Growth capital is the money a company takes on when it's ready to jump from being a successful business to a major force in its market. This isn't seed money for a concept scribbled on a napkin; it's high-octane fuel for an established company that’s already profitable and has a solid track record.

Essentially, growth capital closes the gap between being a solid local player and becoming a market leader.

Understanding Your Business Expansion Fuel

Imagine your business is a race car. It's well-built, you've got a great driver, and you've consistently won races on your local circuit. You’ve proven the model works. But to compete on the national or global stage, you need a serious upgrade.

Growth capital is that upgrade. It’s the bigger engine, the advanced aerodynamics, and the world-class pit crew you need to start winning the really big races. It’s the funding you secure for a specific, major expansion project.

This could mean a few different things in practice:

- Rolling out a new product line to grab more of your market.

- Expanding your physical or digital footprint into new territories.

- Buying out a smaller competitor to consolidate your position.

- Making a significant investment in technology to overhaul your operations and efficiency.

More Than Just a Loan

This is a critical distinction. A traditional bank loan is often about your credit history and what assets you can put up as collateral. Growth capital investors, on the other hand, are betting on your future. They look at your current success as the launching pad for something much bigger.

Because of this, the terms are often more flexible and structured around your specific expansion plans. It’s treated more like a partnership than a simple transaction.

Growth capital isn't about keeping the lights on or maintaining the status quo. It’s for aggressively capturing a market opportunity. This funding is designed for companies that have hit a ceiling and need a significant cash infusion to break through to the next level.

The amount of money available for this kind of scaling is immense. Global equity market capitalization recently jumped 8.7% year-over-year to an incredible $126.7 trillion. At the same time, equity issuance—the actual money flowing into companies—climbed 21.5% to $504.8 billion, signaling a strong investor appetite for backing growth-stage firms. You can dig deeper into these global capital market trends and see the full research for yourself.

To put it simply, here’s a quick overview of what growth capital is all about.

Growth Capital at a Glance

This table breaks down the core components of growth capital into an easy-to-digest format.

| Characteristic | Description |

|---|---|

| Target Company | Established, profitable, and proven businesses ready for major expansion. |

| Primary Goal | To fund specific growth initiatives like market expansion or new product launches. |

| Funding Type | Typically a minority equity stake, structured debt, or a hybrid of both. |

| Investor Focus | Future growth potential and scalability, not just historical performance or collateral. |

| Relationship | A strategic partnership; investors often provide expertise and connections. |

| Risk Profile | Lower risk than venture capital because the company is already successful. |

| Control | Founders usually retain majority control of the company. |

Think of it as smart money from a partner who is just as invested in your next big move as you are.

Choosing the Right Fuel: Growth Capital vs. The Alternatives

Picking the right financing is one of the most critical decisions you'll ever make as a business owner. It’s like choosing the right fuel for a high-performance engine; the wrong choice can stall your progress, while the right one can rocket you forward. This is precisely why getting a firm grasp on growth capital—and how it stands apart from other options—is so important.

It's tempting to lump all business funding into one big category, but that’s a mistake. Growth capital occupies its own unique niche, and it’s fundamentally different from venture capital, bank debt, or a private equity buyout. Each is designed for a different purpose and a different stage of a company's life.

Growth Capital vs. Venture Capital

The most common mix-up is between growth capital and venture capital (VC). The real difference boils down to risk and maturity. Venture capital is the high-stakes bet on early-stage startups. These are often pre-revenue companies with a big, disruptive idea. VC investors know that most of their bets will fail, but they're hoping one or two will become the next unicorn.

Growth capital, on the other hand, is for businesses that have already proven their model. You have paying customers, predictable revenue streams, and a clear path to profitability (if you're not there already). The investors aren't gambling on an idea; they're investing in a well-oiled machine that’s ready to scale. They're providing the high-octane fuel, not the parts to build the engine from scratch.

