When you need funding for your business, the first thing you might think of is putting up collateral—like your office building or company vehicles. But what if you don't have those kinds of assets, or you'd rather not risk them? That's where an unsecured business loan comes in.

It’s a type of financing that doesn't require any physical collateral. Instead of looking at what you own, lenders focus on your business's financial strength, primarily its cash flow and credit history. This makes it a fantastic option for getting capital quickly to fuel growth or manage day-to-day operations.

What Are Unsecured Business Loans and How They Work

Picture this: a huge, game-changing contract lands on your desk, but you need cash now to buy materials and scale up your team. Or maybe a supplier offers a massive discount on inventory, but the deal is only good for 48 hours. Pledging your property for a traditional loan would take weeks. This is the exact moment an unsecured business loan becomes your most powerful tool.

Unlike secured loans that are "backed" by tangible assets, an unsecured loan is fundamentally built on trust and your business's track record. The lender's perspective shifts entirely. They're not asking, "What can we take if you default?" Instead, they're asking, "How strong is this business, and what is its capacity to repay the loan from its ongoing operations?"

The Core Concept: Performance Over Pledges

The easiest way to grasp the difference is to think about it this way: a secured loan is like a pawn shop transaction. You hand over a valuable item (your collateral) to get cash. If you don't pay back the loan, the shop keeps your item. The lender's risk is low because they're holding an asset that covers the debt.

An unsecured business loan, on the other hand, is more like a savvy investor backing a promising company. They aren't focused on physical assets. Their decision is based on a deep dive into your business's potential, its leadership, and its proven ability to generate consistent revenue. The strength of the business is the security.

For lenders offering this type of funding, a few key metrics tell the whole story:

- Consistent Cash Flow: Your bank statements need to show a reliable stream of income. This proves you have the money coming in to make regular payments.

- Credit History: Both your business and personal credit scores tell a story of how responsibly you've handled debt in the past.

- Time in Business: A longer operational history demonstrates stability and reassures lenders that you can navigate market ups and downs.

Unsecured vs Secured Business Loans at a Glance

To make the distinction crystal clear, let's break down the key differences side-by-side.

| Feature | Unsecured Business Loans | Secured Business Loans |

|---|---|---|

| Collateral | Not required. Based on business performance. | Required (e.g., property, equipment, inventory). |

| Risk to Lender | Higher, as there's no asset to seize. | Lower, as collateral mitigates potential loss. |

| Interest Rates | Typically higher to compensate for risk. | Typically lower due to reduced lender risk. |

| Approval Speed | Fast. Often within 24-48 hours. | Slower. Can take weeks due to asset valuation. |

| Loan Amounts | Generally smaller loan amounts. | Can be much larger, based on collateral value. |

| Best For | Asset-light businesses, quick opportunities. | Businesses with significant assets, large capital needs. |

This table shows the trade-offs: unsecured loans offer speed and flexibility at a potentially higher cost, while secured loans provide lower rates in exchange for collateral and a longer application process.

A Growing Market for Agile Businesses

This "performance-first" lending model has exploded in popularity, especially among small and mid-sized enterprises (SMEs) that are rich in revenue but light on assets. The global market for unsecured business loans hit USD 261.6 billion, with significant growth on the horizon.

This trend is directly tied to the powerhouse role of SMEs, which numbered 358 million worldwide in 2023. In the U.S. alone, where North America holds 37% of the global market share, the 33.3 million SMEs that form 99.9% of all businesses are driving the demand for this kind of nimble financing. You can dig deeper into these unsecured business loan market trends to see the full picture.

Key Takeaway: Unsecured loans are designed to evaluate your business's ability to generate cash, not the value of its physical property. This makes them a perfect match for service-based companies, software startups, and any business whose greatest asset is its operational strength.

By sidestepping the need for property appraisals or vehicle title searches, lenders can approve and fund these loans incredibly quickly. The timeline shrinks from weeks or months down to just a couple of days, empowering you to act on opportunities the moment they appear.

The Key Qualifiers for Getting Approved

When you apply for an unsecured business loan, the whole dynamic changes. Since there's no equipment or property on the line, lenders aren't sizing up your assets. Instead, they’re digging deep into one fundamental question: is your business healthy enough to make the payments?

