything. A short term small business loan isn't some all-purpose fix; it's a specific tool for moments when speed and opportunity collide. The real magic happens when you understand exactly how to use its main advantage—incredibly fast funding—to get a leg up on the competition in a way that slower, traditional financing just can't.

Think of it as your strategic ace in the hole. The whole point is to use quick cash to solve a problem or jump on a chance that will bring in an even quicker return. This isn't money for long-shot projects. It’s for tackling urgent needs or grabbing profitable, time-sensitive deals that will pay for the loan and then some.

The Best Use Cases for Fast Capital

The best time to reach for a short-term loan is almost always when it will directly generate immediate revenue or stop a costly operational hiccup in its tracks. If the potential gain from acting right now is much greater than the cost of the loan, then it becomes a seriously powerful tool.

Here are a few real-world situations where that speed is a game-changer:

Seizing a Deep Discount: Imagine you own a trucking company and stumble upon a perfectly maintained used tractor for 40% below market value. The catch? The seller needs cash now and has other buyers lining up. By getting a short-term loan approved in 24 hours, you can snatch up that truck before anyone else does, adding a revenue-generating machine to your fleet on the spot. A traditional bank loan would take weeks, and that truck would be long gone.

Prepping for a Sales Surge: An e-commerce shop is gearing up for a massive flash sale, and projections show it could triple its usual monthly revenue. To pull it off, the owner needs to buy an extra $25,000 in inventory. A short-term loan provides the cash to stock up, making sure they don't sell out and leave thousands in sales on the table. The profits from that sale can then turn around and pay off the loan.

Starting a Profitable Job Immediately: A contractor lands a big commercial renovation project. The only problem is they need to front $40,000 for materials before the client’s first payment comes in. Waiting on a bank would mean delaying the start date and possibly breaching the contract. Fast financing lets them buy supplies, get to work on time, and build a great relationship with a high-value new client.

In every one of these scenarios, the slow pace of traditional financing would have meant a huge missed opportunity or a direct hit to the bottom line.

Recognizing the Risks of Misuse

As powerful as these loans are, they come with real risks if you use them for the wrong reasons. The most common pitfall is using short-term, higher-cost financing for long-term projects that have no clear path to making money quickly. That mismatch can crush your cash flow and put your business in a precarious position.

A short term small business loan is a bridge, not a foundation. It's designed to get you across a temporary gap or to a specific, profitable destination quickly. Using it to build the entire road is a recipe for financial trouble.

For example, taking out a 12-month loan to pay for a five-year office expansion is a textbook mistake. The loan payments will be due long before that new office space starts bringing in any revenue, putting a ton of pressure on your day-to-day operations. Likewise, using a fast loan to cover chronic payroll shortfalls without fixing the root cause is just delaying the inevitable.

This is why having a clear picture of the financial landscape is so important. The U.S. Small Business Administration (SBA) itself has seen a growing need for smaller, quicker loans. In fiscal year 2025, the SBA backed a record $44.8 billion across 84,400 loans. Interestingly, more than half of its flagship 7(a) loans were for amounts under $150,000—the perfect size for the kinds of cash flow gaps and inventory needs that businesses in retail, construction, and logistics face all the time. You can explore the full details of this small business funding trend to see just how these needs are shifting. Smart borrowing means making sure the loan’s term and purpose line up with a clear, fast return on your investment.

A Practical Checklist for Your Loan Application

So, what’s the secret to getting a short-term small business loan funded in as little as 24 hours? It's not magic—it's preparation. Lenders need to see a clear, organized picture of your business's health, and having your documents ready to go is the fastest way to get them what they need. A prepared application eliminates delays and shows you’re a serious, on-the-ball business owner.

We can break down the entire journey into four simple stages, from the first conversation to the moment the funds land in your account. Following this roadmap makes the process much smoother and significantly boosts your odds of a fast approval.

Stage 1: The Initial Inquiry and Eligibility Check

Before diving into a full application, the first move is to make sure you meet the lender’s basic criteria. Most modern lenders care more about your recent performance than a perfect credit score, but they still have minimums.

Knowing these upfront will save you a ton of time and effort. For most lenders in the fast-funding space, the typical baseline looks something like this:

- Minimum Time in Business: Most will want to see at least one year of operating history.

- Monthly Revenue: A consistent $10,000 or more per month is a common benchmark to show you have steady cash flow.

- Business Bank Account: You’ll need a dedicated business bank account to receive the funds and set up repayments.

Stage 2: Getting Your Documents in Order

Once you've confirmed you're a good fit, it's time to gather your paperwork. This is where good preparation really shines. Your goal is to hand the lender a complete, easy-to-understand package that gives them a clear snapshot of your business's financial activity.

A clean, complete, and promptly submitted document package is the single biggest factor in speeding up your funding time. From our experience, the number one cause of delays is incomplete or blurry paperwork.

The list of required documents is usually quite simple. Lenders just need to verify who you are, that your business is legitimate, and see your revenue firsthand.

Having these documents ready will make the application process fast and smooth. Here’s a quick rundown of what you’ll almost always need to provide.

Essential Documents for Your Loan Application

| Document Type | Purpose | Pro Tip |

|---|---|---|

| Government-Issued Photo ID | To verify the identity of the business owner(s). | A clear, unexpired driver’s license or passport works perfectly. Make sure all four corners are visible in your photo or scan. |

| Voided Business Check | To confirm your business bank account details for funding and repayment. | This helps prevent any errors when transferring funds. A bank letter with your account and routing numbers also works. |

| Recent Bank Statements | To analyze your business’s cash flow, revenue, and overall financial health. | Be prepared to provide the last three to six months of statements. Downloading digital PDFs from your online banking portal gives you the best quality. |

| Business Registration | To confirm that your business is a legitimate, registered entity. | This could be your Articles of Incorporation, LLC operating agreement, or a business license, depending on how your business is structured. |

With these documents in hand, you're ready for the final steps.