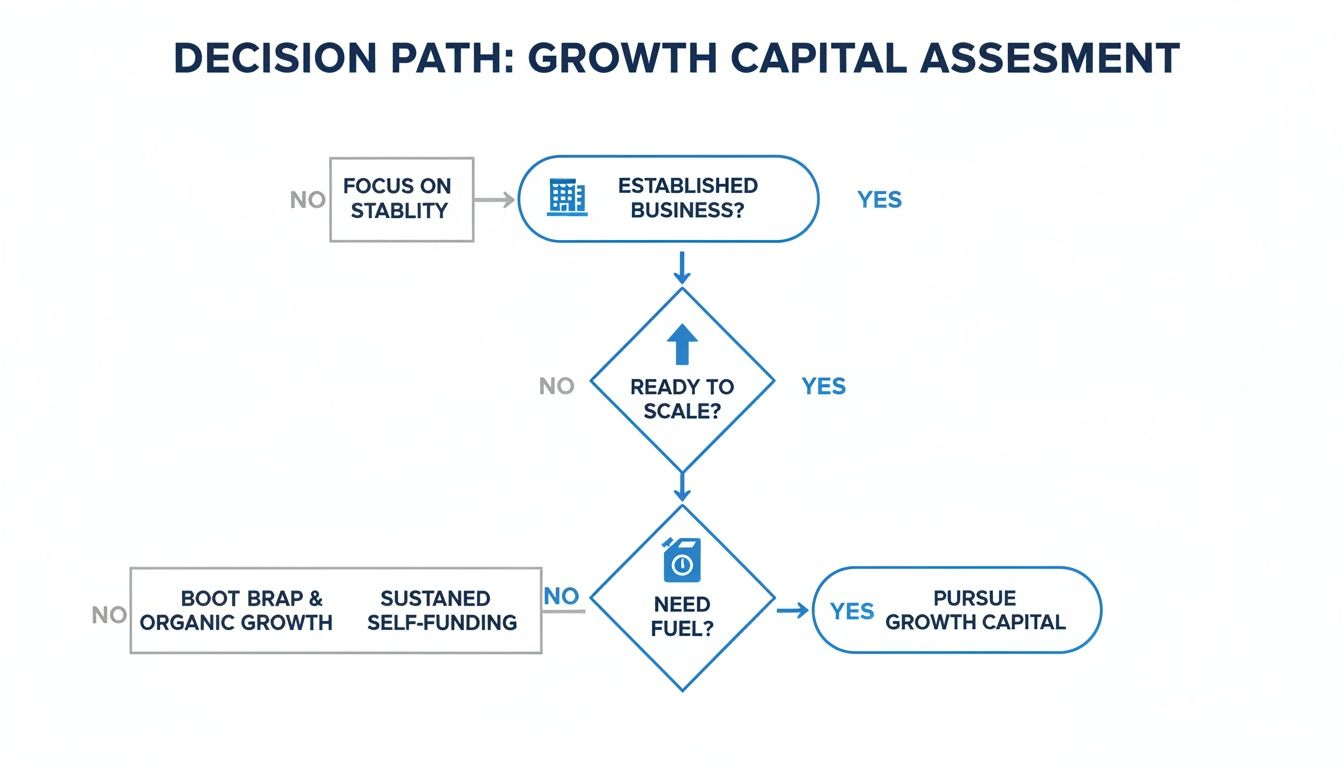

This decision tree shows where growth capital comes into play for a business that’s past the startup phase and ready to hit the accelerator.

As you can see, once a business has found its footing and validated its market, growth capital is the logical next step for aggressive, strategic expansion.

Bank Loans and Private Equity Buyouts

Of course, there are other paths. Traditional bank loans are a common route, but they operate on a completely different philosophy. Banks are, by nature, risk-averse. They look backward at your credit history and what collateral you can put up, often tying you down with strict covenants that can suffocate your flexibility just when you need it most. A bank loan is fine for predictable needs, but it’s often too rigid for a dynamic, all-out growth campaign.

A bank loan asks, "What assets can you pledge to secure this debt?" A growth capital provider asks, "What's your plan to conquer the market, and how can we help you get there?"

At the other end of the spectrum, you have the private equity (PE) buyout. In a classic buyout, a PE firm takes a majority or controlling stake, and founders often cash out a significant portion of their ownership. This frequently means giving up day-to-day control. Growth capital is the opposite. It’s a minority-stake investment designed to empower the existing leadership team, not replace it. You sell a small piece of the company to supercharge its growth while keeping your hands firmly on the wheel.

To make these distinctions even clearer, here’s a side-by-side look at how these funding options stack up.