To get their answer, they essentially give your company a full financial physical. They’re looking at key performance indicators that tell them you’re built to last. It’s less of a rigid checklist and more of a holistic look at your revenue, operating history, and credit profile.

The Power of Consistent Cash Flow

More than anything else, lenders want to see strong, predictable revenue. It’s the lifeblood of your company and, frankly, it’s how you’ll pay them back. A steady, reliable income stream tells them your business is on solid ground.

They aren't easily wowed by a single blockbuster month. A business bringing in a consistent $20,000 every month for a year is a much safer bet than one that had a massive $100,000 month followed by a few that were barely scraping by. Consistency is king because it proves you know how to manage your cash flow.

Most lenders will have a minimum monthly revenue requirement, often starting around $10,000, just to get your foot in the door.

A lender's review of your bank statements is like watching a film of your business's financial activity. They're looking for a steady plot of regular deposits and responsible spending, not a story with dramatic, unpredictable peaks and valleys.

Proving Your Stability with Time in Business

Right alongside revenue is your track record—your time in business. A company that’s been around for a few years has proven it can handle market shifts, keep customers happy, and manage its finances for the long haul. A brand-new startup just doesn't have that history.

Every year you’ve been in operation builds your case. Lenders have different benchmarks for how long you need to have been open, but here are some common minimums:

- At least 6 months: This might get you approved with some flexible, short-term lenders.

- 1-2 years: A standard requirement for many alternative lenders offering term loans or lines of credit.

- 3+ years: This signals a well-established business and can open the door to larger loan amounts and better terms.

A longer history tells the lender that your business model works and you've made it past the volatile make-or-break stage. You've built a foundation, and that de-risks their investment in you.

Understanding Your Credit Profile

Finally, lenders will look at your credit—both your business credit and, in most cases, your personal credit score. You don't need a perfect score to get an unsecured loan, but your credit report tells the story of how you've handled debt before. It's a powerful indicator of your financial discipline.

They’re scanning for major red flags like recent bankruptcies, tax liens, or a pattern of late payments. A clean credit profile, on the other hand, shows you’re reliable and meet your obligations, which gives lenders a huge boost of confidence. While many modern lenders are more flexible on credit scores than traditional banks, a higher score will almost always help you lock in better rates and terms.

Finding the Right Unsecured Funding for Your Goals

Deciding you need an unsecured loan is the first step. The next, more crucial step is figuring out which type of funding is the right fit. After all, you wouldn't use a hammer to saw wood, and the same principle applies here—the right financial tool depends entirely on the job at hand.

Instead of getting bogged down in technical definitions, let's look at how these financial tools solve real-world business problems. By connecting each option to a common scenario, you’ll get a much clearer picture of which one can best fuel your growth, smooth out cash flow, or help you jump on an unexpected opportunity.

