When you're trying to meet small business loan requirements, it really comes down to one thing: proving your business is healthy and reliable. Lenders are looking at your financial history, cash flow, credit, and time in business to answer a single question: can you successfully pay back the loan?

Understanding What Lenders Really Want

Trying to get a business loan can feel like you're trying to solve a complex puzzle, but what lenders are looking for is actually pretty simple. They're looking for confidence. They need to feel confident that your business is stable, well-managed, and capable of taking on new debt without crumbling.

To build that confidence, they don't just guess. Lenders use a structured, time-tested framework to evaluate your application and get the full picture of your company's health. Think of it as their internal scorecard for your business.

The Five C's of Credit

The most common framework you'll encounter is the "Five C's of Credit." These aren't rigid, black-and-white rules. Instead, they're guiding principles that help a lender size up the risk and potential of your loan application. Knowing them helps you see your business through their eyes.

- Character: This is all about your track record and reputation. Lenders will pull your personal and business credit history to see how you've handled debt in the past. Are you reliable? Do you pay your bills on time?

- Capacity: This is your raw ability to repay the loan. They'll dive into your cash flow statements, revenue, and existing debt to make sure you can comfortably handle another monthly payment.

- Capital: Lenders want to see you have some skin in the game. Capital is the money you've personally invested in the business, and it shows them you're committed to its success.

- Collateral: These are hard assets—like equipment, inventory, or real estate—that you pledge to secure the loan. For the lender, collateral is a safety net that reduces their risk if you default.

- Conditions: This covers the bigger picture. What’s the purpose of the loan? How much do you need? What are the current economic conditions for your industry? They want to ensure the money will be used for something productive that makes your business stronger.

To make this even clearer, let's break down how these concepts look in the real world.

The Five C's of Credit at a Glance

| The 'C' | What It Means for Lenders | How You Demonstrate It |

|---|---|---|

| Character | "Can I trust you to pay me back?" | A solid personal credit score (680+), clean business credit report, and a history of on-time payments. |

| Capacity | "Does your business generate enough cash to afford this loan?" | Strong, consistent revenue, positive cash flow, and a low debt-to-income ratio. Bank statements are key here. |

| Capital | "How much of your own money is at risk?" | A healthy owner's equity stake on your balance sheet, or evidence of a significant down payment. |

| Collateral | "What can I recover if you can't repay the loan?" | Appraisals for real estate, invoices for accounts receivable, or a list of valuable equipment you own outright. |

| Conditions | "Does this loan make sense for your business and the economy?" | A clear business plan detailing how the funds will be used for growth, like buying a new machine or expanding your location. |

Thinking about your business through this lens helps you anticipate a lender's questions and get ahead of any potential concerns.

By viewing your business through the lens of the Five C's, you can anticipate a lender's questions and proactively address potential concerns. It shifts the dynamic from simply asking for money to presenting a compelling case for investment in your company's future.

Navigating all these requirements can be tough, especially since every lender weighs these factors a little differently. This is where an expert guide, like a brokerage, becomes a game-changer. They already know which lenders prioritize strong cash flow over a perfect credit score, or which ones specialize in your specific industry. That inside knowledge gets you matched with the right lender from the start, which dramatically boosts your chances of getting the capital you need to grow.

Choosing the Right Place to Apply

Meeting small business loan requirements isn't just about what's on your application—it’s about where you send it. This is one of the most overlooked secrets to getting funded. A denial from one lender doesn't mean your business is a lost cause; it often just means you haven’t found the right lending partner.

Think of it like applying to colleges. A big national bank is like an Ivy League school with incredibly strict, standardized criteria. On the other hand, a local community bank or an online lender is more like a state university—still selective, but with more flexible and diverse standards for acceptance. Your job is to find the institution that’s the best match for your business's unique profile.