Funding Options Compared: Growth Capital vs. The Alternatives

| Funding Type | Typical Business Stage | Use of Funds | Equity Stake | Risk Profile |

|---|---|---|---|---|

| Growth Capital | Established, profitable, or near-profitable. Proven business model. | Scaling operations, market expansion, product development, strategic acquisitions. | Minority stake (typically 10-30%). | Moderate. Investing in a proven model. |

| Venture Capital | Early-stage, pre-revenue, or early revenue. High-growth potential. | Product development, market validation, building the initial team. | Significant minority or majority stake. | High. Betting on an unproven idea. |

| Bank Loan | Any stage with sufficient cash flow and collateral. | Working capital, equipment purchases, real estate. | None. This is debt, not equity. | Low (for the lender). Secured by assets. |

Seeing them laid out like this really highlights the specific role growth capital plays. It's not about survival or starting from zero; it's about seizing a proven opportunity and taking your company to the next level, with you still leading the charge.

Putting Growth Capital to Work in the Real World

It's one thing to talk about growth capital in theory, but seeing it in action is where the concept really clicks. This isn't just about getting a check in the bank; it’s about making a calculated, strategic move to unlock a whole new level of revenue and market share. It’s the fuel that turns steady, incremental progress into a massive leap forward.

The most successful companies earmark these funds for specific, high-impact initiatives. We’re not talking about just covering payroll or keeping the lights on. Growth capital is for projects designed to generate a serious return on investment.

High-Impact Growth Capital Use Cases

Think of this funding as a catalyst for a very specific, pre-planned project. The goal is always to move the needle in a big, meaningful way.

Here are a few common scenarios I’ve seen play out:

- Market Expansion: A regional software company has maxed out its local market. They secure funding to open a new office on the opposite coast, hiring a dedicated sales team to break into an entirely new customer base.

- Strategic Acquisitions: An established manufacturing firm buys a smaller competitor. In one move, they absorb its client list, acquire its unique technology, and take a rival off the board.

- Major Technology Investments: A mid-sized logistics company invests in an advanced fleet management system. The result? They slash fuel costs and dramatically improve delivery times, making them more competitive overnight.

- Significant Product Development: A popular e-commerce brand uses the capital to design, manufacture, and launch a highly anticipated new product line, cementing its leadership position.

The core idea behind every growth capital deal is converting money into momentum. The question isn't just "How much do we need?" but "What specific action will this capital enable that we cannot do today?"

This focus on targeted investment is happening everywhere. Take infrastructure, for example—a prime area for growth capital. Private equity deployment in this space saw an 18% jump in deal value in a single year, the second-highest on record. What’s really telling, though, is that the number of deals only rose by 7%. This points to a clear trend: investors are backing bigger, more strategic plays designed for massive scale, not just small, scattered funding rounds. You can dig deeper into these numbers in McKinsey's Global Private Markets Report.

From Plan to Profit: A Real-World Example

Let's make this even more tangible.

Picture a regional construction company that’s built a great reputation on residential and small commercial jobs. They keep seeing bids for huge, profitable municipal contracts, but they don't have the heavy machinery needed to even get in the door. They’re stuck.

By securing $750,000 in growth capital, they aren't just getting cash. They're executing a precise plan:

- Purchase Advanced Equipment: They immediately acquire two new excavators and a crane.

- Hire Skilled Operators: They bring on three certified operators to run the new gear.

- Bid on Larger Contracts: Now that they’re properly equipped, they confidently bid on a lucrative city infrastructure project—and they win it.

Suddenly, their entire business has changed. Their revenue potential skyrockets, their profit margins expand, and they’ve established themselves as a serious player in a much more profitable market. That’s the power of growth capital.

A Practical Checklist for Growth Capital Readiness

Getting growth capital is a huge step, but let's be realistic—investors and lenders aren't writing checks based on ambition alone. They're looking for concrete signs that your business is a smart bet, not a long shot.

Before you even think about filling out an application, you need to take a hard, honest look in the mirror. Is your company truly ready for this?

Think of this checklist as your pre-flight inspection. Going through these points now helps you spot weaknesses and fix them, ensuring you present the most compelling case when you're finally sitting across the table from potential funders. This isn't just about qualifying; it's about getting the best possible terms.

