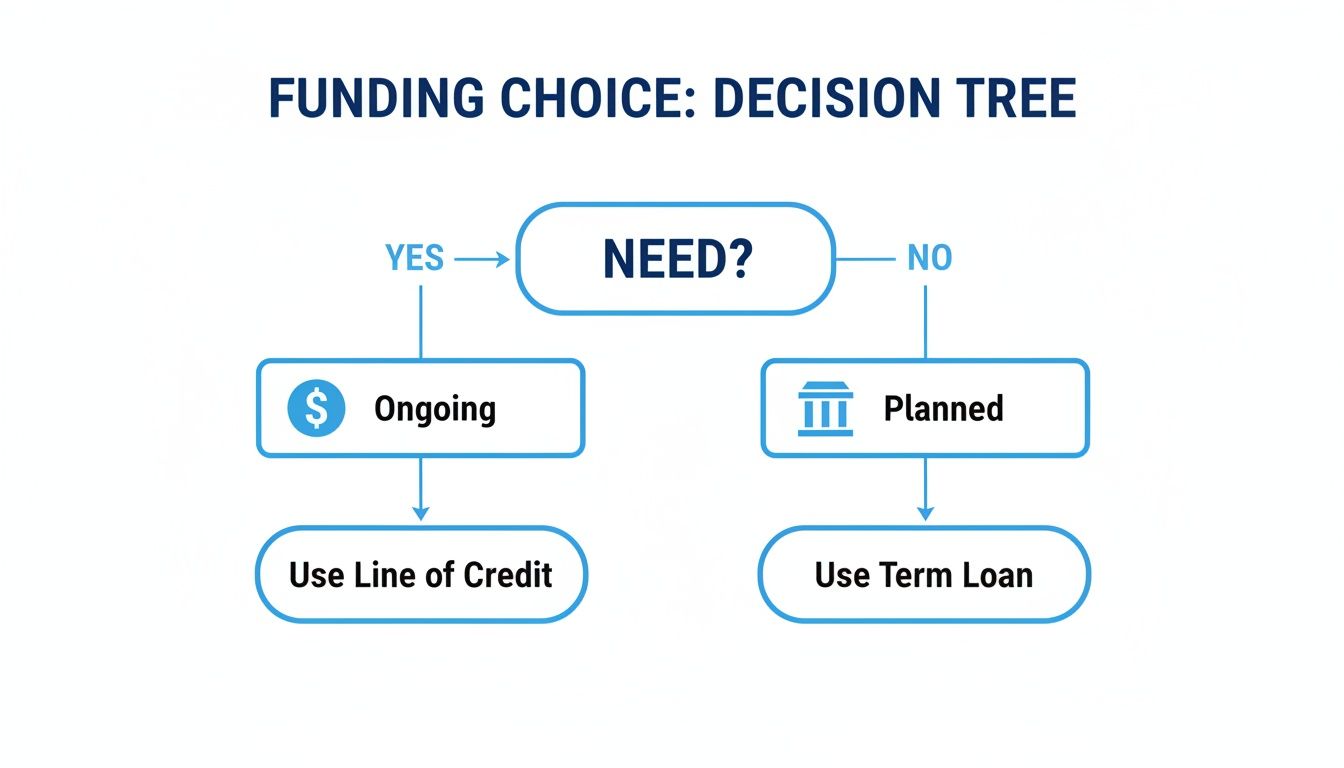

Choosing between a business line of credit vs loan comes down to one question: do you need a safety net for ongoing, unpredictable expenses, or a one-time cash infusion for a planned project?

A line of credit offers flexible, ongoing access to cash. A term loan provides a single lump sum for a specific investment.

Navigating Your Funding Options

Think of a business line of credit like a company credit card. You get an approved credit limit to draw from, repay, and draw from again as needed. It's ideal for managing unpredictable costs or smoothing out cash flow.

A business term loan is more like a mortgage. You receive the full amount upfront and repay it in fixed monthly installments. This is for large, one-time purchases like new equipment.

Line of Credit vs Term Loan: At a Glance

This table highlights the core differences.

| Feature | Business Line of Credit | Business Term Loan |

|---|---|---|

| Structure | Revolving credit to reuse. | One-time lump sum. |

| Best For | Cash flow, surprise costs. | Large, planned purchases. |

| Repayment | Pay interest on funds used. | Fixed monthly payments. |

| Interest | Typically variable rates. | Often fixed rates. |

Lines of credit offer operational fluidity, while loans are for deliberate investments. For slow-paying customers, consider invoice factoring.

Why Choose a Line of Credit?

A line of credit is a financial safety net. Its power is its flexibility—a revolving source of capital for daily business needs. It’s perfect for handling unexpected repairs or seizing inventory deals. You only pay interest on what you use, saving money.

The "revolving" nature means as you repay, the credit replenishes. This is great for cyclical businesses. Explore the best business lines of credit here.

When a Term Loan Makes Sense

For a significant, one-time investment, a business term loan is the strategic choice. It's a lump-sum for large projects like buying real estate or a major expansion.

Its predictability is a key advantage. You get fixed monthly payments over a set term (2-10 years), making long-term planning easy. Successfully managing a term loan also builds your business credit profile. Learn about a business term loan here.

Costs and Qualifications

When weighing a business line of credit vs loan, consider costs and approval odds. A term loan is predictable with a fixed interest rate. A line of credit is dynamic, with variable rates. See how these funding options compare on AmericanExpress.com.

Term loans have stricter requirements (credit score 680+, 2+ years in business). Lines of credit are more accessible (scores from 600, 6+ months in business). Organize your data; learn to convert bank statements to Excel. Our guide on small business loan requirements offers more details.

Frequently Asked Questions

Can I have both?

Yes, many businesses use both. A loan for a large purchase and a line of credit for daily cash flow.

Will applying hurt my credit?

A hard inquiry causes a small, temporary dip. On-time payments will build your credit long-term.

How quickly can I get funded?

Lines of credit are faster, often within 1-2 business days. Term loans can take longer.

Ready to find the right funding solution? FSE - Funding Solution Experts connects you with over 50 lenders. Learn more at fseb2b.com.