The Approval Rate Gap

The difference between these lending channels isn't just a hunch; the data backs it up. One of the biggest unwritten “requirements” is simply being among the small pool of applicants that get a "yes." Federal Reserve data shows that large banks fully approve only around 44% of small businesses that apply for any amount of financing.

But here’s where it gets interesting. The Fed’s Small Business Credit Survey reveals that applicants at small banks have a better shot, with an approval rate of about 54%. That gap widens even more with alternative lenders and nonbank finance companies, which can approve roughly 75% of applicants in some capacity. You can dig deeper into these lending statistics on CreditSuite.com.

This math is a huge deal for owners who can't afford to waste months waiting for an answer. If only 44 out of 100 applicants get approved at big banks, while 50 to 75 find success elsewhere, then “meeting the requirements” is really a game of choosing the right field to play on.

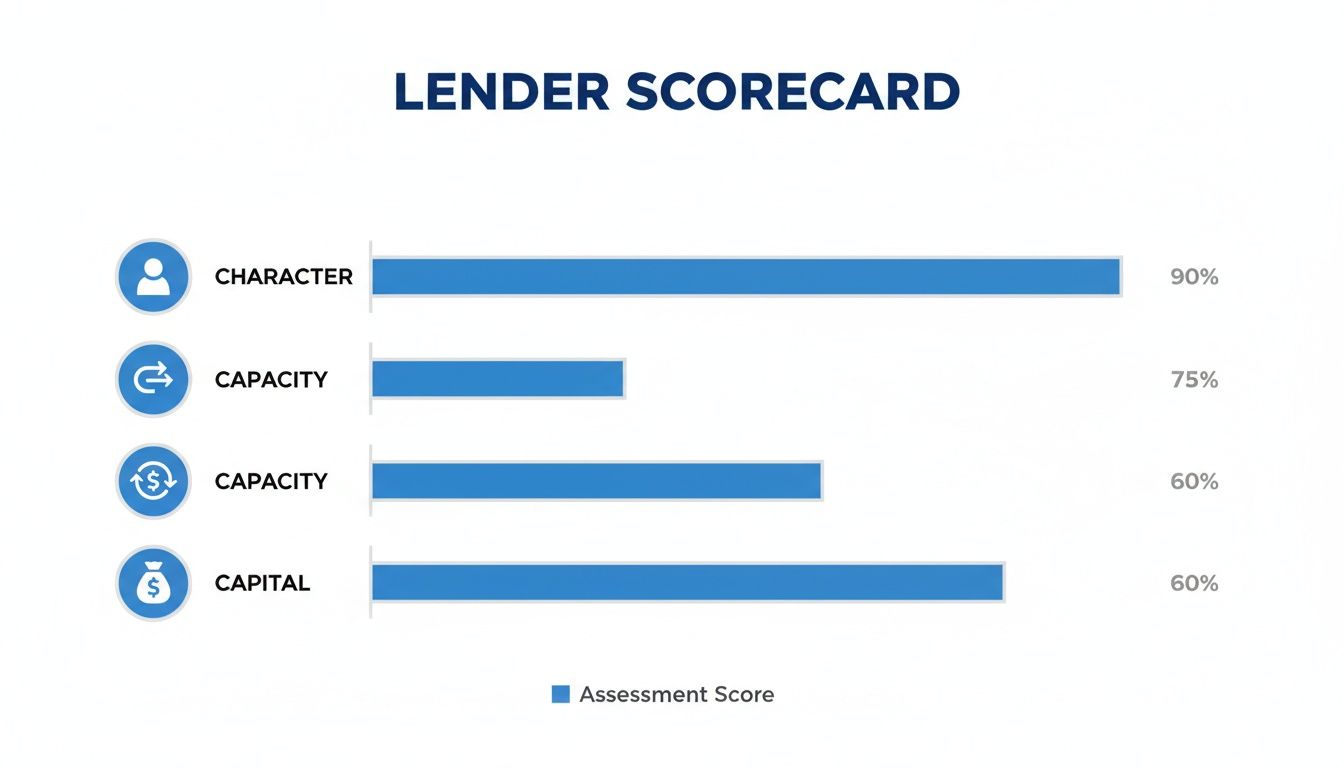

The chart below shows the core areas every lender looks at, though how much they care about each one can vary dramatically.