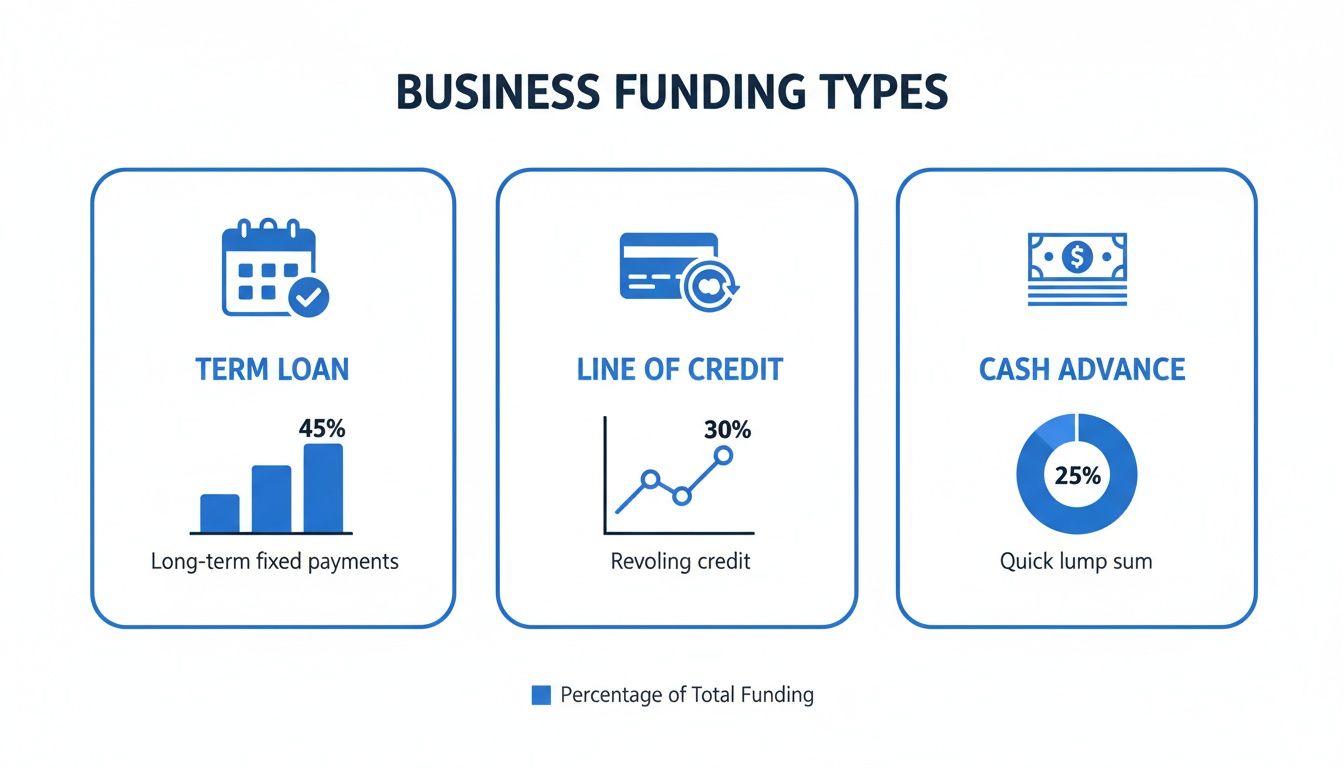

Unsecured Term Loans: The One-Time Growth Catalyst

Think of a term loan as a single, targeted injection of capital. You get a lump sum of cash upfront to fund a specific, planned project and then pay it back over a set period with predictable monthly payments. This straightforward structure is perfect for big, one-off investments where you can clearly map out the return.

For instance, a successful landscaping company wants to upgrade its entire fleet of commercial mowers. The owner calculates that the new equipment will boost efficiency by 25%, allowing them to take on more contracts immediately. An unsecured term loan provides the exact amount needed for the purchase, and the fixed payments are easy to build right into their operating budget.

A term loan is purpose-built for a singular, defined objective. It’s like building a financial bridge to get from Point A (where you are now) to Point B (your growth goal).

Unsecured Lines of Credit: The Flexible Cash Flow Buffer

A business line of credit works less like a one-time cash infusion and more like a financial safety net. It’s a revolving credit limit you can draw from whenever you need it, repay, and then draw from again. The best part? You only pay interest on the funds you’re actually using, which makes it an incredibly versatile tool for managing day-to-day expenses and navigating those inevitable cash flow gaps.

Picture a retail boutique gearing up for the holiday season. The owner needs to buy a lot of inventory months in advance but won’t see the revenue from those sales until December. A line of credit lets them stock the shelves, cover payroll during the slow buildup, and then pay down the balance once the holiday rush kicks in. It’s an ideal solution for managing the peaks and valleys of a seasonal business.

Merchant Cash Advances: The Revenue-Based Accelerator

A merchant cash advance (MCA) isn't a loan in the traditional sense. Instead, it’s an advance on your future earnings. A provider gives you a lump sum of cash in exchange for a percentage of your future credit and debit card sales. Repayment happens automatically as a small slice of your daily card transactions is sent to the provider until the advance is paid back.

This model is a lifesaver for businesses with high volumes of card sales, like restaurants, coffee shops, or retail stores. Let's say a restaurant owner needs $20,000 for an emergency kitchen repair. With an MCA, they can get funded fast. Repayment ebbs and flows with their business—on busy days, they repay more; on slow days, they repay less. It’s directly tied to their cash flow, so it never puts them in a bind.