Key Pillars of Readiness

Investors are searching for two things: stability in the present and a clear vision for the future. Your ability to demonstrate strength in these areas is often what separates a quick "no" from an enthusiastic "yes."

- A Proven Business Model: You need consistent, predictable revenue. This is the proof that you’ve moved beyond the startup "let's try this" phase and have found a real market that wants what you sell.

- A Clear Path to Profitability: If you aren't profitable yet, that's okay—but you'd better have a detailed, data-driven plan that shows exactly how this capital injection gets you into the black. Wishful thinking won't get you funded.

- A Solid Management Team: Investors aren't just buying into a business; they're backing the people who run it. Your leadership team needs a demonstrated history of making smart decisions and the know-how to handle the chaos of rapid growth.

The question every investor is asking is simple: "Does this business have an engine that works, and is the team capable of handling more horsepower?" A confident 'yes' to both is your ticket in.

Your Strategic Plan Is Everything

What you've done is important, but where you're going is what gets a deal done. Your strategic plan is the centerpiece of any growth capital pitch. You need an airtight strategy detailing exactly how you'll use the funds to generate a significant return.

This plan has to be more than a few bullet points. It should clearly outline the expected outcomes, timelines, and the specific KPIs you’ll use to measure success along the way.

This is why looking at global IPO trends is so revealing. In a single year, 1,293 IPOs raised a staggering $171.8 billion worldwide—a 39% jump in proceeds from the previous year. This shows that the market is hungry for mature companies with compelling growth stories, whether they're seeking private funding or a public offering.

You can dive deeper into these global IPO trends and investor appetites to see what the market values. Your strategic plan is what makes your growth story believable and, ultimately, investable.

The Pros and Cons: A Clear-Eyed View of Growth Funding

Taking on growth capital is a huge step. It’s a moment that can redefine your company's future, so you need to walk into it with your eyes wide open, ready to weigh the massive opportunities against the very real trade-offs. The right deal can feel like strapping a rocket to your business, but the wrong one can send you off course.

Let's be clear: this isn't just about the money. It's about bringing on a strategic partner. Thinking through both sides of that partnership is the only way to make sure the agreement you sign actually serves your vision for the company.

The Upside: More Than Just a Check

The most powerful argument for growth capital is simple: it lets you do big things, fast. You're essentially buying speed and collapsing a five-year plan into eighteen months.

- Fuel for Hyper-Growth: This is the most obvious win. Suddenly, that new market you’ve been eyeing, the game-changing product line, or the strategic acquisition is within reach. You have the resources to make bold moves, now.

- A Partner in the Trenches: Top-tier growth investors don't just write checks and wait for reports. They bring a network, strategic know-how, and operational experience to the table. They’ve seen this movie before and can help you avoid common scaling pitfalls.

- Instant Credibility Boost: When a respected firm invests millions into your company, the market notices. This "stamp of approval" can be incredibly powerful, opening doors to key hires, strategic alliances, and bigger customers that might have been hesitant before.

A growth capital partner isn't just a lender; they're an investor in your vision. Their success is directly tied to yours, creating a powerful alignment of interests that a traditional bank loan simply can't offer.

This kind of aligned partnership can be the critical support system you need when the pressure of scaling up gets intense.

The Downside: What You're Giving Up

Now for the other side of the coin. It’s crucial to be realistic about the trade-offs, because they are significant. Understanding them upfront allows you to negotiate terms that protect what you’ve built.

For most founders, the biggest sticking point is equity dilution. Every dollar of equity financing means selling off a small piece of your company. While it's almost always a minority stake, it means you're slicing the pie differently. Your ownership percentage shrinks, and future profits are shared.

Then there's the pressure to perform. Your new partners have invested with clear expectations for a return, and the clock is ticking. This brings a whole new level of accountability. The focus can shift from your original, organic pace to hitting specific quarterly metrics and growth targets defined by the deal.

Finally, you’re no longer the only one calling the shots. Bringing on investors means you have a board and key stakeholders who need to be consulted on major decisions. This partial loss of autonomy is the price of admission for the capital and expertise. The key to making this work is brutal honesty and clear communication from day one, ensuring everyone is on the same page about the path forward.