This illustrates how lenders balance Character (your credit history), Capacity (your cash flow), and Capital (your own investment in the business). A large bank might give all three heavy weight. An alternative lender, however, might focus almost exclusively on your recent cash flow—your Capacity—and not worry as much about the other two.

Finding the Right Lender Fit

Once you understand this, everything changes. A rejection letter isn't a final judgment on your business's health. It’s simply a signal that there was a mismatch between your profile and that lender’s rigid underwriting box. The good news? Your business might be a perfect fit for someone else.

This is exactly why working with a funding expert or a brokerage can be a game-changer. Instead of blindly applying and collecting rejections, an advisor can pre-match your business with institutions actively looking for applicants just like you.

A loan denial often says more about the lender's rigid criteria than it does about your business's potential. The key is to connect with a lending partner who understands and values your specific strengths.

This strategic approach saves you precious time, protects your credit score from the damage of multiple hard inquiries, and dramatically boosts your odds of approval. By targeting lenders whose requirements align with what your business does best—whether that’s strong daily sales, valuable equipment, or consistent monthly revenue—you stop playing a game of chance and start executing a winning strategy.

Decoding the Financial Health Lenders Look For

When a lender looks at your loan application, they aren't just seeing numbers on a page. They're reading the financial story of your business—its past performance, its current stability, and its potential for future growth. Understanding what they're looking for is the single most important step in preparing a successful application.

These metrics aren't just arbitrary hoops to jump through. Think of them as the vital signs a doctor checks. Each one tells a lender something specific about your business's health and its ability to handle—and repay—new debt.

Key Financial Metrics Under the Microscope

While every lender has its own specific underwriting formula, a few core metrics always take center stage. These are the main characters in your business's financial narrative.

Annual and Monthly Revenue: This is the big-picture number that shows your business is active and generating sales. Lenders want to see a consistent, predictable revenue stream because it proves there's a real market for what you do. For many alternative lenders, a good starting point is seeing $10,000+ in consistent monthly revenue.

Cash Flow: If revenue is what you earn, cash flow is what you actually have in the bank. This is arguably the most critical number for most lenders. Positive cash flow demonstrates that you have the liquid cash to cover daily operations and make your loan payments on time, every time.

Time in Business: This isn't just a date on a certificate; it’s proof of your resilience. A business that's been operating for one year or more has shown it can navigate market ups and downs and has built a real operational track record.

Personal and Business Credit Scores: Your credit history acts as a report card for your financial reliability. Lenders review it to see how you've managed debt in the past. You don't need a perfect score, but a score above 650 generally unlocks more—and better—loan options.

Lender Expectations Are Getting Tougher

The lending environment has changed. In the background, requirements for financial strength have quietly tightened, especially at traditional banks. This has reshaped who gets approved and for how much. According to the Federal Reserve’s Senior Loan Officer Opinion Survey, banks are reporting stricter collateral requirements and lower credit limits for small businesses.

For example, a trucking company that might have easily secured a $250,000 line of credit against its receivables a few years ago might now only be offered $150,000 and be asked to pledge additional equipment to secure the loan. The survey also revealed that 72% of banks list a borrower's financials as the number one reason for denying a loan—ranking it higher than both credit history and collateral. You can find more detail on these trends in reports from the Kansas City Fed.

This shift means that consistent revenue, positive bank balances, and manageable existing debt are no longer just "nice-to-haves"—they're the new table stakes for getting competitive loan offers. Lenders are putting a much higher premium on businesses with strong cash flow and a clean credit profile.

This heightened scrutiny makes a solid financial foundation non-negotiable. It's less about hitting one specific number and more about presenting a complete picture of stability and smart financial management.