Stage 3: Offer Review and Acceptance

After you submit everything, the lender’s underwriting team gets to work. If you're approved, they'll send over a loan offer that details the loan amount, term, factor rate or interest, and your repayment schedule. It’s critical to review this document carefully so you understand the total cost and all the terms before you sign.

Stage 4: Funding!

This last part is the quickest. Once you sign the loan agreement, the lender will wire the funds directly to your business bank account. When you've prepared everything ahead of time, this entire process—from your first call to getting funded—can happen in as little as 24 to 48 hours.

How a Broker Simplifies Your Search for Capital

Trying to find the right short-term business loan on your own can feel like navigating a maze blindfolded. There are hundreds of lenders out there, and each one has its own unique rules, rates, and ideal customer. Applying to them one by one isn't just exhausting—it's a massive waste of your valuable time.

This is exactly where a finance brokerage becomes your most powerful tool.

Think of a broker as a financial matchmaker for your business. Instead of you spending hours filling out dozens of different applications, you complete just one simple, universal application with us. We then take that single application and present it to a wide, curated network of lenders, which instantly multiplies your chances of finding the perfect funding partner.

Your Advocate in the Lending World

A brokerage like FSE gives you a serious advantage over going it alone. We start by taking the time to actually understand your business—what makes it tick, your industry, your cash flow patterns, and where you want to go. Armed with that knowledge, we can strategically connect you with lenders who are specifically looking to fund businesses just like yours.

This expert guidance spares you the frustration of wasting time on lenders who were never a good fit to begin with. You’ll work with a dedicated funding advisor who personally analyzes and compares every offer, breaking down the complex jargon into plain English so you can make a truly informed and confident decision.

A brokerage transforms a confusing, time-consuming search into a clear, efficient process. It’s about more than just access to capital; it’s about getting the right capital on the best possible terms, with an expert in your corner.

Let's look at a real-world example. Imagine a trucking company owner who needs cash—fast—for an unexpected engine repair. His bank turns him down because of a recent dip in revenue. Instead of hitting a dead end, he works with FSE. His advisor takes his single application to our network of over 50 lenders and quickly secures three competitive offers from partners specializing in the logistics industry. Within 24 hours, the funds are in his account, and his truck is back on the road.

Gaining a Competitive Edge with Speed

In business, speed is everything. The traditional loan process is notoriously slow. In fact, research shows lenders often spend up to 70% more time processing SBA loans, which is why so many business owners are forced to look for faster alternatives. A brokerage delivers that critical speed, often securing decisions within 24 hours.

By connecting U.S. businesses with our extensive partner network, we've funded over $500M for more than 1,500 clients since 2018. You can learn more about how the market is shifting by reading up on the state of small business lending in 2025.

Working with a brokerage doesn't just make your search easier; it gives you leverage. When lenders in our network know they are competing for your business, you're in a much better position to get better rates and more favorable terms than you could ever find on your own. It’s simply the smarter, faster way to get the funding your business needs to thrive.

Frequently Asked Questions

When you're looking into short-term small business loans, it's natural for questions to pop up. Let's tackle some of the most common ones we hear from business owners so you can move forward with confidence.

Think of this as a quick-reference guide to reinforce what you've learned and clarify the practical side of getting fast capital.

How Quickly Can I Get Funded?

Speed is the name of the game here. Forget the weeks or even months you might wait for a traditional bank loan; this process is built for business owners who need to act now.

If you have your documents in order, you can often go from application to approval in just a few hours. For many businesses, that means seeing the funds hit their bank account within 24 to 48 hours. This incredible speed is exactly why these loans are so effective for jumping on unexpected opportunities or solving sudden cash flow gaps.

Will a Low Credit Score Disqualify Me?

Not necessarily, and that’s a big deal. Many business owners with less-than-perfect credit don't even bother applying, assuming they won't qualify. But alternative lenders see things differently.

While good credit never hurts, they're often more interested in the real-time health of your business. They’ll look closely at your recent monthly revenue and how consistently cash flows through your accounts. If you can show strong, reliable sales, that often carries more weight than an old credit score.

Key Insight: For many alternative lenders, your business's current performance is the best predictor of your ability to repay. They're backing your present success, not just your financial past.

Is There a Penalty for Paying My Loan Early?

This is a fantastic question, and you absolutely need to ask it before signing anything. The answer really depends on the lender and the type of loan.

Some financing, especially products that use a factor rate, have a fixed payback amount. In those cases, paying early won't save you any money because the total cost was set from day one. Other products, like some term loans or lines of credit, don't have prepayment penalties. Always get the specifics on the lender's early payment policy upfront.

Can I Get a Short-Term Loan if My Business Is New?

This can be tough for true startups. Most lenders want to see some kind of track record—usually a minimum of six months to a full year in business.

Why? Because that history gives them the data they need to feel comfortable. It shows them your revenue is stable and your cash flow is predictable, which makes lending to you far less of a risk. Businesses without at least a year of operations under their belt will find it challenging to qualify for most short-term small business loans.

Ready to stop guessing and start exploring your real funding options? The dedicated advisors at FSE - Funding Solution Experts can help you navigate our network of 50+ lenders to find the fast, flexible capital your business needs. Apply in minutes and get a decision in as little as 24 hours at https://www.fseb2b.com.