The global demand for this kind of quick, flexible capital is massive. Short-term unsecured options, including MCAs, actually command the largest revenue share worldwide because they solve immediate needs like hiring staff or launching a marketing campaign. In fact, the market is expected to grow by an incredible USD 4,023.4 billion between 2024 and 2029, driven largely by small and medium-sized businesses. You can dig deeper into the growth of the unsecured loan market to see just how prevalent these tools have become.

Ultimately, choosing the right unsecured funding isn’t about finding the single "best" option. It’s about accurately diagnosing your company's immediate need and matching it with the financial tool built for that exact job. Whether you need a one-time investment, a revolving cash reserve, or a quick boost tied to your sales, there's an unsecured option designed to get you there.

Understanding the True Cost of Your Loan

When you're looking at a loan offer, the big number—the loan amount—is what usually grabs your attention. But that's just the starting point. The real cost of an unsecured business loan is hidden in the details: the rates, the fees, and the way you're expected to pay it back. Getting a handle on these components is absolutely critical to making a sound financial move for your business.

Think of it this way: unsecured loans are built for speed and accessibility. Because the lender is taking on more risk without any collateral to fall back on, the financial terms are naturally going to look a bit different from a standard bank loan. The convenience is a huge plus, but it comes with its own language. Learning to speak it is the only way to avoid nasty surprises later on.

This infographic breaks down the most common types of unsecured funding that business owners like you are using today.

As you can see, options like term loans, lines of credit, and cash advances all fall under the "unsecured" umbrella, but they're each structured to solve very different business challenges.

Decoding the Different Rates and Fees

One of the biggest hurdles for business owners is wrapping their heads around the difference between an interest rate and a factor rate. They both dictate how much you'll pay for the money, but they're calculated in completely different ways—and that can lead to a huge gap in your total repayment amount.

An Annual Percentage Rate (APR) is probably what you're used to seeing with mortgages or car loans. It’s the yearly cost of borrowing, shown as a percentage, and it usually includes both the interest and some of the fees. Crucially, it's often calculated on a declining balance, meaning you pay less interest as you pay down the principal.

A factor rate, on the other hand, is a simple multiplier often used for merchant cash advances and other short-term financing. It's written as a decimal (like 1.3). To figure out your total repayment, you just multiply the amount you borrow by that number. For a $50,000 advance with a 1.3 factor rate, you’ll pay back exactly $65,000. It doesn't matter how fast you pay it off; that total is fixed from day one.

Beyond the headline rate, you’ve got to keep an eye out for other costs:

- Origination Fees: This is a one-time fee the lender charges for setting up the loan. It's usually a small percentage of the total loan amount, and it’s often taken directly out of the funds you receive.

- Late Payment Fees: Miss a payment deadline, and you'll likely get hit with a penalty. These can add up quickly and inflate your total cost.

How Your Payment Schedule Impacts Cash Flow

Another piece of the puzzle is how often you have to make payments. Forget the standard monthly bill you get with traditional loans. Many unsecured options use more frequent payment schedules that are designed to sync up with a business's daily or weekly sales.

- Daily Payments: Very common with MCAs, where a small, fixed amount is pulled from your business bank account every single business day.

- Weekly Payments: Another popular choice for short-term loans, this gives you a little more breathing room than a daily schedule.

- Monthly Payments: This is the classic structure you'll find with most unsecured term loans, and it works just like any traditional loan you've had before.

While smaller daily or weekly payments might seem easier to handle, they demand constant attention to your cash flow. You have to be sure the money is in your account every single day to avoid problems.

The real cost of a loan isn't just the interest; it's the total cash outlay over the life of the loan. Always calculate the total repayment amount to make a true apples-to-apples comparison between different offers.

To bring this to life, let’s look at two different ways to get $50,000 in funding.

