Think of a working capital line of credit as your business's financial backstop—a flexible pool of cash you can tap into whenever you need it to cover day-to-day operational costs. Unlike a typical loan where you get a lump sum, here you only borrow what you need, when you need it. Best of all, you only pay interest on the funds you actually use, which makes it a smart way to manage those inevitable cash flow gaps.

Your Financial Safety Net for Business Operations

Every business owner knows the feeling. One month, sales are soaring. The next, a big client pays late or an unexpected repair bill pops up, and suddenly things feel tight. A working capital line of credit is built for exactly these moments, acting as a rechargeable financial safety net.

It’s less like a traditional, one-time loan and more like a credit card dedicated to your business. You get a pre-approved credit limit, and you can draw funds from it as often as you need. Once you pay back what you’ve used, that money is right there waiting for you again. It’s this revolving nature that makes it such a powerful tool for staying financially steady.

The Power of Financial Flexibility

The real magic of a line of credit is its flexibility. It gives you the freedom to act fast without getting locked into the rigid payment schedules of long-term debt. With immediate access to capital, you can handle common business hurdles and jump on opportunities with confidence.

Here’s where it really shines:

- Managing Daily Expenses: When a slow month hits, you can still easily cover payroll, rent, and utilities without breaking a sweat.

- Seizing Growth Opportunities: A supplier offers a huge discount for a bulk inventory purchase? You can say yes. A great marketing opportunity comes up? You can fund it.

- Bridging Revenue Gaps: Smooth out the cash flow bumps during seasonal lulls or while you're waiting for those 30- or 60-day invoices to get paid.

This kind of adaptability is why it has become a staple for small and mid-sized businesses. In fact, the share of U.S. growth companies using bank lines of credit jumped an incredible 95% in a single year, going from 14.1% to 27.6% of firms surveyed. That surge points to a clear shift toward more nimble financial solutions. You can dive deeper into the full report on corporate capital trends to see how businesses are changing their approach.

A working capital line of credit isn't just about plugging holes; it's about building operational resilience. It gives you the liquidity to run your business smoothly, no matter what surprises the market throws at you.

Whether your business is in construction, trucking, or retail, this guide will walk you through exactly how to get and use a line of credit to make sure your company is always ready to thrive.

How a Working Capital Line of Credit Works

Let’s get one thing straight: a working capital line of credit isn't your typical loan. It’s better to think of it as a financial safety net for your business—a dedicated pool of cash you can tap into whenever you need it, giving you real control over your finances without locking you into unnecessary debt.

Say you get approved for a $100,000 credit limit. That money doesn't just land in your bank account in one big chunk like a term loan. Instead, it sits on standby, ready for you to draw from when an opportunity—or a problem—pops up. This fundamental difference is what makes it so powerful.

When that moment arrives, you pull exactly what you need. A critical machine breaks down? You can draw $10,000 to get it fixed. A slow month leaves you short for payroll? Draw $20,000 to cover it. You call the shots on how much you use and when.

The Draw and Repay Cycle

At the heart of a working capital line of credit is its revolving nature. This is a fancy way of saying that as you pay back what you've borrowed, your available credit goes right back up. It’s a continuous loop of access that provides ongoing financial stability.

It really boils down to a simple four-step process:

- Draw Funds: You take out a portion of your credit limit to handle a business expense.

- Use Funds: You put the cash to work, whether that’s buying new inventory or paying a supplier.

- Repay Over Time: You make regular payments on the amount you drew, plus interest, usually on a weekly or monthly schedule.

- Credit Replenishes: As you pay down your balance, that amount becomes available to use all over again.

This cycle can repeat as often as you need throughout the term of your agreement, ensuring you always have a fallback. In fact, making smart operational investments, like implementing automated inventory control, can actually reduce how often you need to draw by cutting costs and improving your cash flow.

How Interest and Repayments Work

Here’s the best part: you only pay interest on the money you actually use, not the entire credit limit. If you have that $100,000 line but have only drawn $15,000, interest is only calculated on that $15,000. This makes it a much more cost-effective tool than a large loan you might not even use completely.

Repayment terms are also built with real-world business cash flow in mind. Most lenders set up automatic payments, so you don’t even have to think about it.

Key Takeaway: The revolving door of a line of credit means you don’t have to go through the hassle of reapplying every time a new need comes up. Once you’re approved, that capital is yours to access for the entire term, offering a level of convenience that’s hard to beat for managing day-to-day operational costs.