Your Action Plan for Securing Growth Capital

Now that you have a solid grasp of what growth capital is, it's time to build a clear roadmap for finding the right partner. The path from recognizing you need funds to actually securing them is all about meticulous preparation and sharp evaluation. A disciplined approach is your best bet for landing a partner who truly gets your long-term vision.

First things first: get your house in order. This isn't just about having clean books. It means building detailed financial projections that paint a clear picture of how this new capital will drive a return. You'll also need a polished business plan that tells a compelling story about your market opportunity and, just as importantly, why your team is the one to make it happen.

The Search and Vetting Process

With your documentation in place, the hunt begins. Your goal is to identify potential partners—whether they're private equity investors or alternative lenders—who have a proven track record in your specific industry. This isn't the time for a shotgun approach; a targeted search saves everyone time.

Once you start getting term sheets, the real work begins. You have to switch gears from being a salesperson pitching your business to being a sharp-eyed analyst. It’s never just about the big number on the offer sheet; the devil is in the details of the deal structure. At FSE, our advisors specialize in helping businesses compare multiple funding offers to find that perfect strategic fit.

Securing capital isn't just a transaction; it's the beginning of a strategic partnership. The right offer can be a rocket ship for your growth, but the wrong one can become a long-term anchor. Your diligence at this stage is the best defense against a bad deal.

How to Spot Red Flags in a Funding Offer

Evaluating offers is a skill, and a big part of it is knowing what to look out for. Be on high alert if you come across any of these warning signs:

- Vague or Unclear Terms: If you can't easily understand the repayment schedule, interest calculations, or any attached covenants, that's a problem. A reputable partner will always prioritize clarity.

- Excessive Upfront Fees: Legitimate funders might have origination fees, but they're typically reasonable and rolled into the loan itself, not demanded as a large cash payment before you see a dime.

- High-Pressure Tactics: Any potential partner who tries to rush you into signing "before the offer expires" is waving a massive red flag. A true partner will respect your need to conduct due diligence and make an informed decision.

Ultimately, the objective is to secure fuel for your growth engine without accidentally poisoning the well. By preparing diligently and vetting every offer with a critical eye, you put yourself in the best possible position to find a strategic partner who can help you hit those ambitious goals.

Common Questions About Growth Capital

Let's wrap up by tackling some of the most common questions we hear from business owners who are just starting to explore growth capital. These are the practical, real-world concerns that come up time and time again.

How Much of My Company Do I Have to Give Up?

This is probably the biggest question on every founder's mind, and the answer is: it depends entirely on the type of funding.

If you go the traditional equity route, you're typically looking at selling a minority stake in your business—often somewhere between 10% and 30%. But it's crucial to know that many modern growth capital solutions don't require you to give up any ownership at all. Things like working capital loans are structured as debt, meaning you get the cash you need with zero equity dilution.

What Kind of Revenue Do I Need to Qualify?

While the exact numbers vary from one provider to the next, investors want to see a track record. You need to show that your business is stable and has predictable income.

For most alternative funding partners, a good starting point is a minimum of $10,000 in consistent monthly revenue. They'll also typically want to see that you've been in business for at least a year. It's all about proving you have a solid foundation to build on.

How Long Does This Whole Process Take?

The timeline can be night and day depending on where you look. If you’re trying to secure a traditional bank loan or wooing a venture capital firm, get ready for a marathon. It can take months of meetings, pitches, and deep-dive due diligence.

This is where alternative financing really shines. With a streamlined process, many business owners can get from application to approval—with cash in the bank—in as little as 24 to 48 hours. When an opportunity is time-sensitive, that speed makes all the difference.

Is This Just for Tech Startups?

Absolutely not. That’s a common myth, but growth capital is for any established business that has a clear, actionable plan for expansion. It's completely industry-agnostic.

We see companies in construction, logistics, manufacturing, and retail thrive with this kind of funding. The core requirement isn't about being in a "hot" sector; it's about having a proven business model that's ready to scale.

Navigating these options can feel overwhelming. At FSE - Funding Solution Experts, our advisors are here to help you cut through the noise. We'll help you compare offers from over 50+ lending partners to find the capital structure that truly fits your growth plans.

See what your funding options are today by visiting our site at https://www.fseb2b.com.