Understanding the Minimums and Ranges

It’s important to remember that these numbers are guidelines, not unbreakable laws. Lenders look at the whole picture. A business with slightly lower revenue but exceptionally strong, consistent cash flow might be a much more attractive borrower than a high-revenue company with razor-thin margins and volatile bank balances.

Here’s a general idea of what different types of lenders are looking for:

| Metric | Traditional Banks | Alternative Lenders |

|---|---|---|

| Minimum Credit Score | Typically 680+ | Often 550-600+ |

| Time in Business | Usually 2+ years | 6 months - 1+ year |

| Annual Revenue | $250,000+ | $100,000+ ($10k/month) |

| Key Focus | Credit, Collateral, Profitability | Cash Flow, Recent Revenue |

This is precisely where working with a skilled funding advisor can make all the difference. An expert can analyze your complete financial profile and match you with lenders whose specific criteria align with your business’s unique strengths. They know how to position your company so that what might seem like a weakness to one lender is a non-issue for another.

Matching Your Needs to the Right Loan Type

Not all business goals are the same, so it's no surprise that not all loans are created equal. The specific type of financing you're going after will directly shape the requirements you'll need to meet. This is a crucial point—lining up your business's strengths with the right loan can be the difference between a quick approval and a frustrating dead end.

Think of it like choosing the right tool for a job. You wouldn’t grab a hammer to saw a piece of wood. In the same way, applying for a loan that doesn't fit your financial profile or how you plan to use the money is a recipe for wasted time and effort. Each loan product is built with a specific purpose and risk profile in mind.

How Different Loan Products Change the Rules

Lenders look at risk through different lenses depending on the loan’s structure. An unsecured term loan, for example, is all about your business's overall financial health. For that, your credit score and consistent profitability are everything. On the other hand, financing that's secured by a physical asset—like a piece of heavy machinery—shifts the lender's focus from your history to the asset's value.

Here's a practical look at how this plays out with a few common loan types:

Term Loans: Perfect for big, one-time investments like a major expansion. These usually have the toughest requirements, demanding strong credit, a few years in business, and a full set of financial statements.

Lines of Credit: The go-to for managing day-to-day cash flow. Here, lenders care most about consistent revenue and a solid credit history to feel confident you can draw and repay funds as needed.

Equipment Financing: Used specifically to buy machinery, vehicles, or other equipment. The asset you're buying acts as its own collateral, so lenders are more interested in its value than a flawless credit score. This often makes it one of the more accessible financing options.

Merchant Cash Advances (MCAs): Designed for businesses with high volumes of credit and debit card sales. Qualification is almost entirely based on your daily sales receipts, making it a super-fast option for businesses that might struggle to meet traditional loan criteria.

To help clarify which product aligns with different business situations, let's compare them side-by-side.

Loan Requirements by Product Type

This table offers a comparative look at the primary qualification factors for different types of business financing. It's designed to help you see which product might be the best fit for your company's current needs and financial standing.

| Loan Product | Primary Requirement Focus | Typical Use Case |

|---|---|---|

| Term Loan | Credit Score, Profitability, Time in Business | Large, one-time investments (e.g., expansion, acquisition) |

| Line of Credit | Consistent Revenue, Credit History | Managing cash flow, unexpected expenses |

| Equipment Loan | Value of the Asset, Down Payment | Purchasing new or used machinery and vehicles |

| Merchant Cash Advance | Daily Credit/Debit Card Sales Volume | Quick access to capital for inventory or emergencies |

As you can see, the "best" loan truly depends on what a lender is looking for and what your business can prove.

The Rise of Flexible and Specialized Financing

The world of business funding has grown far beyond the traditional bank loan. Government-backed programs and alternative online lenders have completely changed the game, creating new paths to capital for businesses of all shapes and sizes. For instance, the SBA's 7(a) loan program has seen a boom in smaller loans under $150,000, opening doors for younger companies that don't fit the classic big-bank profile.