Most repayment plans will look like one of these two models:

- Automated Weekly Payments: This is common with alternative lenders. Smaller, more frequent payments are automatically pulled from your business bank account, which can be easier to manage for some businesses.

- Monthly Payments: Just like a credit card, you’ll make one larger payment each month. This structure is more typical of lines of credit from traditional banks.

The right structure for you will depend on the lender and your company’s financial health. Ultimately, the goal is to set up a predictable repayment schedule that doesn't put a squeeze on your cash flow, so you can stay focused on what really matters: running your business.

Is a Line of Credit the Right Tool for Your Business?

Trying to find the right business funding can feel like navigating a maze. With so many options out there, it’s tough to know which one is the right fit for your company’s unique needs. A working capital line of credit is an incredibly versatile tool, but you really see its strengths when you put it side-by-side with other common financing products.

Getting a handle on these differences is crucial for making a smart financial decision. Think of it like a toolbox—each funding type is designed for a specific job. You wouldn't use a hammer when you need a screwdriver, and you wouldn't take out a huge loan for small, day-to-day cash flow gaps.

Working Capital Line of Credit vs Other Funding

Every business has different needs, and the right funding depends entirely on the job at hand. This table breaks down the most common funding types to help you see where a working capital line of credit shines compared to the alternatives.

| Funding Type | Best For | Repayment Structure | Flexibility |

|---|---|---|---|

| Working Capital Line of Credit | Managing cash flow, covering payroll, buying inventory, and handling unexpected expenses. | Revolving—pay interest only on what you use, then repay and reuse the funds. | Very high. Use funds for nearly any business purpose as needed. |

| Term Loan | Large, one-time investments like expansion, major projects, or buying another business. | Fixed monthly payments of principal and interest over a set term. | Low. Funds are disbursed in a lump sum for a specific, pre-approved purpose. |

| Merchant Cash Advance (MCA) | Businesses with high daily credit card sales needing immediate, fast cash. | A percentage of daily sales is automatically deducted until the advance is repaid. | Moderate. Funds are provided upfront, but repayment is tied directly to sales volume. |

| Equipment Financing | Purchasing specific machinery, vehicles, or technology for your business. | Fixed monthly payments, with the equipment itself serving as collateral. | Very low. Funds can only be used to purchase the approved equipment. |

Choosing the right option isn't just about getting cash; it's about getting the right kind of cash. A line of credit offers a level of on-demand flexibility that other products simply can't match for operational needs.

Line of Credit vs. Term Loan

The classic comparison is between a revolving line of credit and a standard term loan. A term loan gives you a single chunk of cash upfront, which you then pay back in fixed monthly installments over a predetermined period. It's built for big, planned, one-off investments.

Let's use an analogy:

- A term loan is like a mortgage. You get a large sum to buy a specific, major asset—like a new building or a huge piece of machinery.

- A line of credit is like a business credit card. You have a credit limit you can tap into whenever you need it for ongoing expenses like payroll or inventory. You only pay interest on the amount you’ve actually borrowed.

A term loan is perfect when you know exactly how much you need for a long-term project. But for managing the daily, unpredictable ebb and flow of business? The flexibility of a working capital line of credit is second to none.

Line of Credit vs. Merchant Cash Advance

A merchant cash advance, or MCA, is a different beast altogether. It’s not technically a loan; it’s an advance on your future sales. A provider gives you a lump sum of cash in exchange for a percentage of your daily credit and debit card sales until the advance and their fee are paid back.

MCAs are often easy to qualify for, but they can be expensive. Their cost is shown as a "factor rate," not an interest rate, which can sometimes hide the true cost. They're best for businesses like restaurants or retail stores that have a high volume of daily card transactions and need cash in a hurry.

A line of credit, on the other hand, gives you more predictable costs with a straightforward interest rate and a clear repayment schedule. It provides much greater control over your finances without siphoning off a piece of every sale, making it a far more sustainable tool for long-term cash flow management.

Line of credit vs. Equipment Financing

Equipment financing is a highly specialized tool. Just as the name implies, it's designed for one thing and one thing only: buying business equipment. The equipment you purchase acts as the collateral for the loan, which often makes it easier to secure than other types of funding. When you're weighing a major purchase, understanding all your options for financing is absolutely critical.