Hypothetical Unsecured Loan Offer Comparison

Here's a sample breakdown of two offers. One is a more traditional term loan, and the other is a merchant cash advance. Notice how the small details dramatically change the final cost.

| Metric | Lender A Offer (Term Loan) | Lender B Offer (MCA) |

|---|---|---|

| Funding Amount | $50,000 | $50,000 |

| Rate Structure | 15% APR | 1.3 Factor Rate |

| Origination Fee | 3% ($1,500) | 2% ($1,000) |

| Repayment Term | 24 Months | 12 Months |

| Payment Schedule | Monthly | Daily |

| Total Repayment | ~$58,300 | $65,000 |

Even though Lender B's offer has a lower origination fee, it ends up costing nearly $7,000 more in the long run. This is exactly why it's so important to look past the surface-level numbers and understand the full financial commitment you're making.

The Application and Funding Process: From Start to Finish

One of the best things about unsecured business loans is how quickly you can get them. If you've ever dealt with a traditional bank loan, you know the process can drag on for weeks, sometimes even months. Modern lenders have completely turned that model on its head, shrinking the timeline from application to cash-in-hand down to just a few days.

Forget mountains of paperwork and agonizing waits. This is a system built for the speed of business today. Let’s walk through what you can expect, step by step.

Step 1: The Initial Application

It all starts with a straightforward online form. Seriously, you can usually knock it out in a few minutes. Lenders just need the basics to get a feel for your business and see if you’re a potential fit.

You'll be asked for simple details like:

- Your business name and address

- How long you’ve been in business

- Your estimated monthly revenue

- The loan amount you're looking for

The great part is that this initial check usually involves a soft credit pull. This is a big deal because it does not impact your credit score, so there's no risk in exploring your options. It's a no-pressure way for the lender to pre-qualify you and see what kind of offers might be on the table.

Step 2: Submitting Your Documents

After the initial green light, you’ll need to provide a few documents to back up the numbers. This is where a little preparation can make a huge difference in how fast things move. Unlike secured loans, lenders aren’t looking for complex business plans or detailed asset appraisals.

They're focused on the here and now—the recent health of your business. The most common requests are:

- Recent Bank Statements: This is the big one. Lenders will want to see your last three to six months of business bank statements to verify your revenue and cash flow patterns.

- Government-Issued ID: A simple driver's license or passport to confirm you are who you say you are.

- Voided Business Check: This confirms your business bank account details, making sure the funds go to the right place.

Pro Tip: Before you even start applying, create a digital folder with clean PDF scans of these documents. When the lender asks for them, you can upload them instantly and potentially cut a full day or more off the approval timeline.

Step 3: The Lender's Review and Your Offer

Once your documents are in, the lender's underwriting team takes over. They use a mix of smart technology and human review to analyze your business's financial health and assess the risk. For most unsecured loans, this happens incredibly fast—often within a few hours.

If everything checks out, they'll come back to you with a loan offer. Typically, a funding advisor will call to walk you through the specifics, breaking down the numbers so you can feel confident in your decision.

This is your chance to get clarity on:

- The total loan amount

- The interest rate (or factor rate)

- The repayment term and frequency (daily, weekly, or monthly)

- Any extra fees, like an origination fee

Step 4: Final Agreement and Getting Funded

Happy with the offer? The final step is to sign the loan agreement, which is almost always done electronically. Once you’ve signed on the dotted line, the lender gets the green light to release the funds.

And this is where the speed really shines. In most cases, the money is wired directly to your business bank account and is available for you to use within 24 to 48 hours. This rapid access means you can jump on that time-sensitive opportunity or solve that urgent problem without missing a beat.

Funding Alternatives and When to Use Them

Unsecured business loans are fantastic for their speed and flexibility, but they're not a one-size-fits-all solution. A smart funding strategy means knowing all the tools in your financial toolkit. Sometimes, a different path makes more sense for your specific goals, especially when you can trade speed for better terms.

Let’s be clear: choosing the right financing is about more than just getting cash. It's about finding the most effective and cost-efficient way to grow. By looking at a few key alternatives, you can align your funding perfectly with your business plan.

SBA Loans: For Lower Rates and Longer Terms

If your business has a solid track record and you're not in a huge rush, a loan backed by the Small Business Administration (SBA) is definitely worth a look. The SBA doesn't lend the money directly; instead, it guarantees a significant portion of the loan for the bank, which takes a lot of the risk off the lender’s plate.

What does that government backing mean for you? Two huge perks:

- Lower Interest Rates: With less risk on their end, lenders can offer some of the most competitive rates you’ll find anywhere.