At the same time, online lenders have built products that value speed and recent performance over years of history. This has created a clear divide: medium- and high-risk businesses are now far more likely to work with online lenders because they can often get approved in just 24-48 hours. This market shift gives business owners who might not pass a bank's strict review a real, though sometimes more expensive, path to getting the funds they need. You can dive deeper into these modern lending trends on Ampac.com.

The key takeaway is that your business doesn’t need to be perfect to get funded. It just needs to be a good match for the right product. A knowledgeable partner can analyze your strengths and direct you to the lender who values what you bring to the table.

This strategic matchmaking is where a funding expert really shines. Instead of you having to become an overnight expert on dozens of different loan products, an advisor can quickly spot the best fit. They might see that your strong daily sales make you a perfect candidate for an MCA, or that the value of the truck you want to buy makes equipment financing a slam dunk. It's all about turning a potential rejection into a funding success story.

Your Essential Document Checklist for a Smooth Application

Nothing slows down a loan application like missing paperwork. To a lender, a disorganized application isn't just an administrative headache; it can be a red flag that hints at poor business management. Getting your documents in order before you apply is more than just good preparation—it’s about presenting your business as a professional, organized, and low-risk partner.

This checklist breaks down the core paperwork you'll need and, more importantly, why each piece matters.

Think of it like building a case for your business's future success. Each document is a piece of evidence. Together, they tell a powerful story about your financial stability and growth potential.

Business Legal and Identity Documents

First things first, lenders need to verify that your business is a legitimate, legally registered entity. These documents prove your company's identity and confirm that you have the authority to borrow money on its behalf.

- Government-Issued ID: A simple driver's license or passport for any owner with a 20% or more stake in the business. This is basic identity verification.

- Business Licenses and Registrations: These prove you're operating above board and are compliant with local, state, and industry regulations.

- Articles of Incorporation/Organization: This is the official document that created your LLC or corporation. It’s essentially your business’s birth certificate.

- Voided Business Check: A simple way to provide the lender with your correct account and routing numbers so they know exactly where to send the funds once you're approved.

Business Financial Health Documents

Next, you'll need the documents that paint a clear picture of your company's financial performance. This is the part where you prove you can handle the loan payments.

- Recent Business Bank Statements: For many modern lenders, the last 3-6 months of bank statements are the single most important document. They provide a real-time, unfiltered look at your daily cash flow—what's coming in, what's going out. It's often more revealing than a year-old tax return.

- Business Tax Returns: Lenders will typically ask for the last 1-2 years of returns to see a consistent history of profitability and verify you're up-to-date with the IRS.

- Financial Statements: This trio—your Profit & Loss (P&L) statement, balance sheet, and cash flow statement—offers a structured, big-picture view of your company's financial health.

Having these documents ready to go can radically speed up the entire process. When underwriters have a complete, organized file, they can make decisions with confidence, often moving from application to funding in as little as 24 hours.

The good news is that working with modern funding partners is a far cry from the mountains of paperwork demanded by traditional banks. While a bank might ask for a 50-page business plan and detailed financial projections, many alternative lenders can give you a decision based on just your application and recent bank statements.

This streamlined approach saves you an incredible amount of time and gets you back to focusing on what you do best—running your business.

How to Strengthen Your Loan Application

Knowing what lenders want is one thing. Actually taking steps to become the applicant they can't turn down is another. This is where you move from just meeting the bare minimums to building a truly compelling case for your business.

Think of it like getting your house ready to sell. You wouldn't just hope a buyer sees its potential through the clutter. You'd clean, stage it, and highlight its best features. Preparing your loan application is no different—it's all about presenting your business in the best possible light.

Clean Up Your Financial House

First things first: get your financial records in order. This is probably the single most important action you can take. To a lender, messy books are a massive red flag. They scream disorganization and make it nearly impossible to gauge the true health of your company.