The catch? Its use is incredibly narrow. You can't use equipment financing to make payroll, restock inventory, or run a new marketing campaign. A working capital line of credit gives you the freedom to direct funds wherever your business needs them most, making it the clear winner for covering a wide spectrum of operational costs.

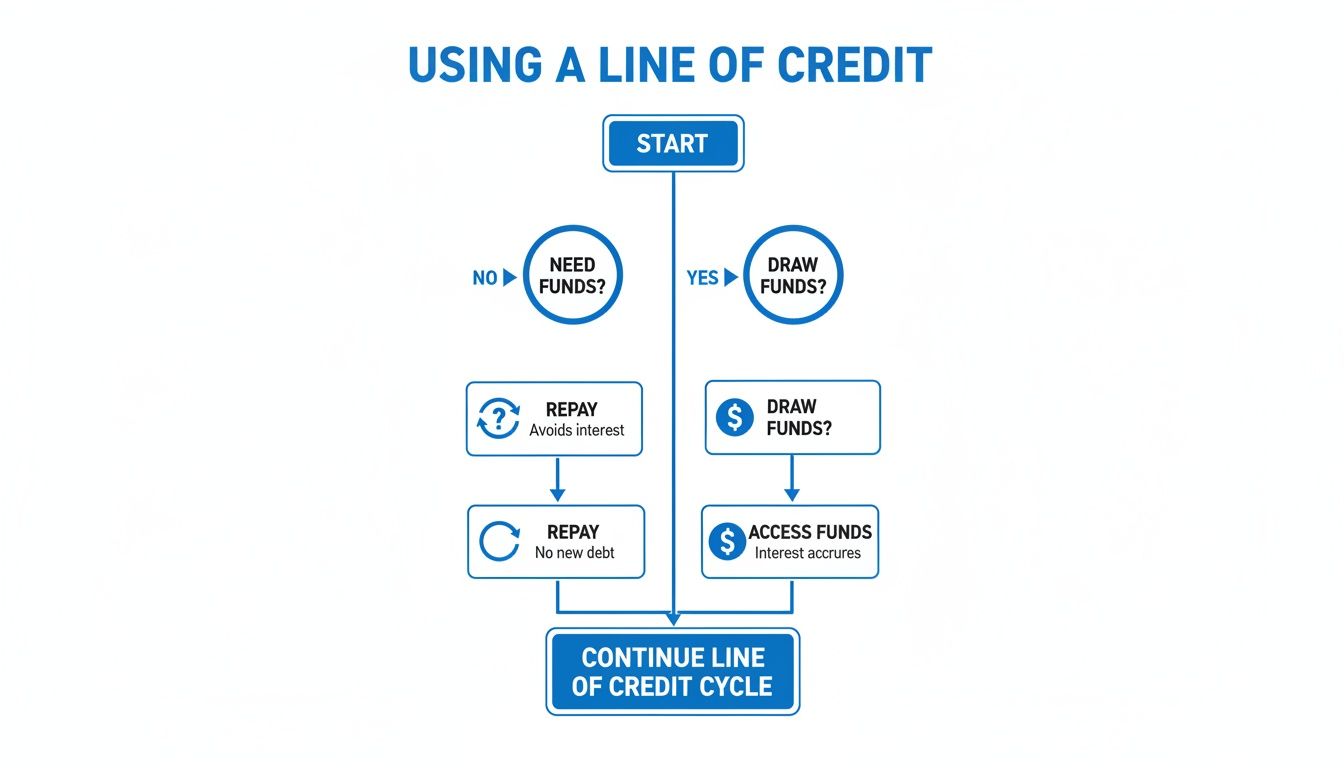

This simple flow chart shows just how straightforward and useful a revolving line of credit can be.

As you can see, the key advantage is its cyclical nature—you draw funds, use them, repay them, and the full credit line becomes available to you again. It’s a financial safety net that’s always there.

The best choice always comes down to your specific situation. By understanding how a working capital line of credit measures up against the alternatives, you can pick the perfect financial tool to drive your business forward and ensure you have capital ready right when you need it.

How Different Industries Use a Line of Credit

A working capital line of credit isn't some generic, one-size-fits-all loan. Its real power comes from how different businesses bend it to fit their unique operational rhythms. From chaotic job sites to bustling storefronts, this flexible funding becomes a strategic tool for bridging cash flow gaps, jumping on opportunities, and keeping the momentum going.