- Longer Repayment Terms: SBA loan terms can stretch out for years—even decades for real estate—which means your monthly payments are much more manageable.

Of course, there’s a catch. The application is rigorous, and the approval timeline can take several weeks or even months. An SBA loan is perfect for big, strategic moves like buying commercial property or acquiring another company—situations where saving thousands in interest over the long haul is more important than getting cash tomorrow.

Equipment Financing: For Specific Asset Purchases

Need a new delivery truck, a high-tech manufacturing machine, or a full suite of new computers? Equipment financing was designed for exactly that. It works a lot like a car loan: the asset you’re buying acts as its own collateral.

This built-in security makes a huge difference. Since the loan is backed by a tangible asset, it’s often easier to get approved, even for newer businesses or those with less-than-perfect credit. The rates are typically better than what you’d get with an unsecured business loan, and you'll get the funds much faster than you would with a traditional bank loan.

Key Insight: The best funding choice really comes down to what you're trying to accomplish. Unsecured loans are champions of speed and flexibility for operational cash flow and sudden opportunities. Alternatives like SBA loans and equipment financing, on the other hand, offer specialized, cost-effective terms for specific, long-term investments.

Ultimately, this isn't just about getting funded. It's about strengthening your business's financial foundation. If you need to upgrade your construction equipment, equipment financing is a direct and logical route. If you're executing a well-documented five-year expansion plan, the incredible terms of an SBA loan are tough to beat. But when you need working capital now to jump on a time-sensitive deal, the speed of an unsecured loan is simply unmatched.

Common Questions About Unsecured Business Loans

Diving into business financing can feel a bit like learning a new language. You're not alone if you have questions about unsecured business loans and how they actually work. Let’s clear up some of the most common points of confusion so you can move forward with confidence.

We'll cover everything from how applications affect your credit to how fast you can actually get your hands on the cash.

Will Applying for an Unsecured Loan Hurt My Credit Score?

This is a big one for most business owners, and the short answer is: probably not, especially in the beginning. Most modern lenders and funding platforms use a soft credit pull for the initial application. Think of it as a preliminary check-up that lets you see what you might qualify for without leaving a mark on your credit report.

Only after you’ve reviewed your options and decided to accept a specific loan offer does a hard credit pull happen. That can cause a small, temporary dip in your score, but by then, you're already on your way to getting funded. This approach lets you shop around for the best deal without any risk.

Can I Get an Unsecured Loan with Bad Credit?

Yes, it's definitely possible. While a traditional bank might see a low credit score as a deal-breaker, many alternative lenders look at the bigger picture.

Lenders are often more interested in your business's recent performance and consistent cash flow than a years-old credit issue. Strong and steady revenue can frequently outweigh a low credit score, demonstrating your ability to handle repayments.

A stronger credit profile will always help you secure better rates and terms, there's no doubt about that. But if your business is healthy and generating consistent income, you still have a very good shot at getting the unsecured funding you need.

How Quickly Will I Receive the Funds?

Speed is where unsecured business loans truly shine. The entire process is built to be fast, cutting out the weeks (or even months) of waiting you often get with old-school bank loans.

Once you’ve submitted your application, gotten approved, and signed the final offer, things move very quickly. In most cases, you'll see the funds hit your business bank account within 24 to 48 hours. This kind of speed means you can jump on urgent opportunities or solve unexpected problems without missing a beat.

What Is a Factor Rate and How Is It Different?

Getting a handle on how much your loan will actually cost is crucial. Some unsecured loans use a standard Annual Percentage Rate (APR), which you’re probably familiar with. However, many short-term options, like a merchant cash advance, use something called a factor rate.

A factor rate is just a simple multiplier, shown as a decimal like 1.2 or 1.35. You multiply your loan amount by the factor rate to get your total repayment amount. It's that straightforward.

For example, a $20,000 loan with a 1.35 factor rate means you will repay a total of $27,000. The total cost is set in stone from day one, which gives you clear, predictable numbers to work with.

Ready to explore your funding options without the guesswork? The dedicated advisors at FSE - Funding Solution Experts can help you navigate offers from over 50+ lenders to find the perfect fit for your business goals. Start your no-obligation application today and see what you qualify for.