Imagine the difference. A business with jumbled spreadsheets and missing bank statements looks like a gamble. But that same business, presented with clean Profit & Loss statements and a clear balance sheet from professional accounting software, suddenly looks like a well-managed operation.

Here’s a quick checklist to get you started:

- Get on Accounting Software: If you're still using spreadsheets, now's the time to switch. Tools like QuickBooks or Xero are the industry standard and can generate lender-ready reports in minutes.

- Reconcile Your Accounts: Make it a monthly habit to ensure your books match your bank statements to the penny. This simple discipline demonstrates you have a tight grip on your finances.

- Separate Business and Personal: Still running business expenses through your personal checking account? Stop. Open a dedicated business bank account immediately. Commingling funds makes your true cash flow a mystery to underwriters.

Boost Your Credit and Tell a Compelling Story

With your financials looking sharp, it's time to focus on your credit and the story behind the numbers. Your credit scores directly influence the interest rates and terms you'll be offered, while a solid business plan gives the lender context and confidence.

Start by pulling your personal and business credit reports. Check for errors and see where you can make quick improvements. Often, simply paying down a high-balance credit card or two can give your score a nice little bump. And, of course, make sure every single bill is paid on time.

A strong business plan does more than just ask for money; it articulates a clear vision for growth. It shows a lender exactly how their capital will be used to generate a return, turning the loan from a risk into a strategic investment.

Finally, craft a clear, one-page summary of your funding request. Don't just ask for money—explain why you need it and how it will help you grow. Are you buying a new piece of equipment to take on bigger jobs? Launching a marketing campaign to reach new customers? This narrative helps the underwriter see you have a real plan for success.

Working with an advisor at a company like FSE - Funding Solution Experts can be a huge help here. They can spot weaknesses you might miss and connect you with lenders who understand your vision, not just your history.

Your Top Questions About Loan Requirements, Answered

Even with all the information laid out, a few specific questions always seem to pop up right when you’re ready to apply. It’s completely normal. Let’s tackle some of the most common ones we hear from business owners, so you can move forward with total confidence.

Can I Really Get a Business Loan with Bad Personal Credit?

Absolutely. While a traditional bank might fixate on your personal credit score, the lending world has changed. Many modern funding partners are far more interested in the actual health of your business—things like consistent revenue and healthy cash flow.

It helps to know that certain loan products are built for this exact situation.

- Equipment financing, for example, is secured by the equipment itself, which acts as collateral.

- A merchant cash advance is based on your future credit card sales, not your past credit history.

In both cases, the lender's risk is lower because there's built-in security. You might see a slightly higher interest rate to offset a lower credit score, but it's rarely a deal-breaker for getting the funding you need to grow.

What’s the Magic Revenue Number to Qualify?

This is probably the number one question we get, and the truth is, it varies wildly. A big national bank might not look at you unless you’re pulling in hundreds of thousands in annual revenue. But that's not the whole story.

For most of the lenders we work with, the focus isn't on massive annual figures. Instead, they look for consistent monthly income. A solid benchmark to aim for is $10,000 or more in monthly deposits over the last three to six months.

Remember, consistency trumps a one-time sales spike. Lenders want to see a reliable pattern that proves your business can handle its operating costs and, most importantly, a new loan payment.

If I Could Only Provide One Document, What Would It Be?

Hands down, for nearly every non-bank lender out there, your recent business bank statements are the most crucial document you can provide. Tax returns are great for showing last year's performance, but bank statements give a real-time, unfiltered look at your company's financial heartbeat.

Underwriters can see your daily revenue, expenses, cash reserves, and average balance at a glance. This transparency is what allows them to make fast, accurate decisions—and it’s the reason many can get you funded in as little as 24 hours.

Navigating all these details is much easier when you have an expert in your corner. The team at FSE - Funding Solution Experts is here to evaluate your specific situation and match you with the lender that makes the most sense for your goals. Start your no-obligation application today.