A working capital line of credit isn't some generic, one-size-fits-all loan. Its real power comes from how different businesses bend it to fit their unique operational rhythms. From chaotic job sites to bustling storefronts, this flexible funding becomes a strategic tool for bridging cash flow gaps, jumping on opportunities, and keeping the momentum going.

Seeing how other business owners tackle real-world problems is the best way to grasp its potential for your own company. Let's dig into a few specific scenarios.

Construction and Contracting

The construction world runs on projects, and that often means long, drawn-out payment cycles. A contractor might wrap up a major job but still have to wait 30, 60, or even 90 days to see the cash from that invoice. Meanwhile, the bills never stop—crews expect their paychecks, materials are needed for the next job, and equipment needs fuel.

This is where a line of credit is a game-changer.

- Upfront Material Costs: You can draw funds to buy lumber, concrete, and fixtures on the spot, securing what you need without draining your bank account.

- Consistent Payroll: It’s the key to making sure your crew gets paid on time, every single week, even if you’re still waiting on a big client payment to clear.

- Unexpected Repairs: When a critical piece of equipment like an excavator suddenly breaks down, a quick draw from the line covers the repair and prevents a costly project delay.

In short, it closes the gap between what you spend and what you earn, allowing you to take on more jobs at once and grow your business without the constant cash flow headache.

Trucking and Logistics

For any trucking company, cash flow is always on the move. Fuel, surprise repairs, and insurance payments are relentless. At the same time, a profitable last-minute haul can pop up out of nowhere, but you need cash on hand to even get the truck rolling.

A working capital line of credit is what keeps a logistics business moving forward. Say a driver is hundreds of miles from the shop when a tire blows out. With a line of credit, the owner can fund the repair instantly, getting that truck back on the road to finish the delivery on time.

It also provides the cash to fuel up for a lucrative cross-country job before getting paid for it, turning what could have been a logistical nightmare into a solid payday.

In sectors like construction and retail, managing cash flow is paramount. Recent data shows that Days Inventory Outstanding (DIO) has increased by 13.6% in Western economies, while Days Sales Outstanding (DSO) has risen 5.5% in North America. These trends mean cash gets trapped in inventory and unpaid invoices longer, making a flexible line of credit vital for covering operational gaps. Discover more insights about how working capital trends impact businesses on alliedmarketresearch.com.

Restaurants and Hospitality

The restaurant business is famous for its peaks and valleys. A great summer patio season or a packed holiday rush can bring in a ton of business, but gearing up for that surge costs money upfront. Owners have to hire and train extra staff, stock up on food and drinks, and ramp up marketing—all before that extra revenue actually hits the register.

Here’s how a line of credit helps smooth things out:

- Seasonal Staffing: Hire and train servers and cooks weeks before the busy season kicks in.

- Inventory Stock-Up: Buy ingredients in bulk to handle a full house or a massive catering order.

- Emergency Repairs: Instantly cover the cost of a broken freezer or oven without shutting down service.

Having that immediate access to capital means a restaurant can actually maximize its profits during those peak times instead of being held back by a temporary cash crunch.

Retail and E-commerce

For retailers, whether they’re online or on Main Street, inventory is king. Success boils down to having the right products on the shelf at the right time, especially for huge sales events like Black Friday or the holiday season. A line of credit gives you the buying power to properly prepare.

An e-commerce owner can draw on their line to place a huge inventory order months in advance, locking down popular items before the supplier sells out. It also lets them pour money into a big digital ad campaign to drive traffic when it matters most. Once the sales revenue starts flowing in, they pay down the line of credit, and it's ready to go for the next cycle.

Qualifying for Your Working Capital Line of Credit

Getting approved for a working capital line of credit is much more straightforward than most business owners assume, especially once you look beyond the big banks. While every lender has their own specific criteria, they all zero in on a few key signs of a healthy, stable business. Knowing what they’re looking for ahead of time is the best way to make your application a slam dunk.

Think of the application less like a test and more like an opportunity to tell your company's financial story. Lenders simply want to see that you have a handle on your operations, generate reliable cash flow, and manage your finances well. A little preparation helps you put your best foot forward.

The Core Qualification Pillars

When lenders review your application, they’re looking at a handful of core metrics. There’s no single magic formula, but most funding specialists and non-bank lenders want to see a solid foundation built on these three pillars. Hitting these general benchmarks will dramatically improve your odds of approval.

- Time in Business: Most lenders look for at least one year of operating history. This shows them your business is past the volatile startup phase and has a proven concept.

- Monthly Revenue: Consistent revenue is a huge factor. The typical minimum is around $10,000 per month in sales, which proves you have enough cash flow to manage repayments.

- Credit Profile: Your business and personal credit scores both come into play. Alternative lenders are certainly more flexible than traditional banks, but a personal credit score of 600 or higher is a common starting point.

These three data points give lenders a quick snapshot of your business’s stability and its capacity to repay new financing. A strong showing here doesn't just get you approved; it opens the door to better rates and higher credit limits.

Preparing Your Documentation

Gone are the days of binders filled with paperwork. Modern, tech-driven application processes have thankfully streamlined everything. Unlike a traditional bank that wants to see five-year projections and a full-blown business plan, funding specialists are more interested in what your business is doing right now.

Having these documents on hand will make the whole process feel effortless:

- Recent Bank Statements: This is the big one. Lenders will usually ask for your last three to six months of business bank statements. It gives them a real-time view of your revenue, cash flow patterns, and overall financial health.

- Basic Financial Records: For larger lines of credit, you might be asked for a recent profit and loss statement or a balance sheet. These give a broader picture of your company’s profitability.

- Proof of Ownership: Simple documents like your Articles of Incorporation are used to verify the legal structure and ownership of your business.

The modern application for a working capital line of credit is built for speed. By focusing on real-time data like bank statements instead of lengthy historical documents, funding specialists can often provide a decision within 24 hours.

This is a world away from the old-school bank loan process, which can drag on for weeks or even months. The goal is to get you the capital you need to act on an opportunity now, not next quarter. By gathering these few key documents, you set yourself up for the fastest possible funding decision.

Frequently Asked Questions About Lines of Credit

As you get serious about a working capital line of credit, a few key questions probably come to mind. It's smart to dig into the details—what it costs, how it affects your credit, and how it plays with any other financing you have. Let's tackle the most common questions business owners ask so you can move forward with confidence.

What Are the Typical Interest Rates and Fees?

There's no single, one-size-fits-all answer here. The cost of a working capital line of credit really depends on your business's financial health, how long you've been operating, and the specific lender. As you'd expect, businesses with a strong track record and consistent cash flow tend to qualify for the most competitive rates.

But the interest rate is only part of the story. You also need to keep an eye out for other potential costs that can add up:

- Draw Fees: Some lenders might charge a small fee every time you pull funds, often a percentage of the amount you draw.

- Maintenance Fees: You may see a monthly or annual fee just to keep the line open and available, even if you aren't using it.

- Late Fees: Just like any other loan, falling behind on payments will trigger penalties.

The bottom line? Always read the fine print. A good lender will be upfront about every potential fee so you can understand the true cost of the capital before you commit.

Will Applying Impact My Personal Credit Score?

That's a great question, and one every business owner should ask. The answer depends on the lender's process. Many modern funding partners, including us, start with a soft credit inquiry. This lets them take a look at your credit profile without dinging your score. It’s a no-risk way to see what you might qualify for.

If you like an offer and decide to move forward, the lender will then perform a hard credit inquiry to finalize everything. This will show up on your credit report and can cause a small, temporary dip in your score.

Key Takeaway: Nearly all business financing, including lines of credit, will require a personal guarantee. This means you, the owner, are personally backing the debt. It's a crucial link, so making timely payments is vital for protecting both your business's and your personal credit standing.

Can I Have a Line of Credit with Other Loans?

Absolutely. It’s very common for a business to have a line of credit working alongside other financing, like a term loan for a big expansion or an equipment loan for a new truck. Lenders get it—different business needs call for different financial tools.

When they review your application, they’ll look at your total debt burden. What they’re really asking is, "Does this business generate enough cash to handle all of its payments comfortably?" Having existing loans isn't a red flag, as long as your revenue shows you can handle the additional payments. What they want to see is responsible debt management, not a business stretched too thin.

Ready to see what your business qualifies for? At FSE - Funding Solution Experts, we simplify the process of securing a working capital line of credit. Our dedicated advisors will help you compare offers from over 50 lenders to find the best fit for your cash flow needs. Apply in minutes and get a no-obligation decision fast.